Deep Dive

TL;DR Choosing how to deploy liquidity strategies and allocate capital onchain can be challenging for DAOs, especially as they usually have multiple stakeholders and operational constraints. This guide covers the key considerations DAOs should make with building Protocol Owned Liquidity and other strategies.

Deploying liquidity onchain is a major challenge for many DAOs. They often face bottlenecks due to team constraints and key decisions are subject to governance votes involving multiple stakeholders. This makes it difficult to manage resources efficiently.

Arrakis Pro has guided leading DAOs like Across, Stargate, and ether.fi through the complexities of onchain liquidity. We also regularly dig into the ecosystem’s most active governance forums to find out how DAOs are approaching treasury management. Based on our hands-on experience and findings, we’ve identified several key questions DAOs face when thinking about their Protocol Owned Liquidity.

We compile them in this feature to offer crucial insights on how DAOs can manage their resources effectively, deploy liquidity strategies, and position themselves for long-term stability.

Table of Contents

1. What is the best approach for acquiring the quote asset?

2. Is renting liquidity worth the cost?

3. Why is building POL important?

4. What are the risks and trade-offs of deploying POL?

5. Why should DAOs use concentrated liquidity solutions and how should they set and manage price ranges for POL?

6. Why are oracles important and how does POL strengthen their security?

7. How do lending protocols like Aave assess a token’s liquidity before listing it?

8. What operational steps can DAOs take to speed up execution with regards to treasury management?

1. What is the best approach for acquiring the quote asset?

Acquiring sufficient sell side liquidity without eating into treasury resources is a common challenge. DAOs frequently seek advice on the best approach.

“We have some ETH in our treasury but would prefer to keep most of it to ensure we’re sufficiently diversified. We also don’t want to sell more of our governance token OTC at a discount to current prices. We feel it's undervalued. How can we still enable our POL with only a little ETH to start?” - $200M FDV DeFi Project listed on Bybit

To deploy liquidity onchain, DAOs often need a quote asset such as ETH in addition to their token. Using ETH for the quote asset minimizes IL and LVR because it has less price divergence from their token than stablecoins. However, DAOs may lack sufficient resources to accumulate ETH and allocating funds requires governance approval.

Liquidity bootstrapping is one way to acquire ETH on concentrated liquidity solutions without creating active sell pressure or costly incentive programs.

Selling the native token to acquire ETH creates sell pressure and bad optics onchain. OTC swaps can prevent this sell pressure but aren’t feasible for all teams (plus, OTC deals may be unfavorable if they feel their token is undervalued).

80/20 pools (such as those offered by Balancer) offer an alternative solution by allowing DAOs to weigh pools towards their token, though they are not as customizable as UniV3 and UniV4 pools.

Single-sided LPing also offers a way to acquire ETH on concentrated liquidity solutions without creating active sell pressure or costly incentive programs. This strategy uses single-sided LP positions instead of swaps to accumulate the quote asset over time. Arrakis Pro uses “Hard Bootstrapping” and “Soft Bootstrapping” strategies depending on the team’s needs. “Hard Bootstrapping” raises ETH or stables for the treasury by removing liquidity as the governance token gets sold. This ensures that volatility or price changes don’t convert the asset back to the governance token, effectively using LPing (maker orders) to execute limit ordering.

“Soft Bootstrapping” lets DAOs provide their token and the quote asset at a ratio of 80:20 aiming to convert to 50:50 over time. In other words, you are passively selling your governance token above the current market price (and not at a discount) to provide better depths onchain. As more ETH is acquired, more inventory can be allocated, minimizing the pool’s price impact. As with other liquidity-related decisions, governance must decide the strategy and starting ratio to opt for.

2. Is renting liquidity worth the cost?

Renting liquidity can be expensive. DAOs must weigh up the costs compared to other approaches such as building POL.

“In traditional liquidity mining, rewards are distributed uniformly across all LPs without performance-based goals, based on their liquidity density. This often attracts mercenary LPs—participants who chase high APRs for short-term gains but exit once rewards are claimed. This behaviour can drain liquidity, creating instability over the long run.” - metrom in Supporting MORPHO token liquidity on DEXs

DAOs must always pay a cost for liquidity, whether through options to market makers, bribes, emissions, or IL.

DAOs have historically distributed token incentives through liquidity mining programs, which work best post-TGE when LPs flock to pools to accrue fees from high volumes. Liquidity mining is most effective when fees exceed emissions. But this approach effectively involves “renting” liquidity as LPs aren’t loyal and emissions create sell pressure for your token. This is why liquidity mining is usually unsustainable in the long term.

Paying bribes through platforms like Aerodrome (on Base) and Velodrome (on Optimism) is another way to increase pool liquidity. DAOs can pay veToken holders to direct emissions to their pool or purchase veTokens directly. They can also supply AERO and VELO rewards to lending markets to accrue extra yield.

LPing on such solutions creates IL risk. But it also offers a way to diversify their treasury without creating sell pressure depending on the rewards available and chosen strategy. DAOs should define their goals before opting for such an approach.

Liquidity mining and bribing tends to be unsustainable as a long-term strategy.

Similar to liquidity mining, bribes become ineffective over time as rewards decline. Bribing rewards locked token holders rather than LPs, who often sell their rewards to accrue more voting power.

Reward and bribe programs eat into resources and require monitoring. On concentrated liquidity solutions, LPs may place liquidity in narrow ranges to maximize rewards then leave once they dry up.

The main alternative is to use POL. This approach typically requires ETH (or stablecoins) and carries IL risk but the cost of capital is lower because the DAO seeds its own liquidity instead of renting it. Onchain market making is one way to deploy POL and achieve greater capital efficiency with less liquidity, allowing DAOs to allocate resources towards growth and development.

3. Why is building POL important?

Teams often ask why they need to build onchain liquidity (POL) for their token in the first place, particularly when they are short on resources. A look at how market makers operate on CEXs illustrates why POL is important.

“What are the best reasons for building POL vs. other approaches and how much can market makers help? We don’t want to deplete too many of our resources.” - early Arrakis Pro user targeting $100M FDV

Whether using CEXs or DEXs, projects need deep liquidity for their token. For CEX listings, teams rely on (two or three) market makers like Wintermute or GSR. The most popular approach for building liquidity is the loan and option model, though some use the retainer and working capital model. While allocation requirements vary between market makers, projects typically lend out 1-5% of their token supply (plus stablecoins with the retainer and capital model).

The market maker’s goal is to manage their risk and profit from bid-ask quotes.

With the loan and option model, the project lends out their token and gives the market maker the option to buy the tokens at a strike price based on the early trading price. This benefits the market maker if the price rises, though such options rarely get exercised. These agreements are optimized for order book market making and the market makers profit from the bid-ask spread; they’re responsible for committing their inventory as required but their goal is to manage their risk and profit from their quotes.

The market makers aim to generate profits from their trades. Some predatory firms profit by shorting the project’s token post-TGE then buy back their position after prices have tanked (so that they can return their loan without taking on much risk). But even if they don’t use such strategies, market makers often dump the token for quote-side liquidity and they’re incentivized to provide wide spreads and shallow depths to improve their margins. This is at odds with what projects and users want.

While market makers are well-versed in providing a service on CEXs, they aren’t as optimized or incentivized to provide liquidity onchain.

The retainer and working capital model involves paying fees plus capital (the token and stablecoins) to the market maker. The market maker gets a percentage of any increase in the working capital’s value but the bulk of their compensation comes from the retainer. This model essentially puts the market maker in charge of the team’s POL for all trading venues. But when the project puts up a large supply of funds, they do not receive any downside protection.

Setting KPIs for liquidity depth and asking for regular reports are some solutions to the pitfalls associated with engaging with market makers.

Understanding the crypto market maker complex is essential to understanding why building POL is important. Market makers operate to make money from loans and spreads. But this approach doesn’t translate to onchain liquidity pools, where liquidity depth is the top priority. Some firms also help projects with their onchain liquidity, but in general their main aim is to profitably trade on CEXs through wide spreads.

Furthermore, healthy spot liquidity is key for any functioning perps market. Many DeFi traders favor perps over spot but a tension can arise if spot volumes and liquidity start to diminish relative to perps, as explained by Ambient Finance’s Doug Colkitt. This is another reason why projects are in the interest of making sure they have adequate POL for spot markets.

4. What are the risks and trade-offs of deploying POL?

DAOs often express concern over the risks of building POL and whether they outweigh the benefits versus other liquidity strategies.

The biggest risk to DAOs deploying liquidity onchain is IL. A whale’s large sell trade can cause a significant price impact if liquidity is spread thin, leaving the DAO rich in their governance token and poor in ETH. In other words, the DAOs risk being used as exit liquidity.

DAOs should also consider how they rebalance positions if impacted by IL. Fixed rebalances can create permanent losses whereas a more strategic approach offers a solution to this problem.

DAOs can think about IL in similar terms to stock buybacks to assess the risks and select ranges they would be comfortable buying at.

When setting ranges, DAOs should consider the price they would comfortably accumulate all their tokens at in case of high sell pressure. Similar to stock buybacks in equities markets, DAOs should be confident that they are prepared to buy back their token at the prices implied by their POL ranges.

The cost to building POL is IL and this should be lower than the cost of emissions for renting liquidity. LPs also suffer from LVR if the pool gets arbed, though trading fees can help offset the cost in volatile periods. Using MEV-aware pools with dynamic fees (such as the Arrakis Pro Private Hook on UniV4) helps minimize IL and LVR.

The biggest risk to DAOs deploying liquidity onchain is IL. They could be used as exit liquidity.

Volatility should be a key consideration for all DAOs building POL because it creates IL and LVR. DAOs can use volatility indicators to widen ranges when volatility increases or tighten ranges when volatility decreases.

DAOs should also consider their CEX strategy alongside their onchain strategy because IL risk is higher if CEX and DEX prices are not at parity.

Finally, building a POL strategy impacts token staking. A high staking ratio is a sign of strength as holders show long-term conviction. When DAOs deploy POL, they optimize for liquidity depth over staking and expose their token to market risk.

5. Why should DAOs use concentrated liquidity solutions and how should they set and manage price ranges for POL?

DAO stakeholders frequently show misunderstanding of how concentrated liquidity solutions work when assessing whether to build POL.

“No one is protected from impermanent losses. Any range adjustment results in a loss unless the fees collected exceed the loss incurred during the adjustment… At this stage, I don’t see the point in increasing liquidity in a narrow range on DEXs; it would make more sense to create a pool from 0 to infinity for all this liquidity… if we claim that there is a point, then what range will be chosen? I don’t see the sense in ‘locking’ the price in a range…” - grumlin in Onchain Market Making for $LSK on Ethereum via Arrakis Pro

Constant product pools have historically been popular for DAOs deploying liquidity onchain due to their simplicity. The “set and forget” factor appeals to less agile groups, plus LP tokens are composable and prices are hard to manipulate when liquidity sits on the whole curve.

DAO stakeholders often dismiss concentrated liquidity solutions because they view them as complex. As the quote above shows, they may also be misguided in how they function. Concentrated liquidity solutions like UniV3 and UniV4 offer token issuers flexibility to deploy liquidity strategies like Limit Order Rebalancing and range layering but such approaches are beyond the scope of most LPs.

DAOs must strike a balance between minimizing inventory risk and price impact.

For DAOs using concentrated liquidity solutions to deploy POL, selecting appropriate ranges is key. DAOs must strike a balance between minimizing inventory risk (with wide ranges) and price impact (with narrow ranges).

Most DAOs want to maintain price stability and preserve runway while also offering users good execution. With concentrated liquidity solutions, LPs can meet the required slippage conditions to improve UX without providing tail liquidity. Lowering a token’s price impact also incentivizes long-term holding as it becomes more resilient to sell side pressure.

6. Why are oracles important and how does POL strengthen their security?

DAOs need oracles to enable lending markets, perps, and other DeFi primitives. This need strengthens the case for building POL.

Whether using DEX pools, lending protocols, or other solutions, DAOs need oracles to provide reliable onchain prices. Similarly, oracles need deep, liquid markets to maintain accurate feeds.

Chainlink is the leading price feed oracle but integrating it has a significant cost and time burden that most DAOs can not afford. Many DAOs opt for an onchain TWAP oracle instead. Building POL helps DAOs ensure that they have a robust TWAP oracle to leverage for other use cases such as lending market integration.

TWAP oracles are not safe unless onchain pools have sufficient liquidity depth.

TWAP oracles use prices across regular time stamps and calculate the average to protect against manipulation. They need sufficient liquidity depth to work effectively, which strengthens the case for building POL.

UniV3 pools can function as oracles, offering historical liquidity data that helps LPs verify current prices against the TWAP. UniV4 pools could also potentially be customized to build an advanced oracle that removes outlier swaps.

While TWAP oracles protect against manipulation, they make a trade-off on accuracy as they use averages rather than specific prices. This problem is heightened during volatile periods. Despite these downsides, the cost and waiting time associated with integrating solutions like Chainlink make onchain oracles a go-to option for many DAOs.

7. How do lending protocols like Aave assess a token’s liquidity before listing it?

Lending protocols attract DAOs because they can offer enhanced liquidity and utility for their token. But these protocols have strict requirements and processes in place for listing new tokens. This creates new considerations for how DAOs think about their POL.

Many larger DAOs aim to receive support for their token on lending protocols to improve their token’s liquidity, expand its utility, and increase integration across the DeFi ecosystem. These factors contribute to price stability and make holding more attractive.

Aave lists leading DeFi tokens and stablecoins that meet specific liquidity requirements. Proposed listings must pass through governance, with proposals often highlighting the token’s utility and the niche it occupies. For example, authors may make the case that their token could give Aave a lead in RWAs or encourage farming strategies.

Chaos Labs and LlamaRisk are Aave’s risk managers (“risk service providers”) and they evaluate key metrics including:

Trading volumes

The token’s paired asset

Liquidity concentration

Buy side liquidity

Price history

Volatility

Incentives (and the degree to which rewards are inflating a pool’s metrics)

The TVL in the token’s project and proposed chain deployment

Chain deployments

Bridging solutions

Price feed sources

Supply distribution

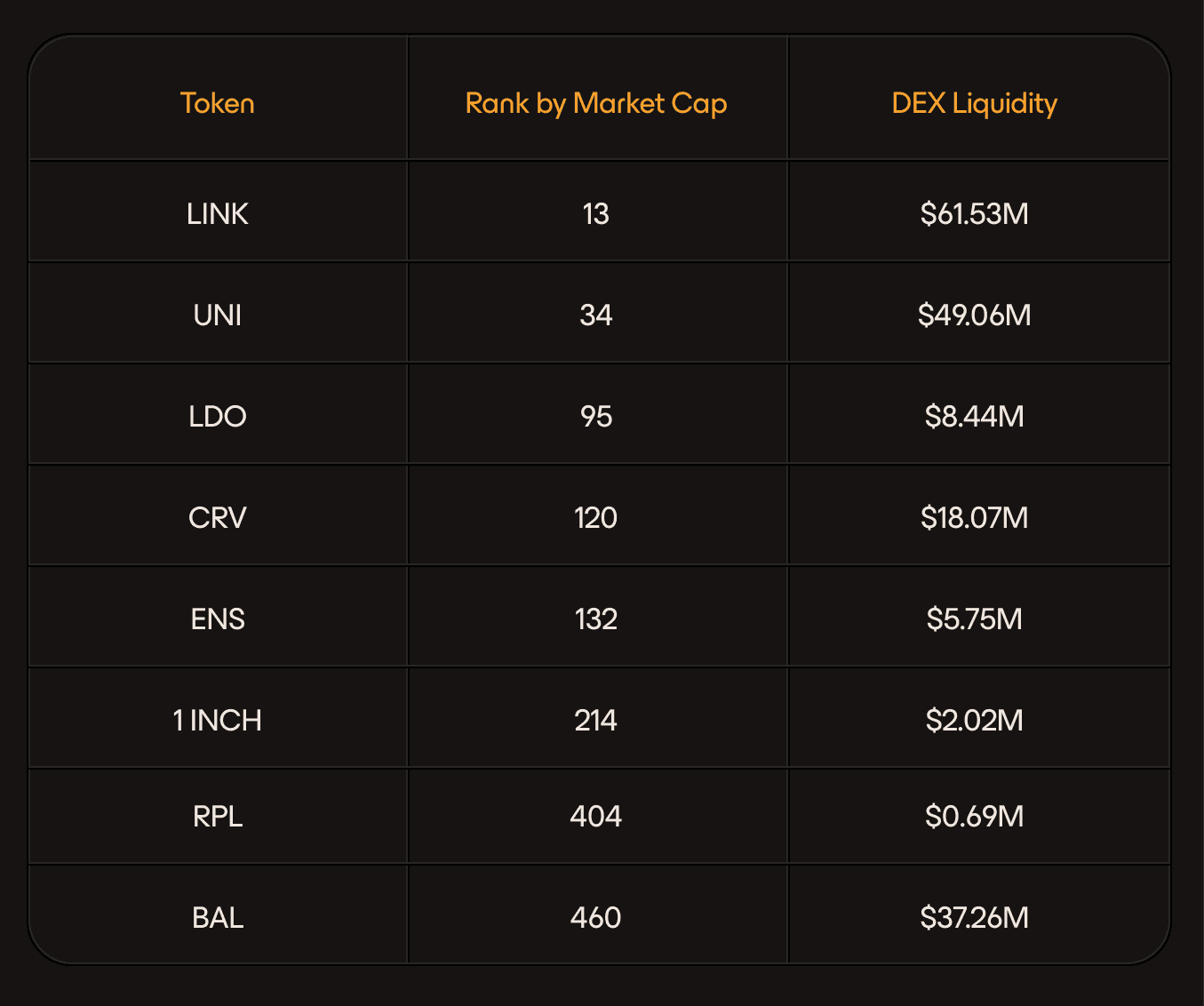

While there’s a large variance between Aave’s supported assets, longtail assets outside of the top 100 tokens by market cap typically have a minimum of $5 million in daily DEX volume and $1 million in DEX liquidity (though the average across them is closer to $15 million in volume and $10 million in liquidity). Examples include RPL, ENS, CRV, SNX, and BAL.

A series of tokens supported on Aave V3 Core Instance and their DEX liquidity. Data correct as of March 24, 2025 (Source: DeFi Llama)

Additionally, Aave’s L2 markets frequently support the corresponding L2’s native asset, for example ARB on Arbitrum, SCR on Scroll, and so on.

Longtail tokens supported on Aave typically have at least $5 million in daily DEX volume and $1 million in DEX liquidity.

Top 50 tokens, meanwhile, typically have upwards of $50 million in both daily DEX volume and liquidity. DEX tokens like CRV, BAL, and UNI also stand out for their high liquidity due to their prominence on their respective DEXs (Curve on mainnet, Balancer V2 on mainnet, Uniswap V3 on mainnet).

When assessing new assets, the risk service providers look closely at liquidity concentration and price impact alongside other factors. Assets considered for listing usually have at least $2 million in daily DEX volume and liquidity and the ability to handle seven-figure swaps within a 7.5% price impact.

However, it’s worth noting that the governance board sees proposals for a wide range of assets and the risk service providers look at multiple factors. For example, pufETH’s $6 million in DEX liquidity was cited as one of several reasons to refrain from listing the token on Aave V3 Core even though some other supported assets have lower liquidity.

DAOs must ensure they have sufficient liquidity onchain if lending protocol support is a priority for them.

Market depth is important to lending markets because they prefer stable assets with minimal price impact. Tokens prone to high slippage and volatility pose greater liquidation risk and potential bad debt exposure.

To mitigate bad debt risk, lending protocols carry out risk assessments and governance votes to support new assets. They also set higher LTV ratios and liquidation bonuses for more volatile assets (i.e. assets they deem riskier).

While lending protocols usually don’t publish minimum liquidity requirements, DAOs must ensure they have sufficient liquidity onchain if lending protocol support is a priority for them.

8. What operational steps can DAOs take to speed up execution with regards to treasury management?

Unlike early-stage projects with nimble teams, DAOs involve many stakeholders. This means they tend to move slower and have different steps to consider when deploying a new liquidity strategy.

DAOs are meant to be “autonomous.” But they often lack agility and face pain points that hinder progress. While DAOs have similar liquidity goals to token issuer teams, they must align incentives between many stakeholders and vote on key decisions. Governance votes can also be frontrun (potentially harming the proposed strategy) or fail to pass (due to a lack of quorum).

Treasury management is key to achieving long-term stability but it’s often handled by team members as a part-time commitment. Due to operational constraints, DAOs generally don’t make treasury management decisions based on market conditions.

DAOs have similar liquidity goals to token issuer teams but they must align incentives between many stakeholders.

In some cases, DAOs may elect to form a Treasury Council to deploy a liquidity strategy. This process creates hurdles: the DAO must decide on the appropriate members to elect and ensure they can access a multisig wallet to execute transactions. Using multisigs introduces new problems, such as timezone conflicts and council members taking time off from work. After the initial deployment, the strategy may also need to be monitored and updated once passed through governance, draining resources.

In summary, decentralized and autonomous governance is difficult in practice. Teams should factor for the speed they can move at when considering new liquidity strategies. Electing a new body may be required, but if the DAO is too constrained, calling in help from liquidity experts may be the next best step.

Level Up Your DAO’s Onchain Liquidity

In summary, DAOs have many things to consider to achieve effective treasury management and onchain liquidity. This is a function of the space’s complexity today. Similar to token issuers, DAOs usually seek price stability and long-term sustainability. They can build POL to position themselves for long-term success but there are many considerations to take when adopting this approach.

DAOs also differ from other entities in that they are usually created post-TGE so that they can be “decentralized” and “autonomous”. This means that decision making can be slow and bottlenecks are common. Many DAOs also treat liquidity management as a part-time job, but managing onchain liquidity requires active monitoring to achieve sustainability. This is where solutions like Arrakis Pro can help.

Arrakis Pro is crypto’s first onchain market maker, focused on helping DAOs and other entities strengthen their onchain liquidity. We’ve helped 50+ leading teams navigate the complexities of the onchain liquidity landscape, including the likes of Across, ether.fi, and Stargate. Check out our in-depth guide to POL to learn more about how we’ve earned the industry’s trust or fill out our contact form to reach out about onboarding.

References

Aave Docs [Aave]

Aave Forum [Aave]

Abracadabra Forum [Abracadabra]

Across Forum [Across Protocol]

Actions Taken on Market Maker Due to Market Irregularities (2025-03-25) [Binance News]

Aera Docs [Aera Finance]

Aerodrome Docs [Aerodrome Finance]

Ampleforth Forum [Ampleforth]

Arrakis Pro: The Onchain Market Maker for Token Issuers [@dreamsofdefi for Arrakis Finance]

Arrakis x Uniswap V4 Is Here [@dreamsofdefi for Arrakis Finance]

Aura Docs [Aura Finance]

Balancer Docs [Balancer]

Chaos Labs [Chaos Labs]

Compound Forum [Compound Finance]

Doppler: A liquidity bootstrapping ecosystem [Whetstone Research]

ether.fi Forum [ether.fi]

Forgd Academy Docs [Forgd]

Framework for an Active DAO Treasury Execution [Karpatkey]

HOPR Forum [HOPR]

Karpatkey [Karpatkey]

Lisk Forum [Lisk]

Mimo Governance Forum [Mimo]

Moonwell Forum [Moonwell]

Morpho Forum [Morpho Finance]

Stargate Forum [Stargate Finance]

The AMM Renaissance: How MEV Auctions and Dynamic Fees Prevent LVR [@dreamsofdefi for Arrakis Finance]

The Arrakis Pro Guide to Protocol Owned Liquidity: Key Tips for TGE and Beyond [@dreamsofdefi for Arrakis Finance]

Uniswap V4 Is Live. These Are the Hooks To Look Out For [@dreamsofdefi for Arrakis Finance]