Arrakis Alpha

TL;DR

Base launchpads have exploded: $20B+ in volume, 5.4M tokens created, 72M wallets interacted.

Launchpads covered: Virtuals Protocol, Zora, Ape.Store, Clanker.

Main issue: liquidity inefficiency. Protocol-owned liquidity deployed by launchpads underperforms mercenary capital.

Example: An $AIXBT/wETH pool with $52K TVL generates more orderflow than a $2.3M pool.

Causes: passive liquidity, poor range management, weak routing.

Fix: active liquidity management with dynamic ranges + rebalancing.

Goal: keep trading volume and fees inside the Base ecosystem.

Cut through the noise. Subscribe to Arrakis Alpha for sharp, actionable onchain market research.

Data powered by Dune and Sealaunch.

Introduction

Token launchpads continue to play a central role in onchain activity. What started as coordinated ICO-style platforms like Pink Ecosystem or CoinList has evolved into autonomous token factories that automate creation, bonding, and liquidity deployment.

In 2023, platforms like pump.fun reshaped how communities launch tokens. Today, Base has emerged as one of the fastest-growing ecosystems for these launchpads. Projects such as Virtuals Protocol, Clanker, Zora, and Ape.Store are powering a new onchain creation economy.

This article examines:

How Base-native launchpads operate

Key data behind their rapid growth and current market size

Why their liquidity frameworks often lag behind their success

The Launchpad Surge on Base

Base’s launchpad sector is large, active, and fragmented. No single platform dominates, but together they form one of the most dynamic areas of the Base ecosystem.

As Manuel Amaral, co-founder of Sealaunch, put it succinctly:

Token launchpads are a major trend this cycle, and Base sits at the center.

Unlike Solana’s memecoin-driven pump.fun, Base supports broader categories including AI agents and creator tokens. Continued experimentation and niche-specific launchpads are likely.

Cumulative Metrics Since October 2023

$20B+ in launchpad trading volume

5.4M+ unique tokens created

72.3M+ unique wallets interacted with launchpad protocols

Data: Sealaunch — https://dune.com/queries/4915278/8136666

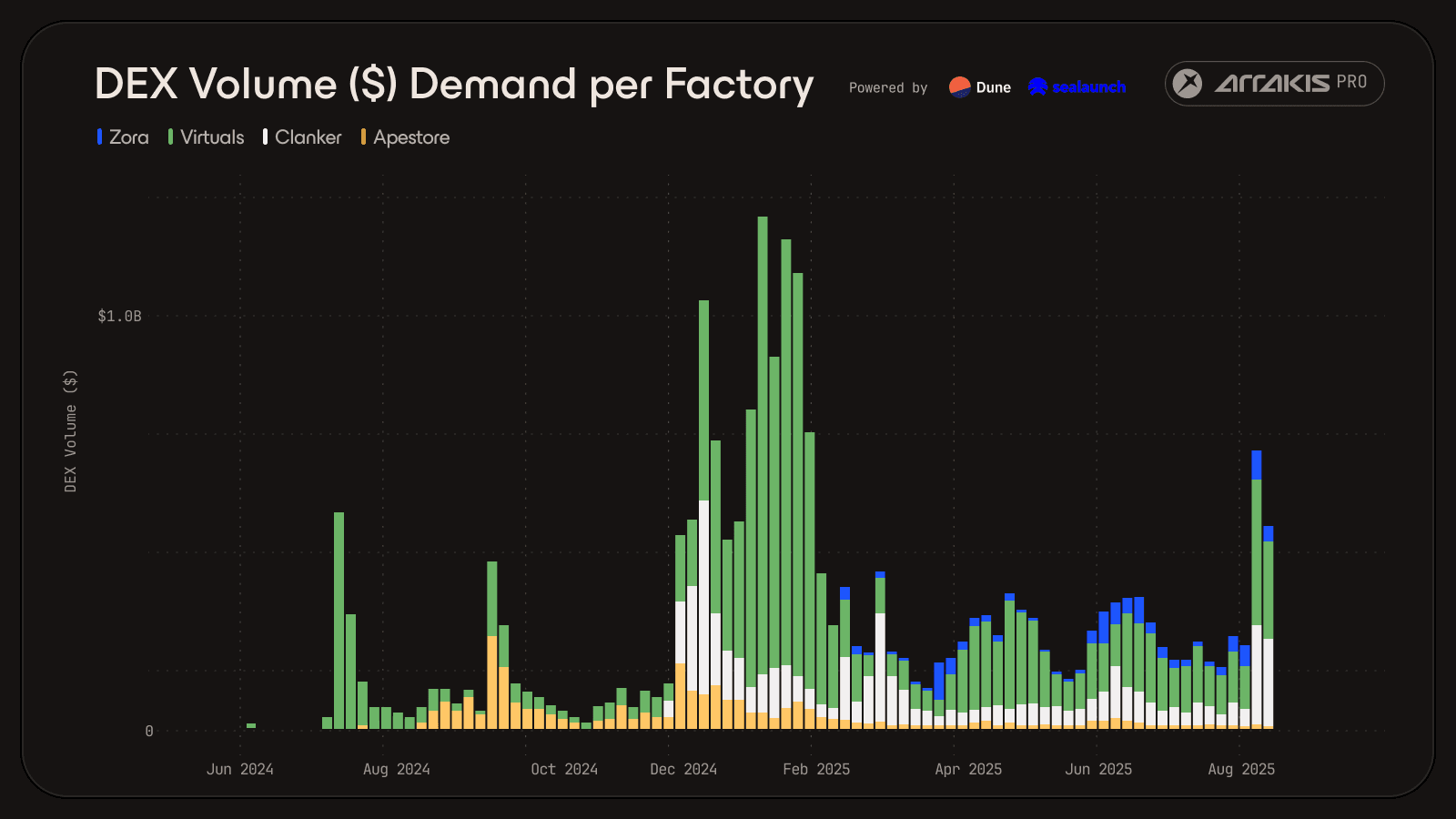

Although volumes peaked in January 2025, driven by a wider memecoin mania, daily activity has remained strong, indicating steady demand even after the initial hype faded.

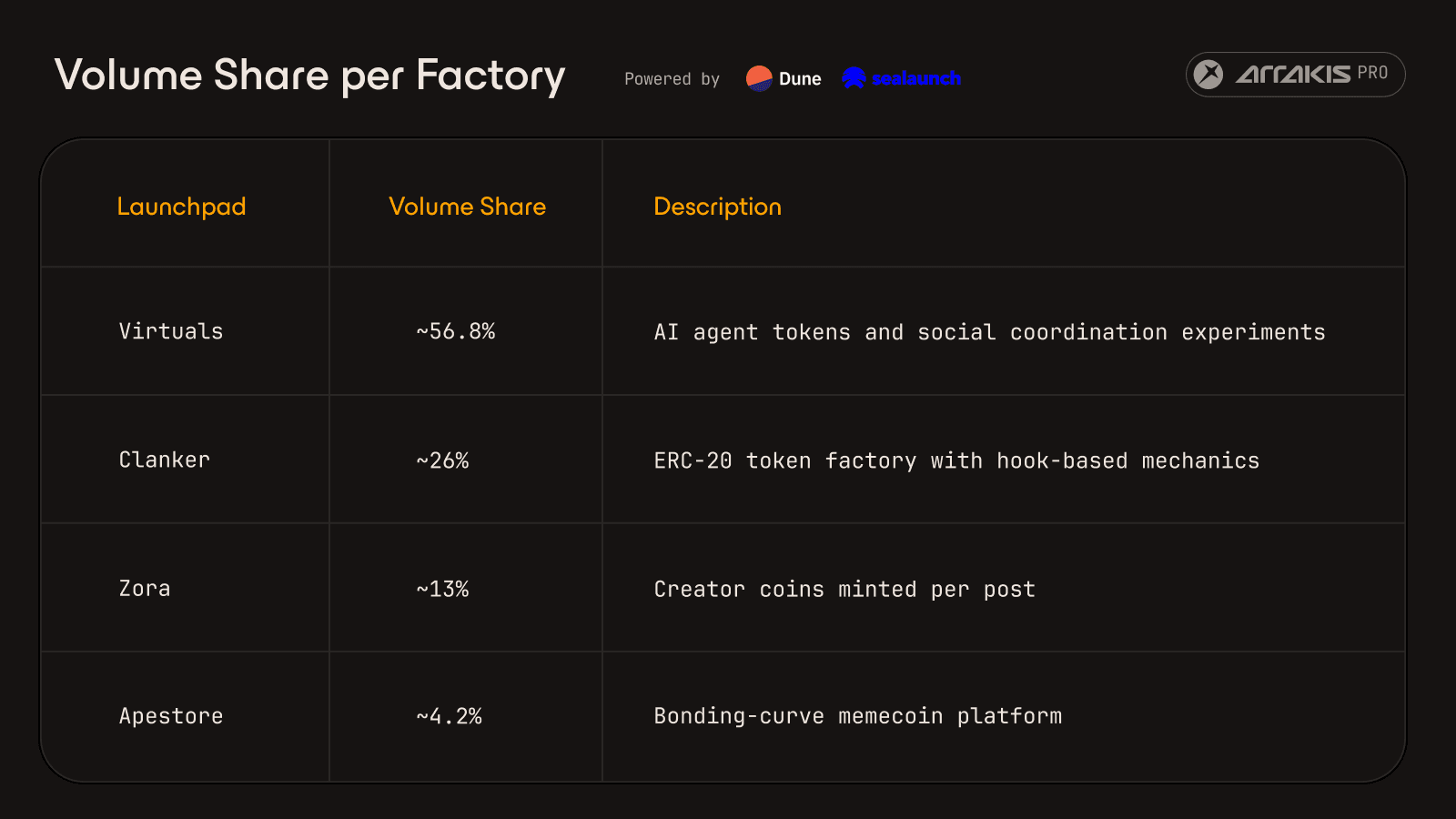

Market Leaders

Data from Q3 shows a diverse landscape with multiple players serving distinct niches.

Data: Sealaunch — https://dune.com/queries/4915278/8136711

While Virtuals leads in volume, Zora creates the highest number of tokens since each post on the platform is represented by a minted token. Apestore, once dominant with a roughly 80% share at the end of June 2024, has since lost traction.

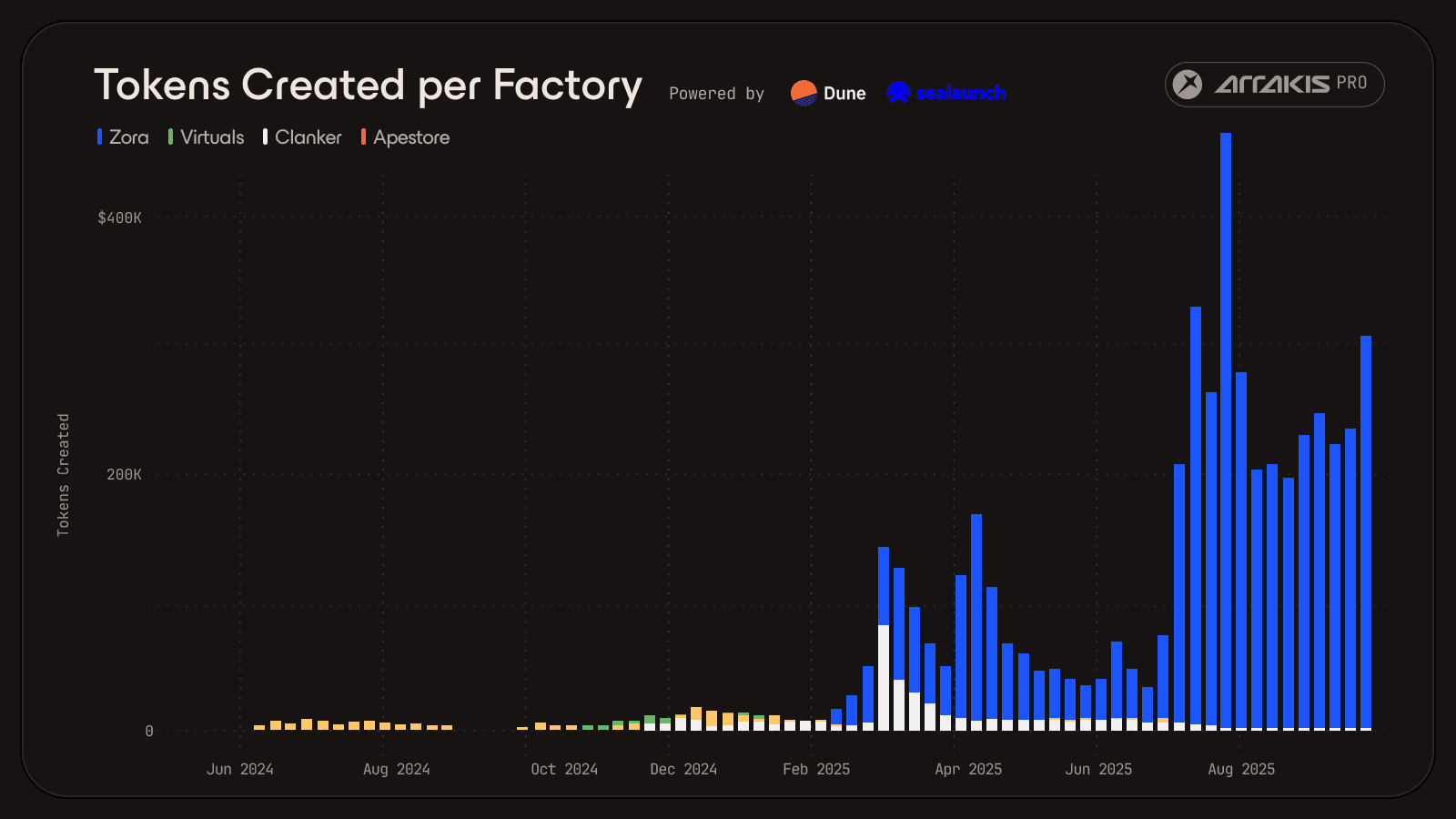

The data demonstrates a strong product-market fit: users consistently launch a high volume of new tokens, even as speculative intensity fades away.

Data: Sealaunch — https://dune.com/queries/4906213/8122438

However, beneath this momentum, a critical pattern has surfaced, the liquidity supporting these launches is frequently inefficient.

When Liquidity Fights Back

Launchpads typically facilitate token launches by deploying liquidity on-chain, usually funded by the project itself. The launchpad often holds a significant share of the token supply to ensure fair distribution and market stability. Liquidity may come from tokens allocated for this purpose and a portion of sale proceeds, or, in some cases, through participant-driven mechanisms such as direct minting or bonding curves. The deployed liquidity is meant to make the market functional and liquid from day one. In practice, however, this assumption rarely holds true.

Across leading launchpads, external concentrated liquidity (CL) pools on Aerodrome outperform the native launchpad pools, even when the latter hold significantly higher TVL. This pattern repeats in every major case reviewed.

Case Study: $AIXBT on Virtuals

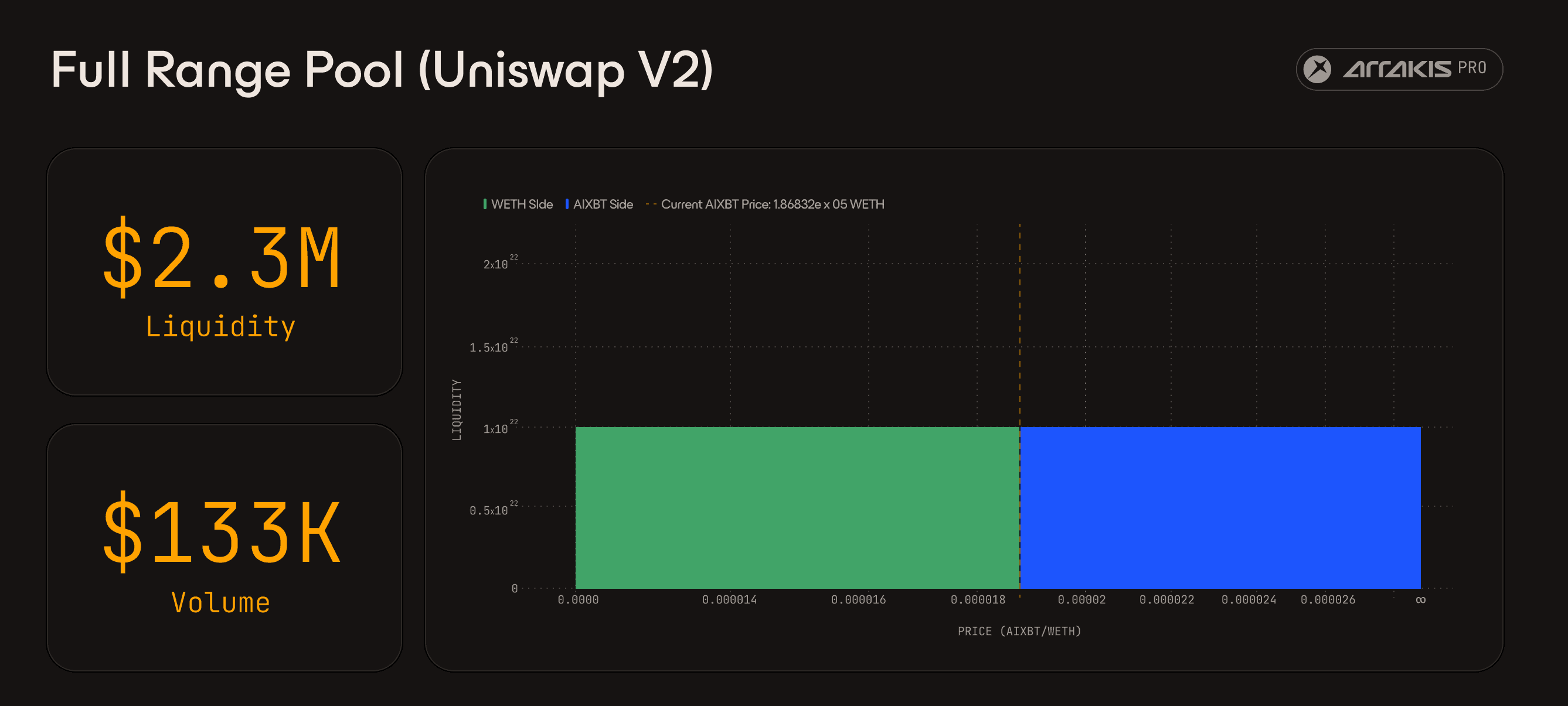

Virtuals introduces an innovative “auto-graduation” mechanism for token launches. Once 42,000 $VIRTUAL has been spent on a creator’s token, the system interprets this as strong community demand and automatically deploys a 50/50 Uniswap v2 pool. This provides initial liquidity and instantly enables trading without any manual setup. The launch of $AIXBT on Virtuals shows that the way liquidity is structured and how efficiently it’s managed have a bigger impact on trading activity than the size of the pool itself.

Across networks and DEXs, several pools exist for $AIXBT, yet their performance varies significantly. As of November 3, 2025, the initially launched Uniswap v2 $AIXBT/$VIRTUAL pool, where funds are distributed evenly from zero to infinity, holds $2.3M in liquidity but only records about $133K in daily volume, with a volume-to-liquidity ratio of 0.057x.

VIRTUAL / AIXBT - Uniswap Pool

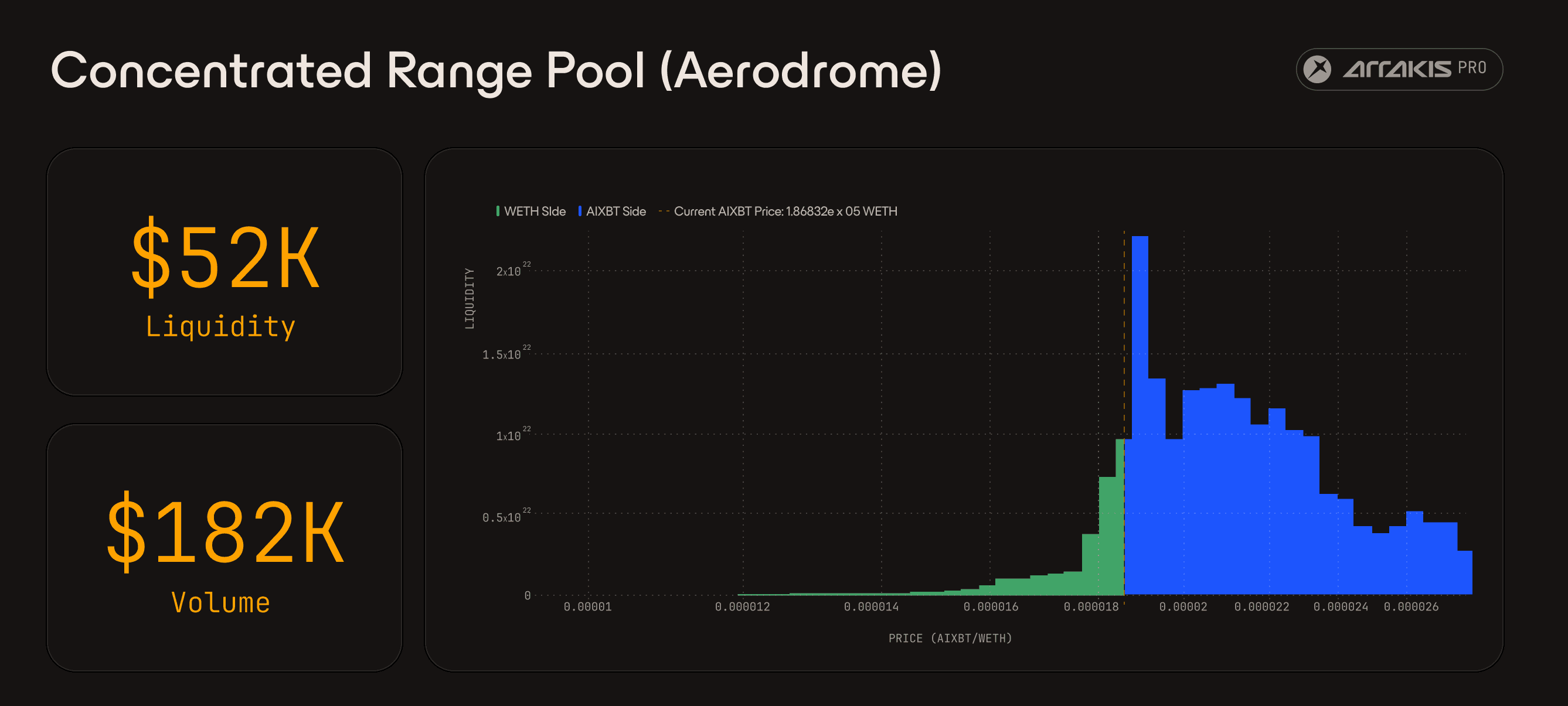

In contrast, concentrated range pools allocate funds as close to the active price as possible and, despite having a fraction of the liquidity, achieve similar or higher trading volumes. The most extreme example is the $AIXBT/wETH CLAMM pool on Aerodrome, which holds just $52K in liquidity yet generates $182K in daily volume, achieving a volume-to-liquidity ratio above 3.5x, based on data from November 3, 2025. This highlights how optimized design and aggregator routing can amplify trading activity without large capital reserves.

Pool Address - 0x22a52bb644f855ebd5ca2edb643ff70222d70c31

The data speaks clearly: despite having much deeper liquidity, the $AIXBT/$VIRTUAL v2 pool lags behind the small $AIXBT/wETH Aerodrome pool, which trades more than three times its own liquidity.

$AIXBT reflects a consistent pattern seen across the Virtuals ecosystem and other launchpads alike - smartly managed liquidity structure outperforms size. Efficiency, routing, and design ultimately determine trading performance, not the amount of capital locked in a pool. A larger liquidity pool does not necessarily translate into higher trading activity.

In summary, CLAMM pools paired with major assets like USDC or wETH connect better with aggregators, improving discoverability and trade flow. By concentrating liquidity within tighter ranges, they achieve stronger execution and higher capital efficiency than Uniswap v2’s full-range pools. Even with higher fee tiers, CLAMMs often outperform because efficiency and routing matter more than cheaper trades.

Conclusions

Base has become a key launchpad for new forms of onchain creation, community ownership, and experimental token models. Yet, despite the progress, liquidity remains the biggest structural challenge once the initial excitement fades.

The Core Problem: Inefficient Liquidity

Across most launchpads, liquidity still follows outdated, passive models. Pools are often deployed as full-range or unmanaged CLAMMs, spreading liquidity thin and leaving it unoptimized as trading begins. Active LPs quickly take over, capturing most of the trading volume and fees. This drains the launchpad’s own pools, leaving protocol-owned liquidity idle and reducing income for both creators and the platform. In the long run, this dynamic discourages participation and erodes one of the main incentives for building onchain.

The Path Forward

To fix this, Base launchpads should move from static liquidity setups to dynamically managed pools. Concentrated ranges, flexible fee tiers, and ongoing rebalancing can turn liquidity into a productive, self-sustaining resource. Such an approach deepens markets, stabilizes prices, and ensures that the value generated through trading remains within the ecosystem that launched the token.

Base nailed token creation. Now it’s time to conquer liquidity management.