Research

Hyperliquid

This article is published for informational and educational purposes only and does not constitute investment advice. Arrakis has made reasonable efforts to verify the accuracy of the data presented but does not warrant that all information is accurate, complete, or current.

Thank you to 0xArchiveIO, HyperTracker (by Coinmarketman), and Stacy Muur for their contributions to this research.

Abstract

When we wrote our first article on ‘Who’s trading on HIP-3’, the attribution was statistical. We classified each wallet based on their trading behaviour over past 3 months: addresses with maker-dominated were classified market makers, addresses with high-frequency taker activity were classified arbitrageurs, addresses with low fill rates and builder tagged orders were deemed retail. While this revealed interesting pattens in the market structure, this classification was probabilistic, and the method left roughly 70% of wallets in the market unclassified.

This piece replaces statistical inference with mechanical classification. Every order on Hyperliquid carries a deterministic set of tags that the exchange itself signs and publishes: time-in-force (ALO, GTC, IOC, FrontendMarket), builder code, fill flag, hold time. We used this order metadata to classify each wallet into one of four buckets: Retail, Market Maker, Arbitrage Bot, or Airdrop Farmer.

The second step identified the wallets behind these buckets, pulling identity and trading-behaviour data from the Arkham and HyperTracker APIs. The top 450 wallets carry 78% of total volume. Within that set we identified several Polymarket-associated handles, Jump Crypto, Selini Capital, Wintermute, Abraxas, and others.

Several patterns emerged from this two-step classification. We examine them in detail below.

The Wallets

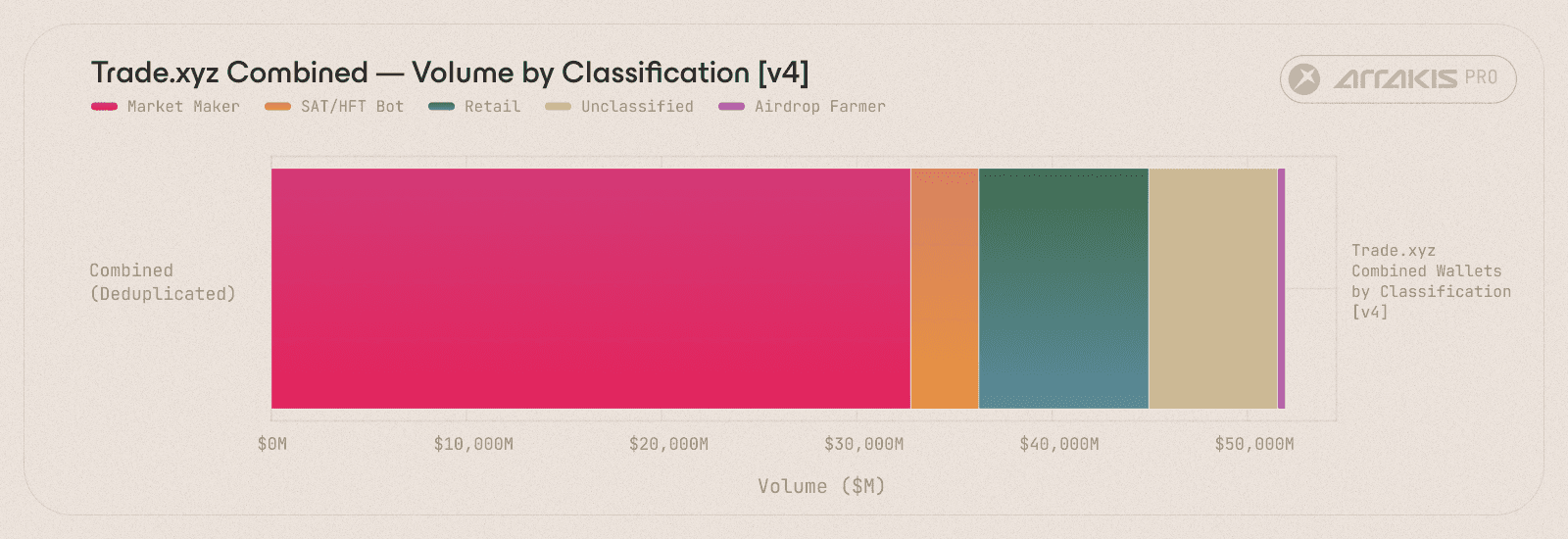

We observed a period of 21 days, from 10 March, 2026 to 31 March, 2026. Across that period, the four Trade.xyz markets (xyz:CL for oil, xyz:SILVER, xyz:TSLA, and xyz:XYZ100) recorded 79,622 unique participating wallets and $51.95B of aggregate volume.

The 79,622 participating wallets across 21 days, decomposed by trading volume. Market makers carry 63% of every dollar despite representing under half a percent of the wallets.

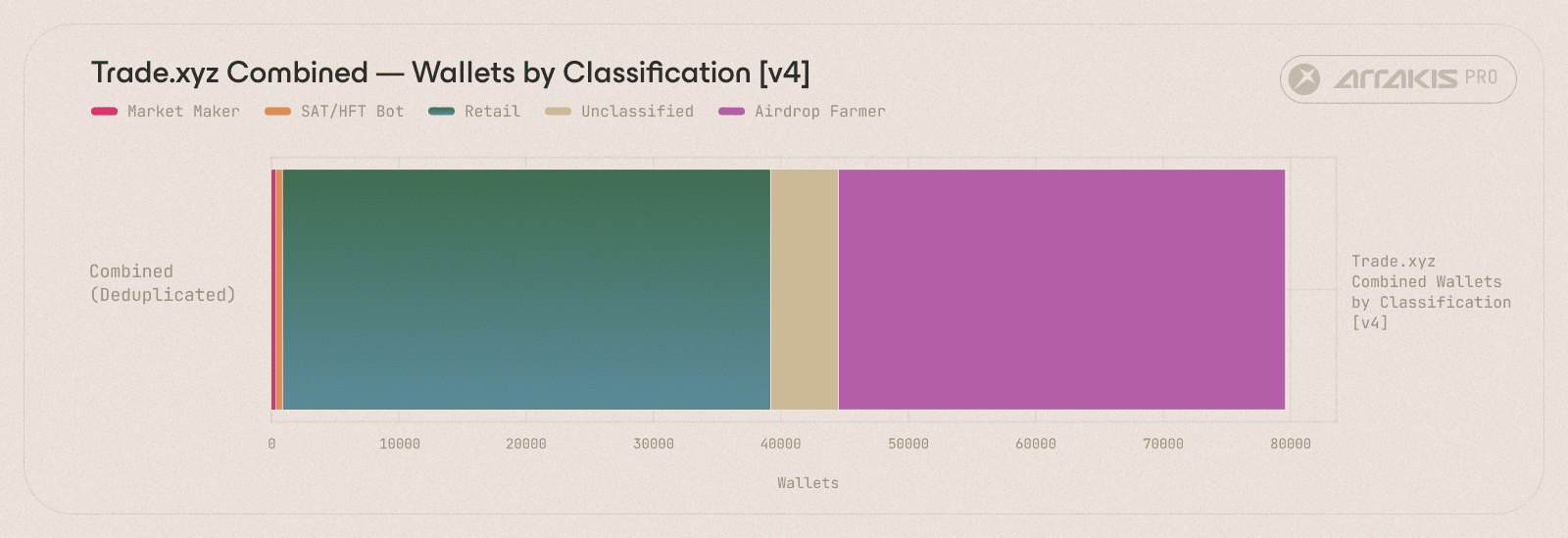

Wallets classified by number of wallets instead of volume. The Airdrop Farmer bucket alone holds 35,091 wallets, almost half of the total number of wallets identified.

The Airdrop Farmer bucket was one of the largest classifications by wallet count and the smallest by volume share. 35,091 wallets represented 44.07% of the total wallets but generated only $0.40B in trade volume across the window, or 0.77% of the venue's $51.95B total. Nearly half of all active wallets on Trade.xyz produced under one percent of the total volume in the market.

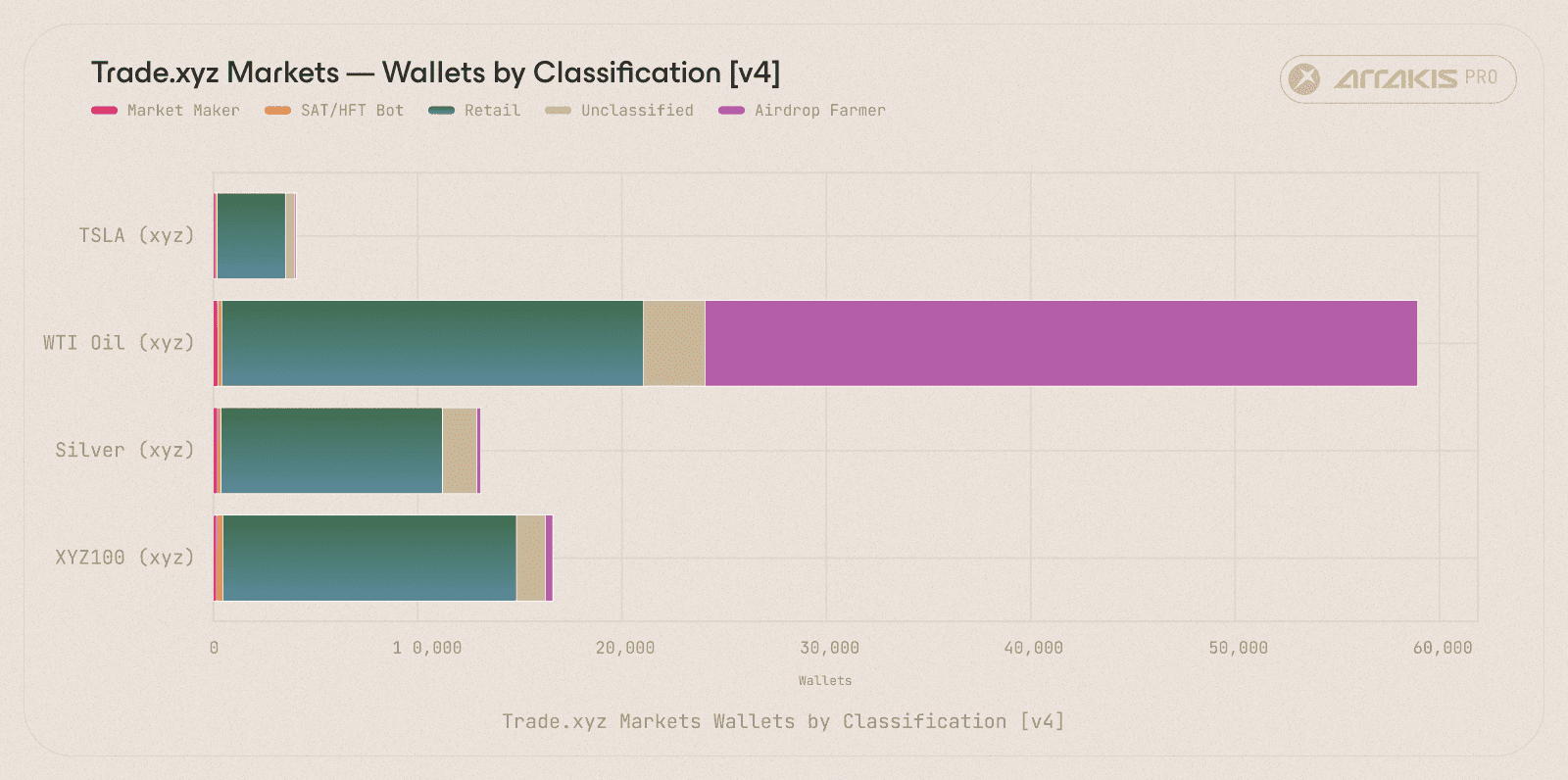

Breaking them down by the market they participated in reveals another striking pattern.

Wallet population split by market. xyz:CL absorbs 99.3% of the Airdrop Farmers due to best execution.

Of the 35,091 wallets in the Airdrop Farmer bucket, 34,859 (99.3%) traded xyz:CL during the window. The remaining 232 wallets are spread across xyz:SILVER, xyz:TSLA, and xyz:XYZ100. This pattern is consistent with airdrop farming: each wallet places small back-to-back trades in both directions, registering volume without taking on price risk. This approach depends on tight execution costs and benefits from minimal slippage. xyz:CL was the deepest of the four Trade.xyz markets, which makes it a natural venue for the activity.

Another interesting observation was who was behind these addresses. The onchain trace presented later in the piece links 34,553 of those farmer wallets to a single Polymarket operator. That entity alone accounted for 43.4% of all participating wallets on Trade.xyz over the window.

At the opposite extreme of this classification was market making. 363 wallets, or 0.46% of the total active addresses, moved $32.75B during the window: 63% of every dollar traded on Trade.xyz. The three remaining categories occupied the space between. 522 SAT/HFT bots ran $3.50B (6.7% of volume). 38,307 wallets classified as Retail moved $8.70B (16.7%). 5,339 wallets in the Unclassified bucket accounted for $6.61B in volume (12.7%).

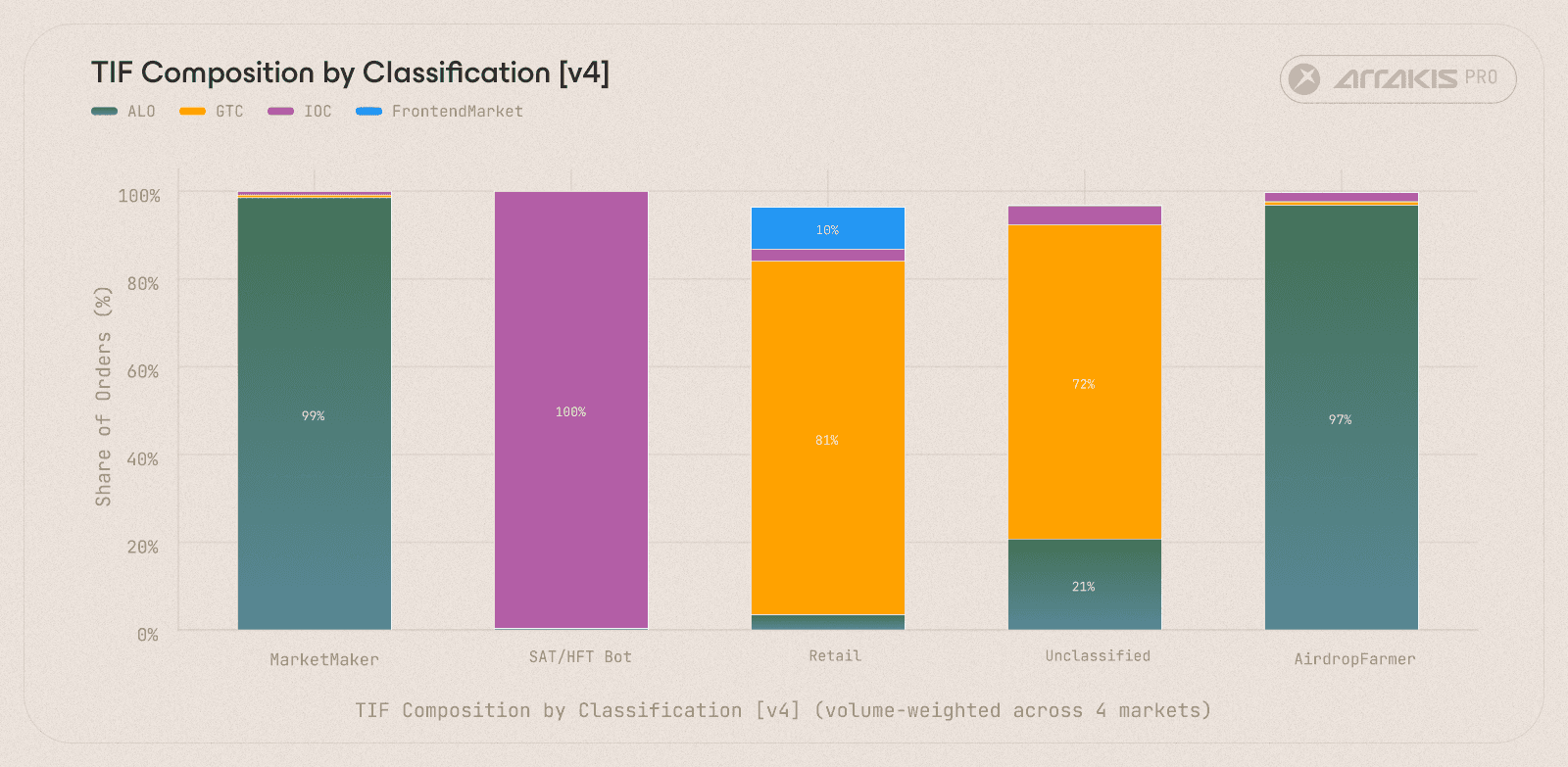

The 12.7% of volume sitting in Unclassified cannot be assigned to a definitive strategy from the metadata alone. It's reasonable to assume that a meaningful share of this volume reflects retail participants placing limit orders through the Hyperliquid frontend, or market and limit orders through the Trade.xyz frontend. Since, neither of these channels attach an explicit builder code or dedicated TIF tag to these type of orders, leaving these fills invisible to a metadata-driven classification.

Time-in-force mix by category, weighted by order count. Unsurprisingly market makers run 98.5% ALO and Arbitrage bots do 100% IOC orders. The Unclassified bucket leans 71.5% GTC, the signature of frontend participants resting limit orders manually.

The TIF composition supports this assumption, 71.5% of the orders aggregated into the unclassified bucket carry the GTC (Good Till Cancel) time-in-force, a tag that is typically used by frontend participants posting resting limit orders.

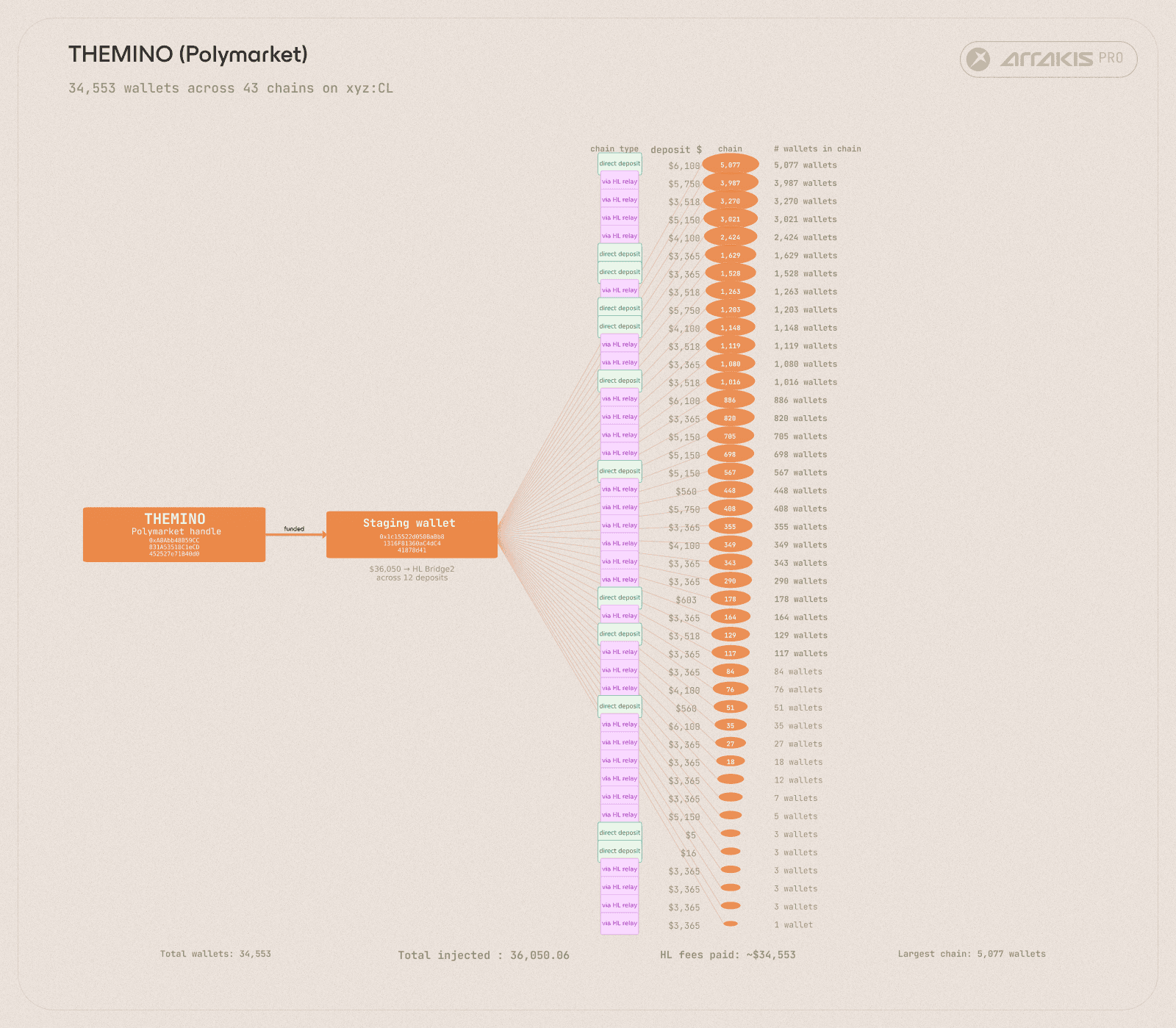

Meet Themino. And Themino. And Themino.

Over the past few weeks there has been considerable discourse on whether Trade.xyz's headline user count reflects genuine human participation, or whether it has been inflated by airdrop-farming activity in anticipation of the venue's expected TGE. While we are not in a position to comment on the broader landscape of farming behaviour across the venue, upon analysing the fill-level data for the four Trade.xyz markets in March, it surfaced one pattern worth presenting.

Out of 34,553 of the 34,602 wallets classified as Airdrop Farmers, 99.9%, trace back to a single Polymarket identity going by the handle "Themino".

The Themino complex. One Polymarket Arbitrum identity seeds 70 distinct linear chains spanning 34,553 farmer wallets.

How this worked. Hyperliquid's L1 has an internalTransfer primitive that moves USDC wallet-to-wallet for a flat $1 fee regardless of amount. Themino's operator used that primitive to walk a single seed deposit through tens of thousands of fresh wallets. Each wallet ran the same five-step sequence in roughly 26 seconds:

Receive $X from the previous farmer wallet via internalTransfer, losing $1 to the HL transfer fee on the way in.

Send $14 into the xyz sub-account.

Execute two IOC orders on xyz:CL, one buy and one sell, generating two fills and roughly registering some trade volume.

Send ~$13.99 back to the main account (the cent gap assumes execution slippage and trading fees).

Send $X minus 1 onward via internalTransfer to the next farmer wallet.

The next wallet then repeats the sequence.

Across the operation's 34,510 internal-transfer events, Themino lost $34,510 in protocol fees, a pattern consistent with their Polymarket trading history.

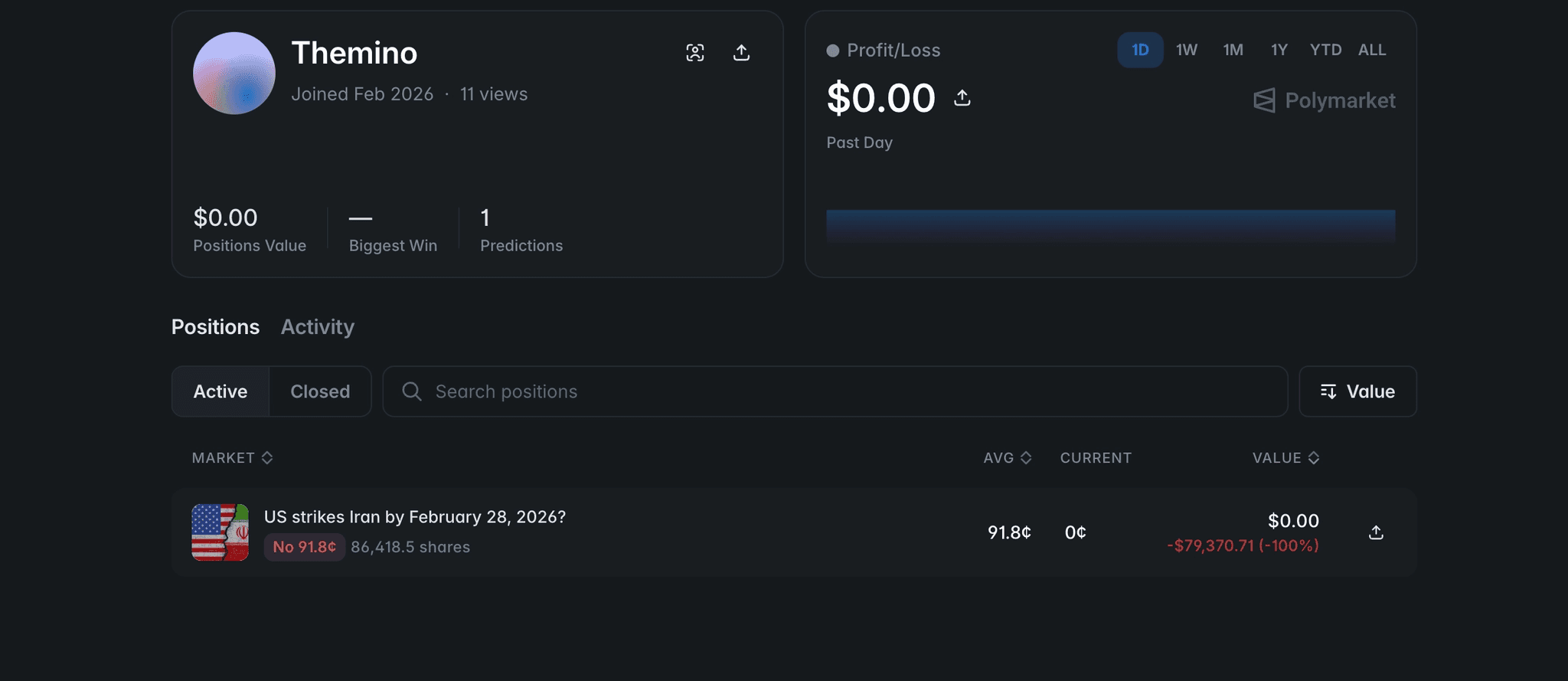

Themino also lost ~$80k betting no on "US strikes Iran by February 28, 2026?" on Polymarket. The strikes happened on February 28.

Farmer wallets | 34,553 |

Distinct chains | 70 |

Largest chain | 2,886 wallets |

USDC moved farmer→farmer | $79.72M across 34,510 events |

Actual xyz:CL trade volume generated | $860K |

External capital Themino injected | ~$36,050 |

HL protocol fees extracted | ~$34,510 |

Cost per fake-user | ~$1 |

% of total wallets on Trade.xyz | 43.4% |

The builders

Hyperliquid attaches an identifier to orders routed through third-party frontends to enable apps to charge custom frontend fees. This identifier is the builder code, and it is the most direct read on which interface a wallet traded through, if any. Across the wallets that traded on the four markets, the builders can be grouped into three archetypes.

Algorithmic Builders. These are products that retail users use to maximise their volume on DEXs to farm points for potential airdrops. Before late 2025, farming on a perp DEX meant wash trading or non-directional taker-taker orders run algorithmically, these were not only costly for the participant but also net negative for the exchange. Retail market-making bots like Tread.fi and Planemo replaced wash trading with valuable market making. Each order through these products is post-only, so the wallet adds liquidity to the book rather than consuming it.

As David, founder of Tread.fi, put it:

"Before retail market-making solutions existed, farming on perp DEXs meant wash trading, inflating volume at the cost of execution fees, slippage, and risking a ban. We solved this by building a novel farming solution: bots that would only quote maker orders on both sides. Users pay lower costs to farm, often making money on the spread they capture, and the by-product is genuine top-of-book liquidity for the market, exactly what HIP-3 equity perps need on nights and weekends when traditional market makers won't quote. It's a better way to farm, and the reason why HIP-3 markets have great execution today."

The contribution of these market making bots to the markets is clearest at the times traditional market makers are not quoting. CME's WTI futures close Friday afternoon and reopen Sunday evening, and equity perps face the same overnight-and-weekends gap. Across those windows, retail MM bots have populated the top of the book on xyz:CL, xyz:TSLA, and similar markets.

Note that while we classified wallets routed through these algorithmic products as Airdrop Farmers in this analysis, the trading behaviour and effect on the market is structurally different from sybil activity.

Builder | Wallets | Volume |

|---|---|---|

446 | $338M | |

Planemo Trading | 41 | $4.6M |

Origami Tech | 2 | $3.8M |

Wallet-integrated Builders are the perps interfaces embedded inside consumer wallets. Since the start of 2026, these integrations have collectively become one of the largest sources of retail orderflow on HIP-3. The group includes Phantom, MetaMask, Rabby, Rainbow, and OneKey. Median per-wallet volume sits between $1K and $3K, consistent with ticket sizes from a retail audience that values ease of access over the marginal builder fee.

Builder | Wallets | Volume |

|---|---|---|

Phantom | 6,297 | $355M |

MetaMask Perps | 1,454 | $93M |

Rabby | 599 | $49M |

Rainbow | 139 | $5.7M |

OneKey | 134 | $11M |

Apps are standalone perp frontends and integrations: trader-facing products that offer dedicated workflows for users who want more than a wallet plugin, including better order entry, charting, position management, and execution tools. The group sees fewer wallets than the wallet-integrated channel but higher per-wallet volume, consistent with a power-user base that values feature depth over plug-and-play convenience. Products include Insilico Terminal, Liquid Perps, Hyperdash, Based App, Dreamcash, Infinex, Pear Protocol, DefiApp, and pvp.trade.

0xVKTR, Head of Growth at Insilico, framed it like this:

"At Insilico, we see HIP-3 markets as the next step in making real-world exposure native to crypto rails. Traders do not just want another frontend. They want fast execution, clean market access, and the ability to move between crypto and macro assets without leaving their existing workflow. Trade.xyz has been one of the clearest examples of that demand. The flow routed through Insilico shows that there is a real power-user base for onchain perps when the venue has depth, the product is useful, and the trading experience is built for serious participants."

App | Wallets | Volume |

|---|---|---|

Based App | 375 | $182M |

Insilico Terminal | 142 | $104M |

Dreamcash | 886 | $43M |

Hyperdash | 209 | $29M |

Liquid Perps | 597 | $19M |

Infinex | 37 | $6.5M |

Pear Protocol | 72 | $5.1M |

DefiApp | 76 | $2.6M |

32 | $1.8M |

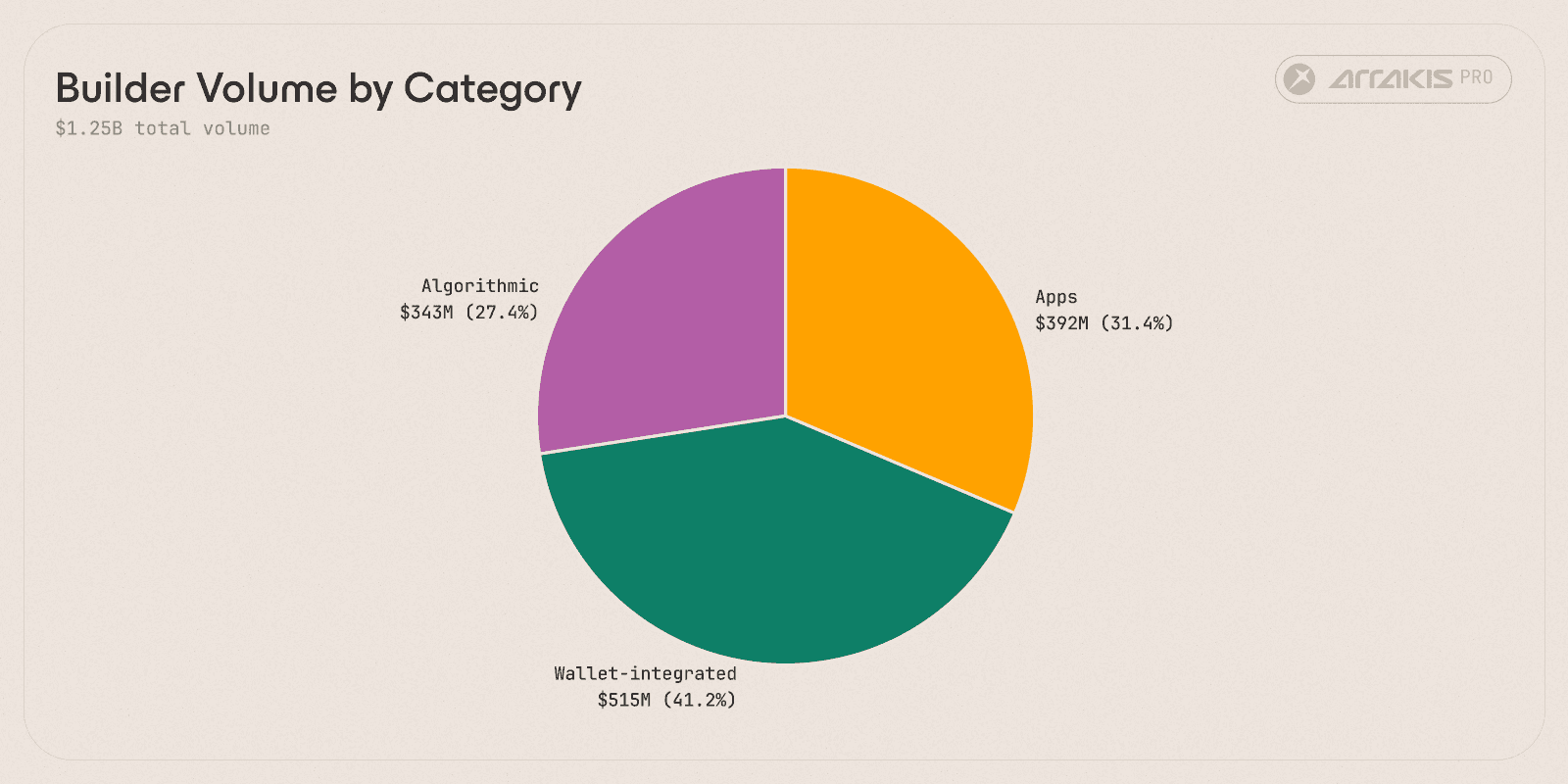

Builder Volume by Category

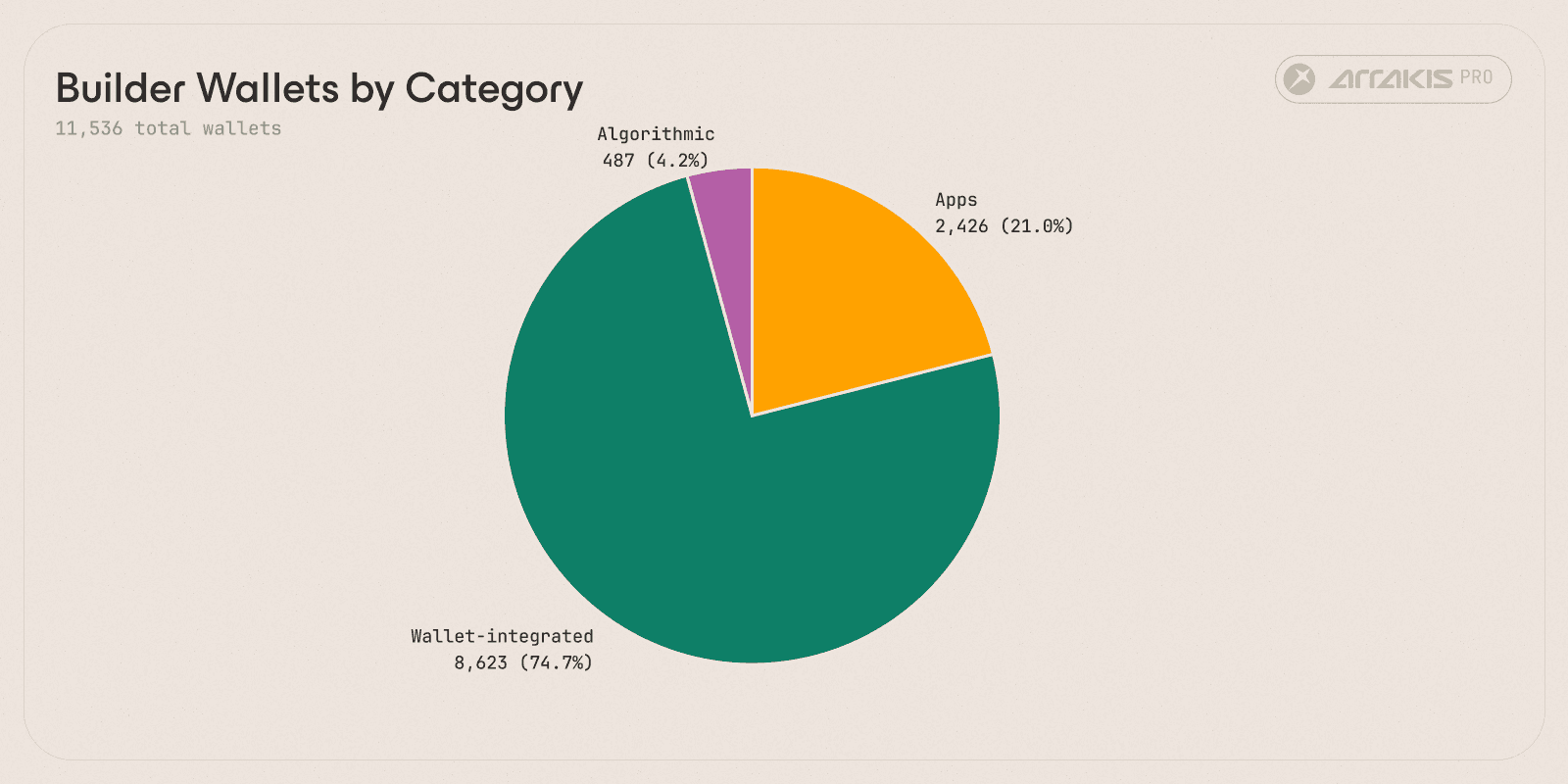

Builder Wallets by Category

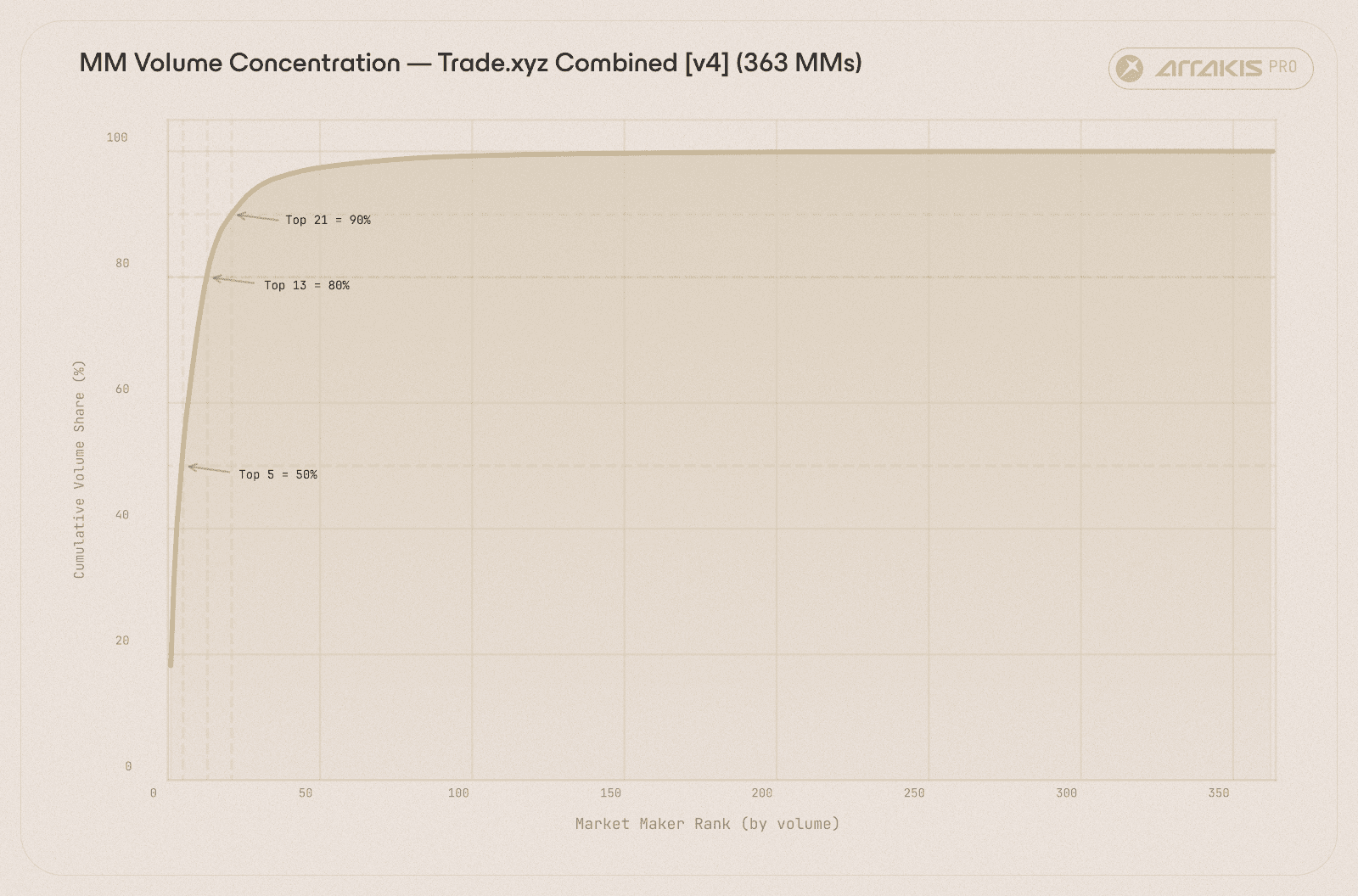

Market makers

The market making landscape on Trade.xyz markets was heavily concentrated. The top 5 market makers ran 50% of MM volume, the top 13 ran 80%, and the top 21 did 90%. A handful of desks processed the vast majority of the venue's MM book.

Cumulative share of MM volume by wallet rank. The top 5 desks ran 50% of all market-making flow, the top 13 reached 80%, the top 21 reached 90%.

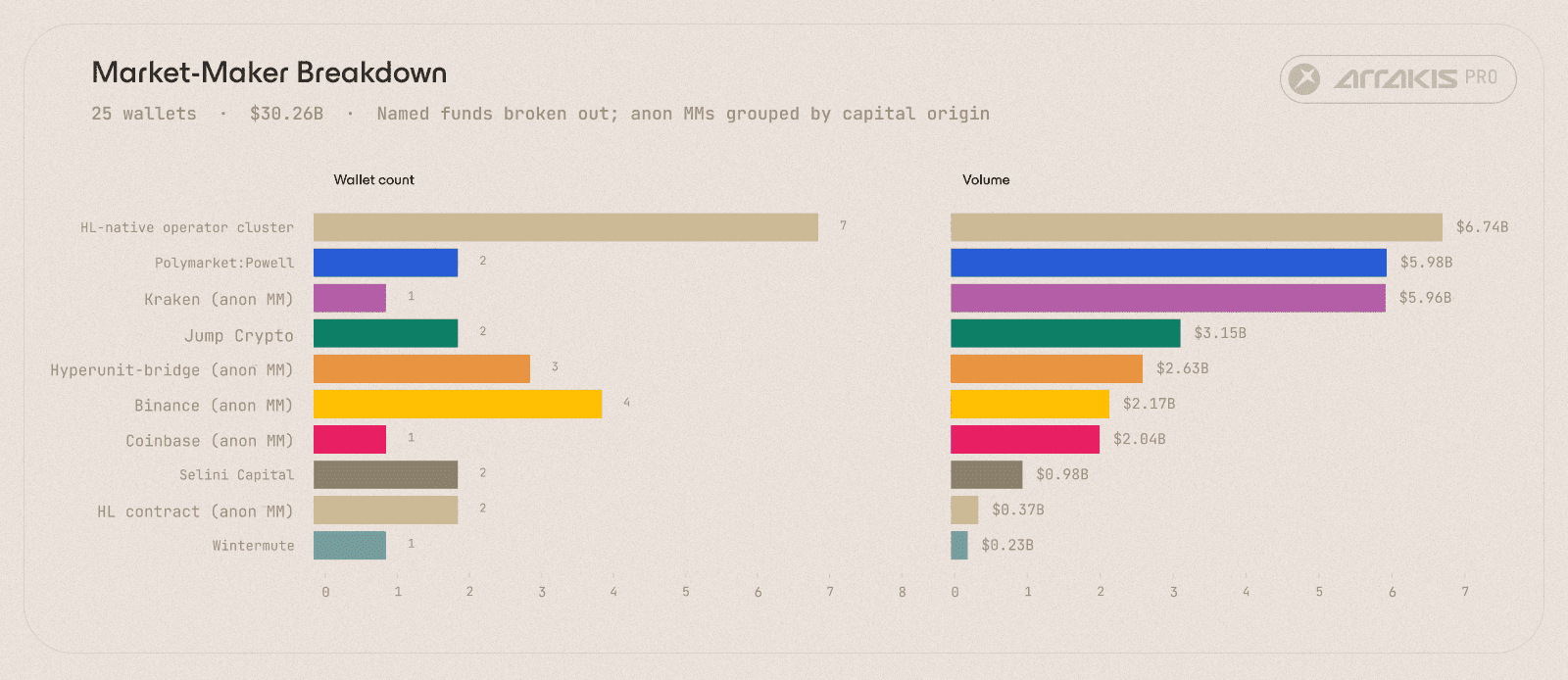

The 2nd largest MM was the single most interesting wallet in the entire cohort. 0xc926ddba…98d3 did $4.39B of volume at a 0.52% fill rate, a textbook maker profile. Arkham tags that address as "Powell" on Polymarket. One of the largest market makers on Trade.xyz was a Polymarket user running a multi-market quoting book on HIP-3.

A few other notable market making desks that surfaced were:

Jump Crypto ran two wallets totalling $3.15B, funded through 0xf584…d621, an Arkham-clustered Jump treasury wallet holding more than $160M in diversified inventory across LINK, LIT, EIGEN, BNB, ETH, USDC, and USDT.

Selini Capital ran three wallets: two running pure maker quoting (0x44a3e1…35dd, 0x76987c…4480) and one running pure aggressive taking (0x427be6…d1d9), all via API. Total Selini footprint: $1.03B. Hyperliquid's own orderflow tagging is what separates Selini's MM wallets from their HFT wallet. The same desk ran both sides of the book.

Wintermute ran one MM wallet at $229.6M (0xecb63caa…2b00), a smaller footprint than Jump or Selini. Capital origin was OKX.

Top market makers on Trade.xyz, ranked by volume. Powell, Jump Crypto, Selini Capital, and Wintermute occupy the visible-attribution share of the book.

Beyond the named desks, most of MM volume sits in wallets with no entity attribution but clean capital origins: Kraken, Binance, Coinbase, Hyperunit bridges, or HL-native funding. Their behaviour signatures are MM, but the operator behind the address never touched a labelled service that Arkham could stitch to an identity.

The median order-to-fill ratio for Market Makers was 19.4, so for every execution roughly 18 orders were placed and cancelled as part of two-sided quoting. The same top-5 MMs recur across all four xyz markets simultaneously, which means these were multi-market quoting desks rather than four separate businesses.

The MM liquidation rate during the window was 19.2%, almost matching retail's 20.4%. MMs on Trade.xyz carry directional exposure as their quotes fill: a large sell trade matching the bid leaves the desk long, a buy trade hitting an ask order leaves it short. During the March oil volatility, that accumulated inventory moved against the books faster than the desks could hedge, and a fifth of them caught at least one liquidation as a result.

Statistical Arbitrage Takers / Mid Frequency Trading Bots

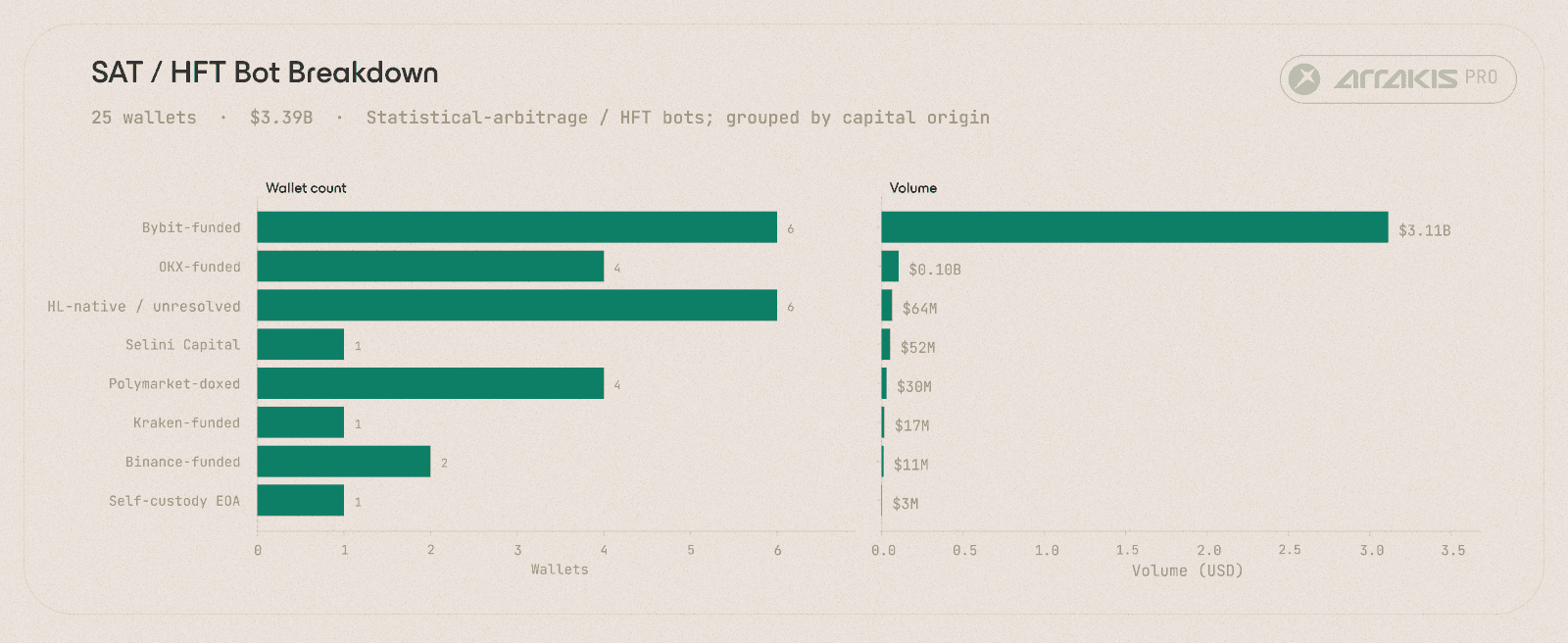

SATs are the counter-party to the MM book. These wallets run 90%+ IOC (Immediate or Cancel) order mixes, pure aggressive takers that lift and hit the MMs' quotes.

Top SAT/HFT bots ranked by volume. The top 4 wallets run 89% of the SAT book, with capital origins clustered on Bybit.

The top 4 SATs accounted for $3.1B of the $3.5B SAT book, an 89% concentration. Two of them ran 100% IOC, meaning every order they have placed was an immediate-or-cancel with no maker intent recorded.

Capital-origin clustering points the dominant SAT profile at Bybit. The majority of top-SAT volume traces back to Bybit-funded wallets, which is consistent with a single bot-operator entity or a small bot-operator community.

Three SATs carried Polymarket handles: loracles ($15.5M volume, +$25.7M lifetime HL PnL), Conduit ($5.3M), and ChadwickLongman ($3.7M). Polymarket surfaces here for the same reason it dominates the retail section below. The prediction-markets cohort is the single most common cross-venue identity on Trade.xyz.

The SAT liquidation rate during the window was 8.1%, roughly half the MM and Retail rates. The cohort is the most risk-managed category on the book. They hedge their positions externally and rarely catch margin calls.

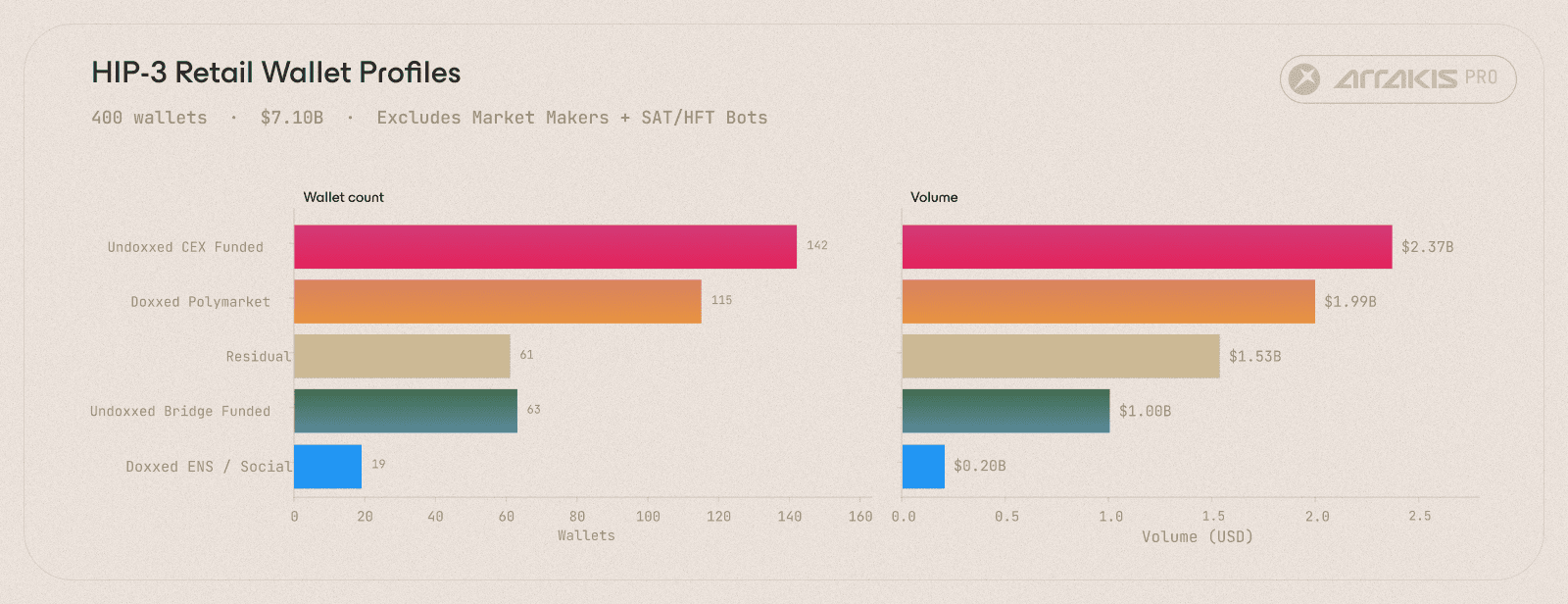

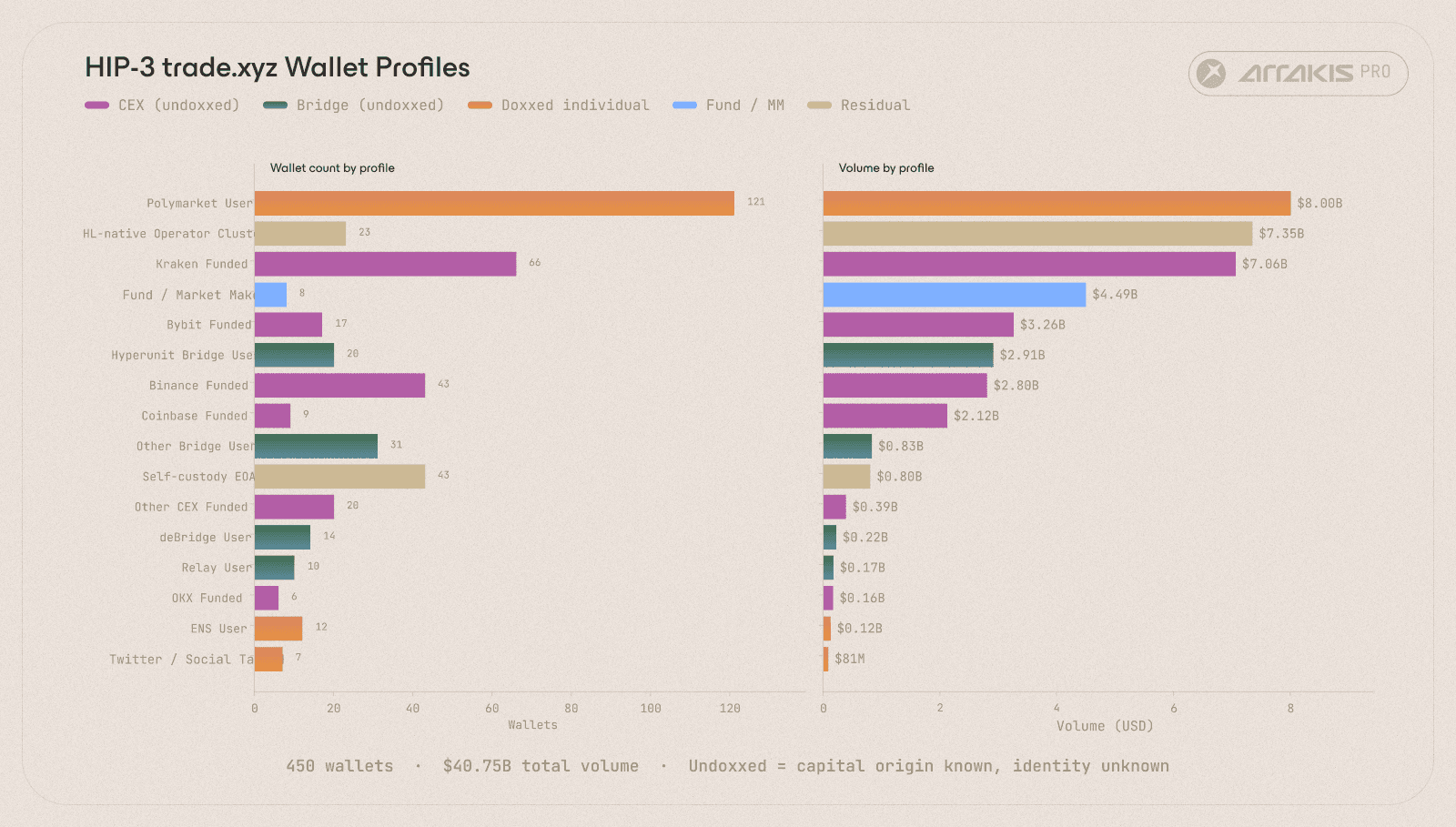

The Retail Cohort

We looked deeper into a subset of 400 top-volume wallets routing orders through the Hyperliquid UI and the builder-integrated frontends, excluding the algorithmic products covered earlier (Tread.fi, Planemo Trading, and the broader algo-builder cohort).

The 400 top-volume retail wallets split by attribution category. Polymarket-doxxed wallets dominate the doxxed share, contributing $1.63B of the cohort's volume.

Polymarket: identifiable Polymarket handles via Arkham's on-chain tag system.

ENS / Social: ENS names or other social-graph identifiers that do not trace back to Polymarket.

CEX-funded: anonymous wallets whose capital origin is a centralised exchange.

Bridge-funded: anonymous wallets funded via cross-chain bridges.

Residual: self-custody EOAs, contract infrastructure, and null-address activity.

The Polymarket share is the number that stands out. 94 of the 400 top retail wallets, 22% of top-retail volume ($1.63B), are verifiabe Polymarket users. This is the single largest identifiable cohort in the retail band. Combined with the Polymarket MM (Powell, $4.39B) and the three Polymarket SATs ($24M), the total Polymarket footprint on Trade.xyz is roughly $6B.

Selected Polymarket retail wallets in the top 15 by volume:

Polymarket handle | Volume |

Mandem | $141M |

skrskrprofitmuncher | $93M |

JonoElGrande | $80M |

tewojfowjei | $62M |

MichaelSolainor | $61M |

MTD (mistertodd.eth) | $60M |

cbalol | $55M |

asssdfc | $46M |

sorarespam | $44M |

GoldbergSilverman | $41M |

gigafree | $38M |

trumpwin24 | $34M |

eggnoodle (eggnoodle.eth) | $33M |

LiquidBaron | $29M |

The overlap makes sense. Polymarket and Trade.xyz offer crypto-native exposure to real-world outcomes through different market structures, prediction markets and perp futures, and the wallet-level data shows the same individuals running both books from the same EVM address.

ENS holders account for a further 26 retail wallets and roughly $400M combined. Notable wallets include caydenb.eth ($33M), eggnoodle.eth ($33M), ethmerg.eth ($19M), baitf1sh.eth ($16M), and wanyekest69.eth ($6.8M, with +$17.6M of lifetime PnL).

The unidentified buckets split by capital origin:

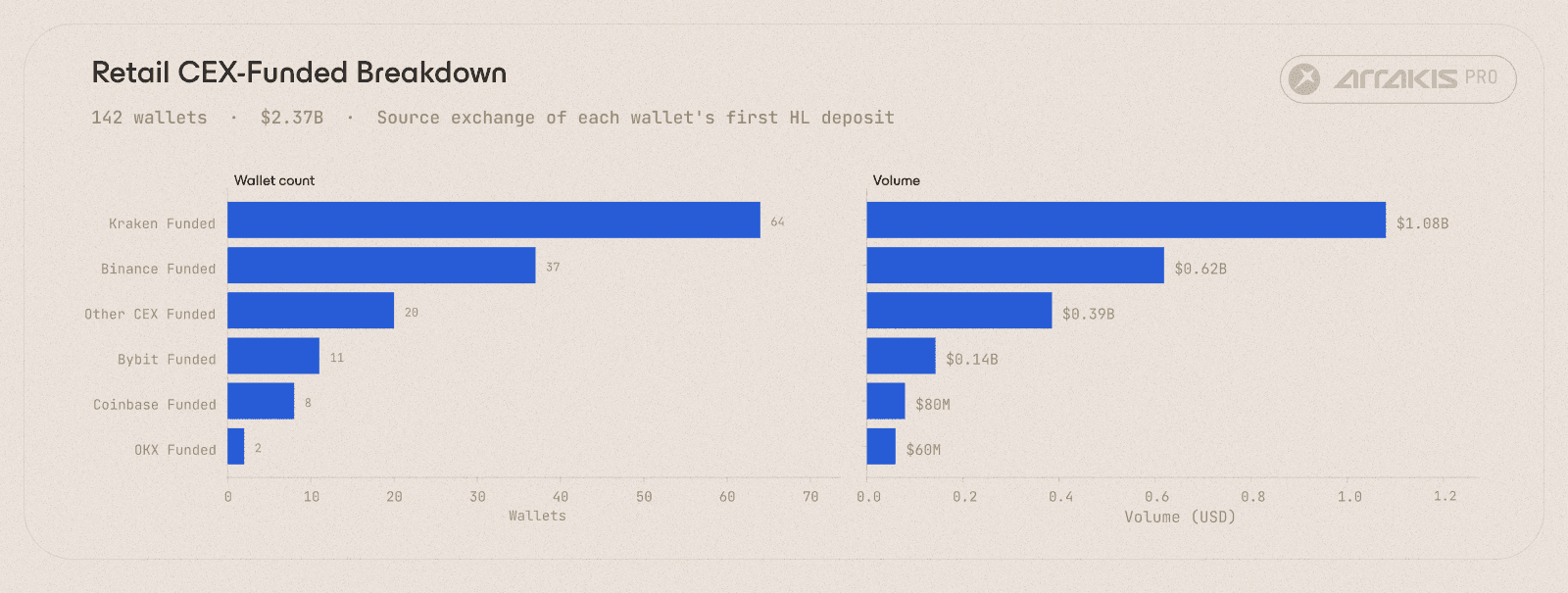

CEX-funded retail wallets by source exchange. Kraken dominates the undoxxed CEX-funded cohort by a wide margin.

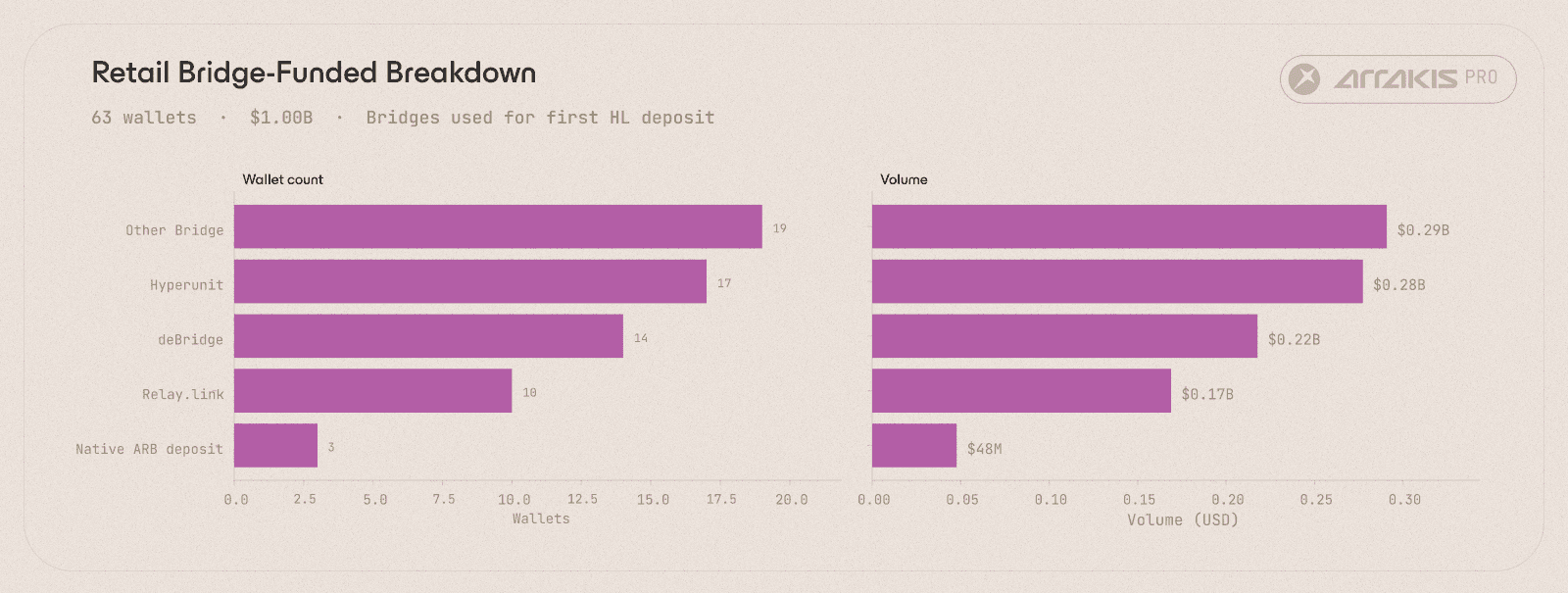

Bridge-funded retail wallets by source bridge. Hyperunit and deBridge dominate the bridge-funded cohort, with Stargate and a long tail accounting for the rest.

Kraken dominates the CEX-funded cohort. Hyperunit and deBridge dominate the bridge-funded cohort, with Stargate and a long tail of bridges accounting for the rest. The retail that actually moves Trade.xyz's order book is therefore three populations: Polymarket cross-over traders, Kraken-funded independent traders, and DeFi natives entering through Hyperunit or deBridge.

Rolling the MM, SAT, and retail cohorts back up into a single view gives the compact picture of Trade.xyz's participant base, stripped of the sybil layer that the next section covers.

The participant base after the sybil layer is stripped. A handful of professional MMs quoting against a handful of bot crews, with a long tail of Polymarket veterans and CEX-funded independent traders taking directional bets through the Hyperliquid UI.

A handful of professional MMs quoting against a handful of bot crews, with a long tail of Polymarket veterans and CEX-funded independent traders taking directional bets through the Hyperliquid UI. That is a consolidated view of the Trade.xyz book.

Methodology

The analysis combines four data sources. Hyperliquid's L4 order lifecycle data, pulled from 0xArchive, supplies one parquet per market with a row per order event. The relevant per-event fields are tif (one of Alo, Gtc, Ioc, FrontendMarket, LiquidationMarket, or empty for resting trigger orders), builder (third-party identifier when the order was routed through a frontend), status (open, filled, cancelled, triggered), oid, side, size, and price. Hyperliquid's L1 info API supplies userNonFundingLedgerUpdates per wallet, which is the deposit / internalTransfer / send / spotTransfer / subAccountTransfer ledger that reveals each wallet's HL-internal funding and movement. Arkham Intelligence supplied entity attribution, populatedTags, and capital-origin transfers on Arbitrum and other EVM chains. HyperTracker supplied HL-native segment, equity, and lifetime aggregates for wallets with no EVM footprint.

The analysis ran across a window of 21 days, from 10 March 2026 to 31 March 2026, across the four Trade.xyz markets.

Behavioural classification runs on a per-wallet profile aggregated across all four markets. Wallets active on multiple markets have their order counts summed and their TIF and builder percentages recomputed once before any rule fires. The classifier never operates on a per-market basis.

The waterfall is "first match wins". Market Maker requires pct_alo ≥ 80% and total_orders ≥ 1,000. Both gates are aggregate, so a desk quoting two-sided spreads with thousands of ALO entries qualifies but a wallet that posted five ALO orders does not.

SAT requires pct_ioc ≥ 90%, pct_frontend_market == 0, pct_builder_orders == 0, and total_orders ≥ 10. The IOC gate is dominant but the two presence-checks are strict: a single FrontendMarket order or a single builder-tagged order disqualifies the wallet, on the principle that any human-facing surface signal is enough to rule out a pure direct-API operation.

Retail requires pct_frontend_market > 0 OR has_paid_builder == True. Any single FrontendMarket tag or paid-builder routing is sufficient evidence that the wallet ever touched a human-facing surface.

Airdrop Farmer requires exactly 2 fills (one to open the trade and another to close), plus pct_ioc ≥ 90%, pct_frontend_market == 0, and pct_builder_orders == 0. Strict equality on the order and fill counts because a relaxed version leaks into Retail and Unclassified. Additionally, a number of wallets from known algorithmic builders were also classified under Airdrop Farmers.

Anything that did not classify under the above rules was deemed unclassified.

Identity attribution was run on a top-450 candidate pool of wallets that move the dollar-weighted picture. The pool was composed of three lists: the 400 highest-volume wallets from the Retail and Unclassified buckets, the 25 largest MMs and the 25 largest SATs.

Unclassified was restricted to wallets whose dominant TIF was GTC. That last restriction excludes Unclassified wallets dominated by algorithmic orders: ALO (partial quoters) or IOC (pure takers), since the candidate pool was built to surface directional limit-order and market order traders instead of market makers and arb bots. Together the 450 wallets carry 78% of total volume of the markets.

For each candidate wallet, the Arkham waterfall started at address_enriched to read entity, label, populatedTags, and clusterIds. For HL retail, arkhamEntity rarely fired. The doxx happens through populatedTags[] (Polymarket-handle entries) and arkhamLabel (ENS, Gnosis Safe). Capital origin was traced via /transfers?to={addr}&chains=arbitrum_one&sortDir=asc&limit=3. The chronologically earliest Arbitrum inbound returned by that call was deemed the CEX, bridge, or upstream EOA that funded the wallet.

HyperTracker filled the HL-native blind spot: wallets that bridged once to HL and now trade exclusively on the L1 have no EVM footprint Arkham could index, but HyperTracker indexes HL's L1 directly through its segment, equity, and lifetime aggregates. Combined Arkham and HyperTracker coverage on the candidate pool was 91%.

Conclusion

Recent discourse around Trade.xyz has centred on whether participation is real or whether the venue is dominated by sybils farming the expected TGE. The analysis points to a layered answer.

Like any pre-TGE DeFi market, Trade.xyz has a sybil layer, as exemplified by a single operator running tens of thousands of wallets through a baton-pass farm. However, the sybil layer inflated the wallet count and not the dollar throughput.

We found no evidence of a separate high-volume wash-trading operation built to fabricate dollar throughput. Most of what looks like farming in the data runs through retail market-making bots: wallets posting both sides of the book and adding top-of-book depth rather than consuming it.

A lot of volume that does exist, comes from identifiable sources. A meaningful share of the top retail wallets carry Polymarket handles, ENS records, or social-graph identifiers from largest crypto-liquid desks (Jump Crypto, Selini Capital, Wintermute, Abraxas Capital).

The inflated wallet count is predictable pre-TGE behaviour. It does not extend to the dollar volume, nor to the identifiable cohort routing it.