Hyperliquid

Cross-venue lead-lag across 29 crypto perp markets, and a deeper look into PerpDEX architectures.

Introduction

Hyperliquid is the biggest onchain perp venue by volume and open interest. It has expanded beyond crypto perps into RWAs, prediction markets, and a permissionless DeFi stack. If you spend enough time on Crypto Twitter, you will hear some version of the claim that Hyperliquid has displaced Binance as the venue where crypto price discovery now happens.

We tested this claim. Taking inspiration from Hoffmann, Rosenbaum, and Yoshida (2013), we ran a modified Hayashi-Yoshida lead-lag estimator across three venues: Hyperliquid, Binance Futures USDT-M, and Lighter.

What we measured

The question: when the price of an asset moves on one venue, how long does it take for the price to show up on the others?

Every venue publishes a trade tape, a timestamped list of every fill that happens. The cleanest way to measure cross-venue lead-lag is to take two tapes, shift one in time relative to the other across a range of possible time-shifts, and pick the shift where the price moves on both tapes line up best. Whatever shift produces the cleanest alignment is the lead-lag between the two venues.

If shifting Hyperliquid back by 700 ms makes its price moves line up cleanly with Binance's, Binance is leading by 700 ms.

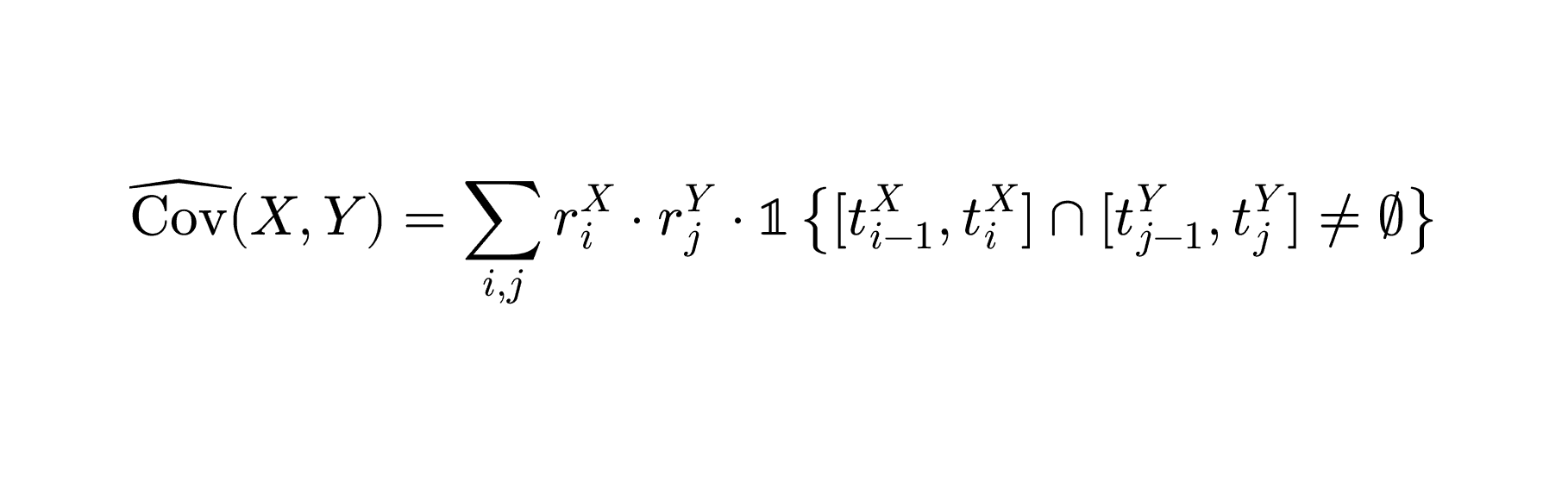

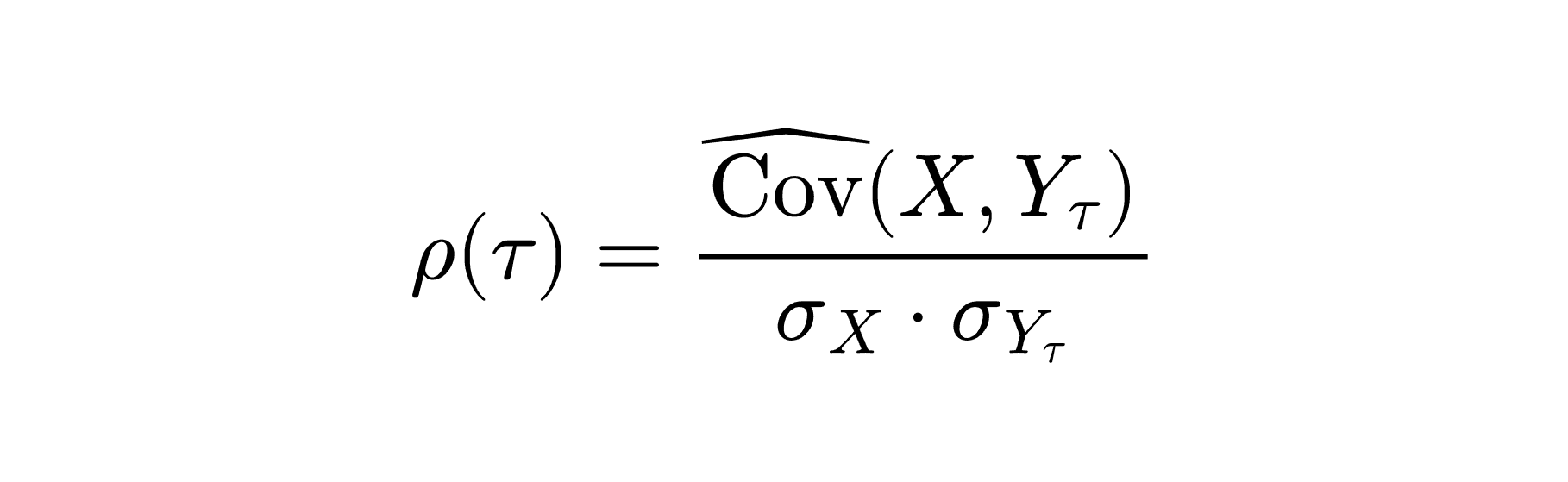

We use the Hayashi-Yoshida estimator (Hoffmann, Rosenbaum, Yoshida, 2013), designed for two price series whose trades happen at irregular, non-synchronised times. At each candidate time-shift, it computes:

Where Cov(X, Y) is the covariance between X and Y, in our case, the fill-return series from the two venues we are comparing. σ_X and σ_Y are the standard deviations of those two distributions.

We run the estimator separately on bid-side fills (taker-sells) and ask-side fills (taker-buys) to avoid bid-ask bounce noise at sub-second resolution. For each pair, we compute ρ across a grid of time-shifts from −2,000 ms to +2,000 ms in 100 ms steps, then read off the shift at which ρ peaks. Positive lag means the first-named venue leads.

We analysed the top 29 crypto assets by market cap that trade on all three venues:

$BTC · $ETH · $BNB · $XRP · $SOL · $TRX · $DOGE · $HYPE · $ZEC · $ADA · $XMR · $BCH · $LINK · $TON · $XLM · $LTC · $SUI · $AVAX · $HBAR · $NEAR · $TAO · $DOT · $UNI · $ONDO · $WLFI · $ASTER · $ICP · $MORPHO · $AAVE

Our analysis window was 16 days ending 26 February 2026, and the pairs we tested were: Hyperliquid vs Binance, Hyperliquid vs Lighter, and Lighter vs Binance.

Full methodology can be found in the end.

What we found

Every analysis gave a consistent story:

For 29 of 29 assets: Binance led Hyperliquid

For 27 of 29 assets: Lighter led Hyperliquid

For 23 of 29 assets: Binance led Lighter

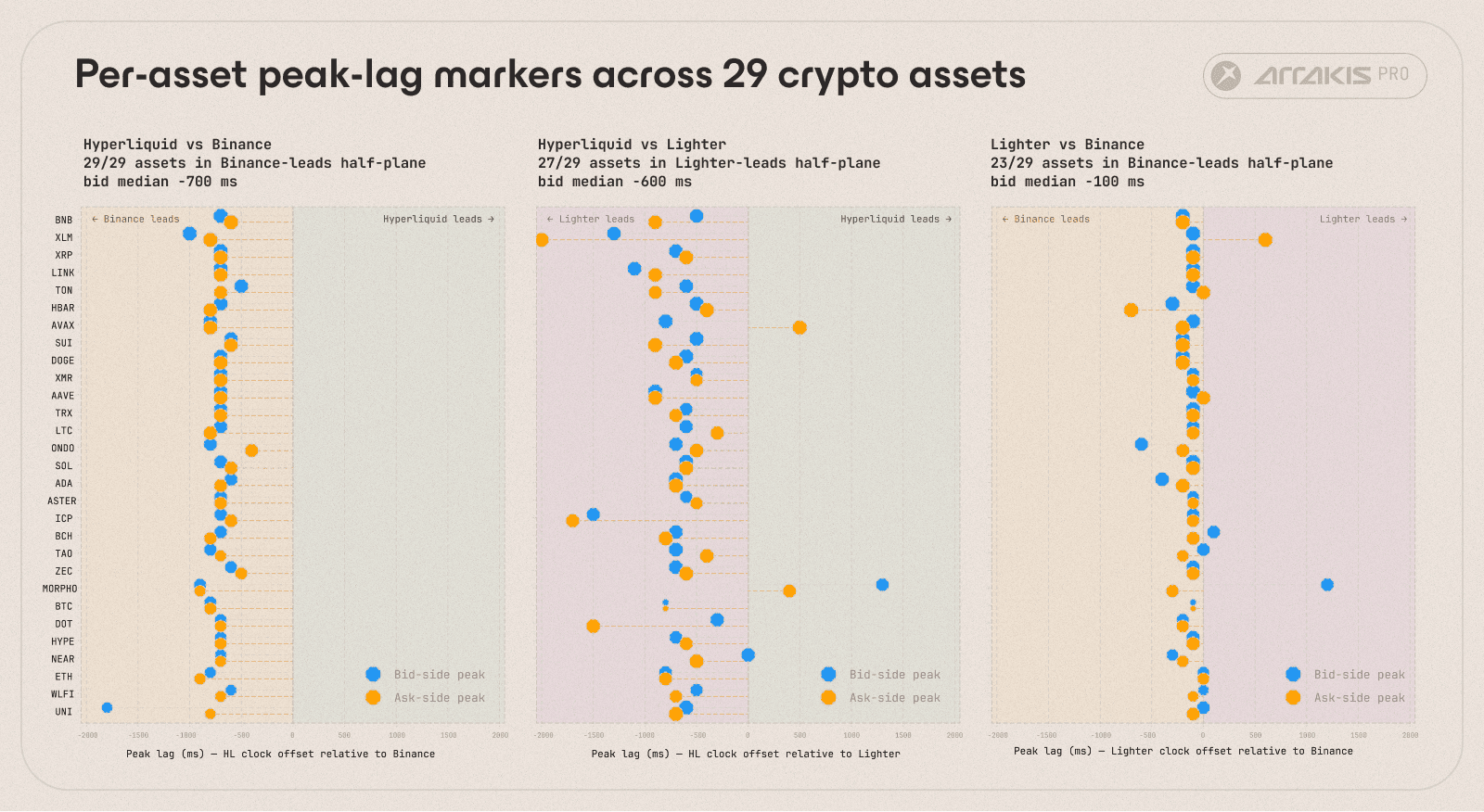

Per-asset peak-lag markers across all three venue pairs, same asset ordering across panels. The two Hyperliquid panels look nearly identical regardless of which venue is on the other side. The Lighter-vs-Binance panel collapses to a tight cluster at the negative-lag edge.

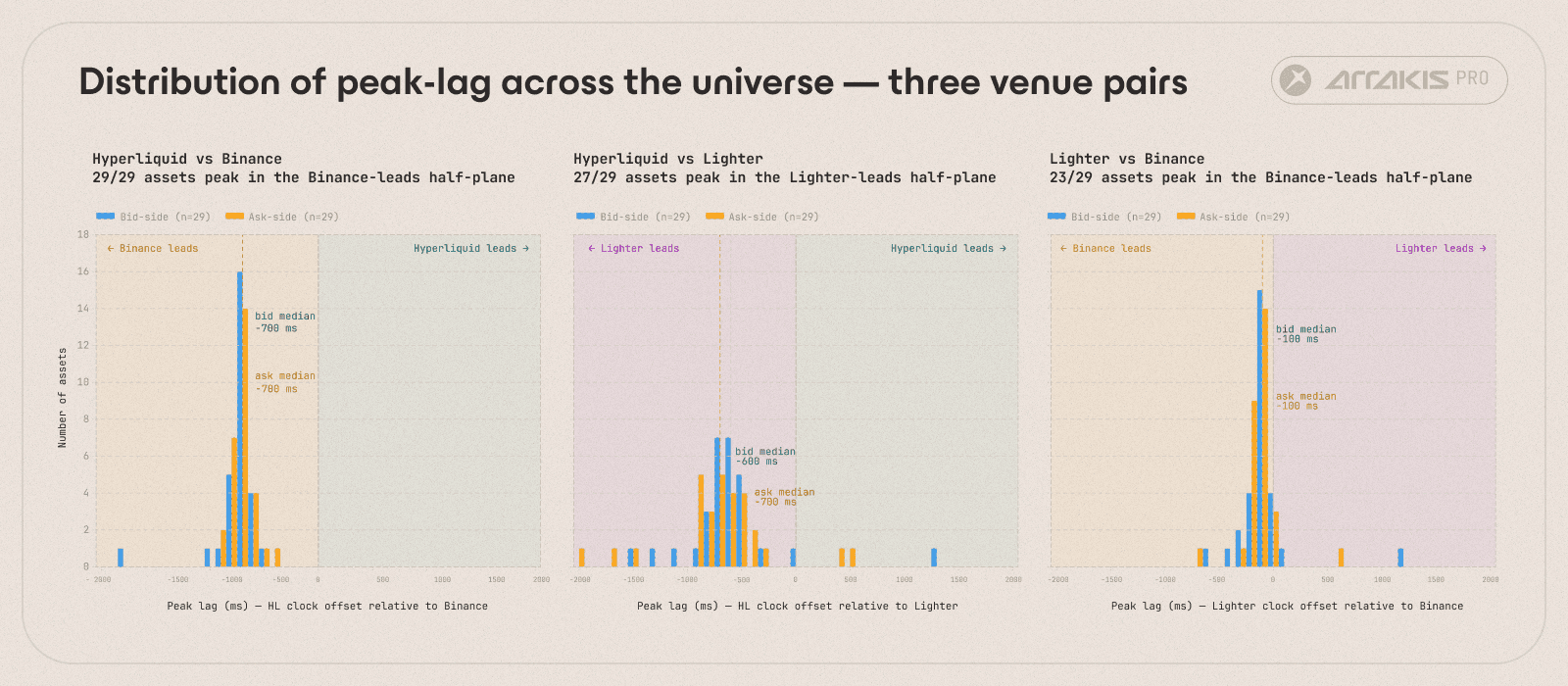

Distribution of peak-lag bins across the 29 universe assets, in 100 ms bins from −2000 to +2000 ms. Both Hyperliquid panels peak between −600 and −700 ms. The Lighter-vs-Binance panel peaks at −100 ms.

The two Hyperliquid panels look nearly identical: tight clusters around −700 ms regardless of which venue is on the other side. From Hyperliquid's perspective, Binance and Lighter had very similar latency, both lead it by roughly the same amount. The Lighter-vs-Binance panel sits an order of magnitude tighter, at around −100 ms, which was the smallest increment at which our analysis tested lead lag between the time series.

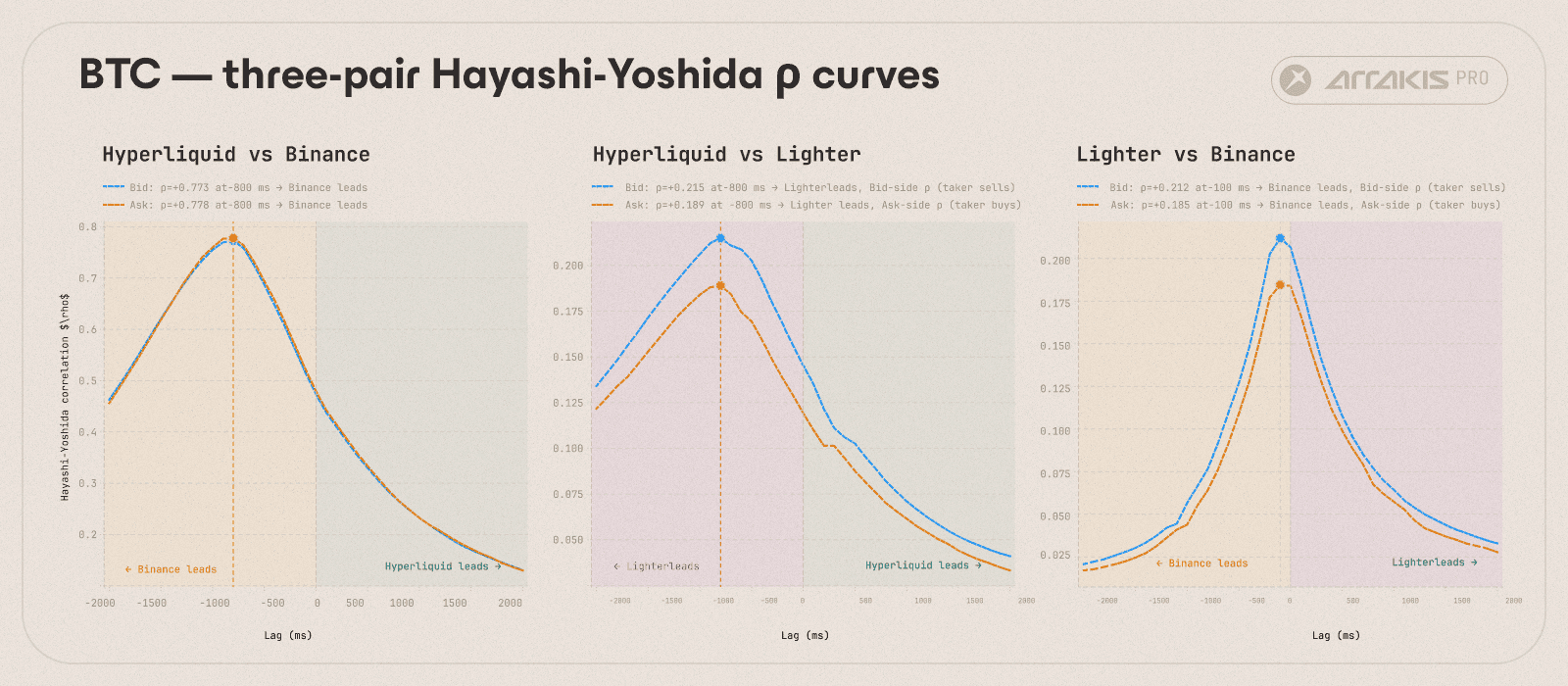

This can be clearly observed at a per-asset level when looking at BTC fills. Correlation consistently peaked for both Hyperliquid vs Lighter and Hyperliquid vs Binance at -800 ms, indicating that Hyperliquid lagged behind both of these venues consistently at those levels.

BTC ρ-vs-lag curves across all three venue pairs. The lag direction is consistent: −800 ms on both Hyperliquid panels, −100 ms on Lighter vs Binance.

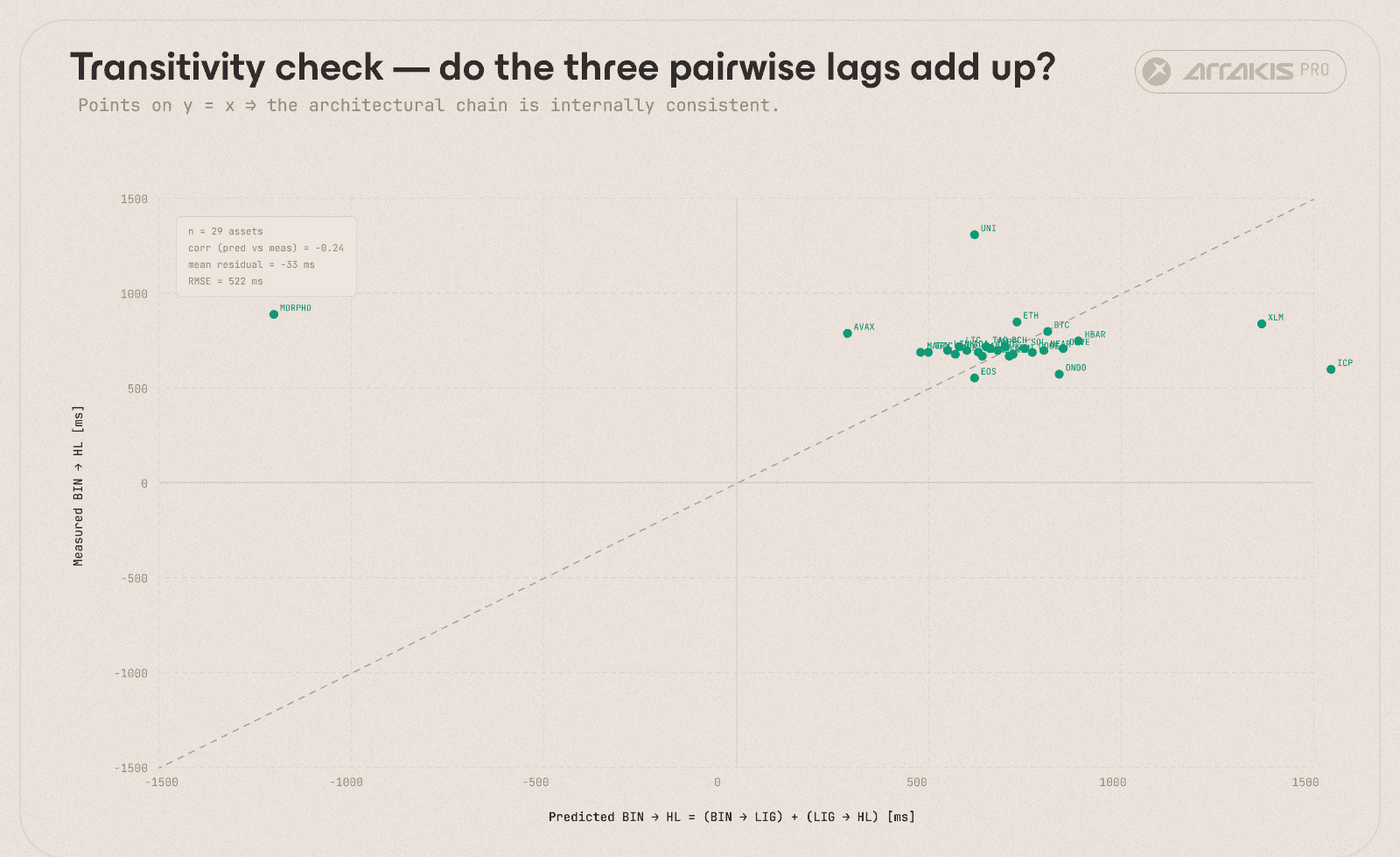

Transitivity check

If the three pairwise lags reflect the same underlying microstructure, they should be additive: Binance → Hyperliquid lag should equal (Binance → Lighter) + (Lighter → Hyperliquid). We checked this across the 29 markets we did this analysis on.

Predicted Binance → Hyperliquid lag (sum of Binance → Lighter and Lighter → Hyperliquid) on the x-axis vs measured Binance → Hyperliquid lag on the y-axis. Each point is one asset. Universe median residual is −33 ms.

The median residual was only −33 ms, indicating that transitivity for these assets held. The outliers (MORPHO, ICP, XLM, UNI) were noisy because their lag-correlation curves never properly peak inside our ±2000 ms window. Our estimator couldn’t pin down a clear lead-lag number for them.

Every other market held to the transitivity relationship. That consistency suggests the lead-lag is structural to how these venues match and settle, not an artifact of any single pair.

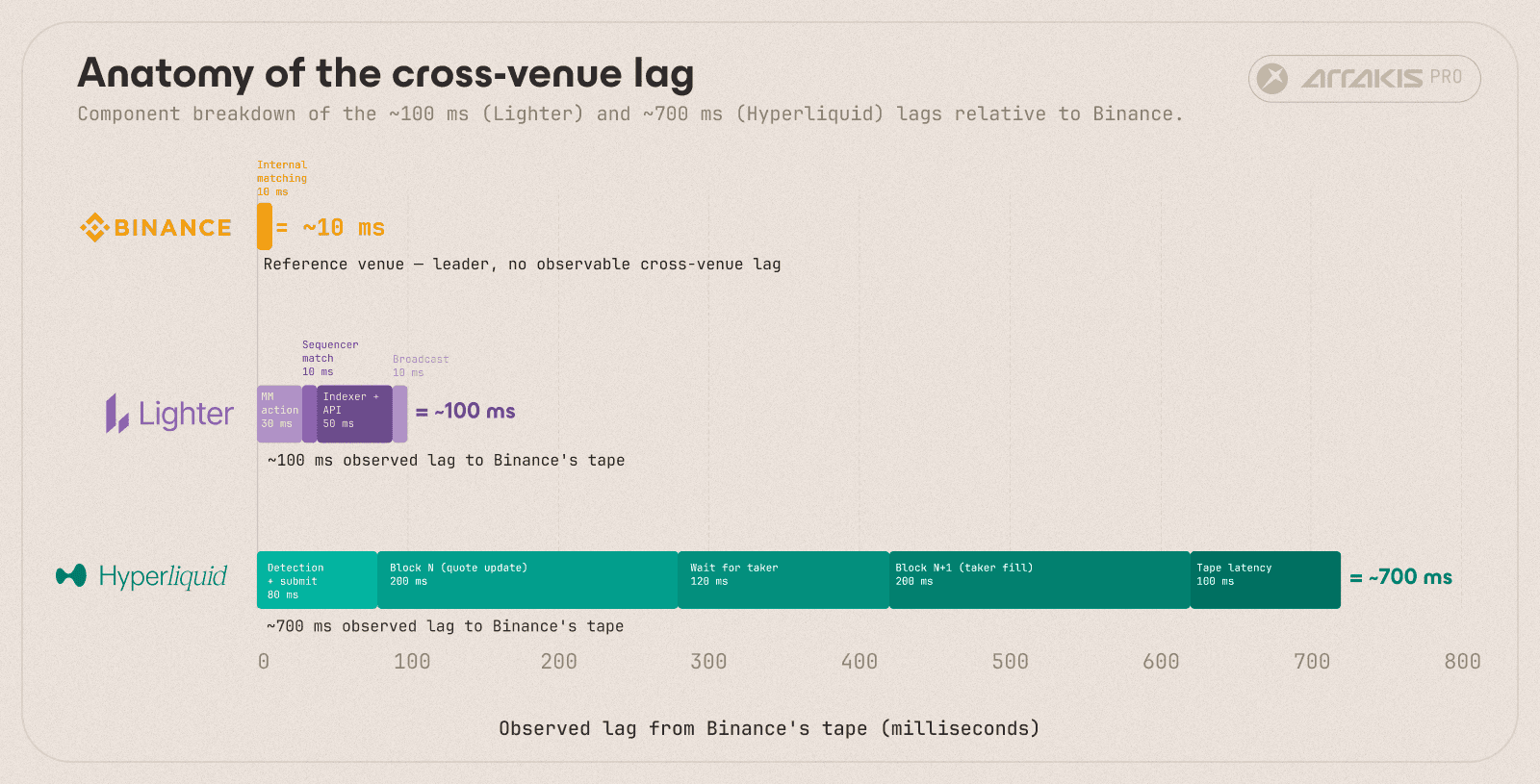

Where does Hyperliquid's lag come from?

The three venues run three different matching architectures.

Anatomy of the cross-venue lag. Binance is the reference. Lighter's ~100 ms lag is essentially the Sequencer → Indexer → API pipeline. Hyperliquid's ~700 ms lag is dominated by two full HyperBFT consensus cycles, one for the maker quote update (Block N), one for the organic taker fill (Block N+1).

Venue | Architecture | Internal matching | Lag to Innovation |

|---|---|---|---|

Binance | Centralized in-memory C++ CLOB, FIFO | ~5 ms | ~10 ms (reference) |

Lighter | Off-chain Sequencer + zk-rollup. Matching off Ethereum, proofs settle later. | Sub-ms to low-ms | ~100 ms |

Hyperliquid | On-chain CLOB inside HyperCore. Matching is the state transition executed inside HyperBFT consensus. | Fast internally, gated by block finality | ~700 ms |

Binance and Lighter both match in-memory in milliseconds, while Hyperliquid's matching is the HyperBFT state transition itself, so every fill waits for ~200 ms block finality (per Hyperliquid's official docs). But the observed lag in fills is ~700 ms, not ~200 ms. The extra ~500 ms come from a maker-taker round-trip layered on top of single-block finality.

The most plausible explanation is a maker-taker round-trip that spans two consecutive blocks. Here is the sequence after a price move on Binance:

Stale liquidity sits on Hyperliquid. Resting market-maker quotes are mispriced relative to the new price on Binance.

The mempool race. Arbitrageurs spam IOC orders speculatively, targeting expected stale liquidity. Market makers fire cancel-and-replace transactions to refresh quotes. Whoever reaches the block proposer first wins.

Block N commits at ~200-300 ms. Cancels remove the stale quotes that market makers got to in time. New orders post refreshed quotes. Surviving IOCs hit residual stale liquidity at the old price, hence fills in this block mostly occur at the stale price relative to Binance.

The Hyperliquid book is now clean, but no one has traded against the refreshed quotes yet.

Takers start trading at the now updated price.

Block N+1 commits at ~500-700 ms. The taker matches a refreshed quote. This is the first fill carrying new price information, and what our estimator picks up correlating with Binance’s lagged price innovation.

This implies it takes at least two full HyperBFT cycles for a price move on Binance to surface in fills on Hyperliquid.

By contrast, Lighter skips this entirely. Its Sequencer matches in-memory; a quote update and a fill against it happen in the same millisecond. The ~100 ms lag reflects the latency around the Indexer and API and is also the lowest granularity at which we were incrementing lead-lags in our estimator.

What Lighter proves

Lighter's pricing follows Binance's closely, with a small lag relative to Hyperliquid. This falsifies the assumption that "Hyperliquid lags because it's a DEX" as lighter is also a DEX. Orders flow into a centralized off-chain Sequencer, but the system as a whole is verifiably decentralised via zk-proofs settled to Ethereum.

The difference is where decentralisation is enforced. Hyperliquid enforces it at the matching layer: with every order, cancel, and fill committed by the validator set, while Lighter enforces it at the settlement layer: the Sequencer matches in-memory, then proves correctness to Ethereum after the fills.

Lighter buys speed by relocating the trust boundary from matching to settlement. Hyperliquid keeps the trust boundary at matching and pays for that in latency.

What Hyperliquid could do

These are a few changes to its current design Hyperliquid could make in order to improve in its pricing lag against discovery venues like Binance.

Tighter HyperBFT pipelining. Push below the 200 ms median through tighter leader rotation, parallel voting, or networking optimizations. Each shaved millisecond compresses both blocks in the round-trip. Although this doesn’t get rid of the structural reason this lag exists, any material improvement in block time improves the price lag several-fold.

Pre-confirmation or soft-finality layer. A separate fast path that pre-confirms block inclusion, with HyperBFT finality arriving asynchronously. Market makers post quotes against pre-confirmed state and the effective tick latency drops. The trade-off: pre-confirmations are credible commitments requiring either trusted infrastructure or slashing-backed bonds. Both reintroduce trust assumptions that Hyperliquid currently does not have.

Decoupling matching from consensus. The most ambitious and costly. Run an offchain fast matching layer that produces preliminary fills, then batch-commit them to consensus, structurally closer to Lighter's design. The latency floor compresses with this dramatically, but the trust assumption changes substantially from the current laissez-faire validator model.

Each path requires intrusive changes to the architecture at different levels and introduces trust assumptions not currently present in the system. Whether the latency these methods improve is worth the added trust assumptions they introduce is a question for the team and community to decide.

What this means

Hyperliquid has established itself as the leading PerpDEX across liquidity, open interest, and retail participation. It is pioneering a unique frontier in DeFi by introducing novel markets that do not exist in TradFi: weekend trading of stocks and commodities, pre-IPO equity perp markets, outcome markets on inflation, and others.

But as the market matures and more players enter, the next round of onchain perp competition will be fought on the latency frontier. Hyperliquid built the most liquid venue on a decentralised onchain matching engine. The open question is whether it can hold that design while remaining the leading price-discovery venue for the novel markets it has introduced.

Methodology details

Why a regular-grid estimator fails

The intuitive way to measure cross-venue lead-lag is to sample both tapes onto a shared 1-second grid and run a regression. Trades on the two venues do not happen at synchronised instants, and that breaks the assumption the regression rests on.

Suppose Binance prints at 10:00:00.998 and Hyperliquid's most recent fill was at 10:00:00.612. A last-in-bin sampler at the 10:00:01 boundary treats both prices as contemporaneous, even though Hyperliquid's is 386 ms older. At the sub-second lags we want to measure, that misalignment sits on the order of the effect itself.

The Hayashi-Yoshida estimator avoids the grid entirely. It pairs every Binance return with every overlapping Hyperliquid return on each venue's own tick clock, weighting each pair by the length of its overlap.

The HY formula in detail

For two return series indexed by their native tick intervals, the cross-covariance is:

Two return intervals enter the sum only if their wall-clock ranges overlap. The correlation at a candidate time-shift τ is:

is the second series shifted by τ milliseconds.

A worked example. Suppose Hyperliquid prints two fills: HL_A spans 10:00:00.100 → 10:00:00.400 and HL_B spans 10:00:00.400 → 10:00:00.900. Binance prints four fills in the same window: BIN_1 through BIN_4, with intervals .050-.200, .200-.450, .450-.700, and .700-.950.

At τ = 0, HL_A overlaps with BIN_1 and BIN_2; HL_B overlaps with BIN_2, BIN_3, and BIN_4. Each overlapping pair contributes its return product to the covariance. Shift Binance's clock by τ = +500 ms and the overlap geometry changes, some pairs drop out, others appear, and ρ(500 ms) is computed on the new overlap structure.

We scan τ from −2000 ms to +2000 ms in 100 ms steps. The peak in |ρ| is the lead-lag.

Side-separated fills

Cross-venue noise at sub-second resolution is dominated by bid-ask bounce. A venue's last trade flips between bid and ask on its own internal flow, even when the underlying mid has not moved. Running HY on raw fills mixes that bounce into the cross-venue signal.

We split each venue's tape into two streams. Bid-side fills are aggressor sells. Ask-side fills are aggressor buys. Within a stream, prices walk only one side of the book. We run HY independently on each side. For most of the universe, both sides agree to within one bin (100 ms).

Caveats and limitations

100 ms is the resolution floor. The shift grid is 100 ms. The estimator cannot resolve a lead-lag shorter than that. The 100 ms peak on Lighter vs Binance may be an upper bound on the true Lighter lag relative to Binance.

Local stationarity. HY is unbiased for two co-integrated price series with stable noise structure over the estimation window. Across 16 days, volatility regimes shift and liquidity migrates intraday. We read the headline peak as a representative value over the window.

Peak ρ above 1.0 on thin tapes. On a small number of low-liquidity assets the estimator returns ρ > 1.0 at the peak. This is a known small-sample artefact of HY under heavily asynchronous tapes (Hayashi-Yoshida 2005, §3): the numerator can grow faster than the denominator product when overlap structure is sparse. The lag direction stays robust; ρ magnitudes on these assets should be read as ordinal within the pair.