Deep Dive

Crypto Market Makers 101: What Founders Need To Know

TL;DR

Every new token needs professional market making. Adverse selection, unhedgeable inventory risk, and absent price history make organic liquidity economically irrational. But for the first time, founders have real choices in how they structure it. CEX market makers operate under loan-and-option or retainer models, each with distinct cost and transparency tradeoffs. On the DEX side, passive LP positions are permissionless but unmanaged, while active onchain market making keeps assets protocol-owned and automates execution without custodial handoff. The decision is no longer binary.

The Bid-Ask Spread

Before explaining how market makers operate, it helps to define the mechanism at the center of their business.

The bid-ask spread is the difference between the highest price a buyer is willing to pay (the bid) and the lowest price a seller is willing to accept (the ask). Every liquid market has one. The spread exists because buyers and sellers rarely agree on exactly the same price at the same time, and someone needs to bridge that gap.

For a token trading near $1.00, the bid might sit at $0.995 and the ask at $1.005. The spread in this case is $0.01, or about 1%. For highly liquid assets like BTC or ETH on major exchanges, spreads compress to 0.01-0.05%. For newly launched tokens with thin order books, they can widen to several percentage points.

For a trader, the spread is the cost of immediacy. A trader who wants to buy right now pays the ask. A trader who wants to sell right now hits the bid. The counterparty positioned between those two prices, earning the difference, is the market maker.

What Is a Crypto Market Maker?

A market maker is a firm or individual that continuously posts buy (bid) and sell (ask) quotes for an asset, enabling other market participants to trade without needing to find a direct counterparty. To do this, market makers typically hold an inventory of assets on both sides of the orderbook, allowing them to meet demand regardless of direction.

This continuous quoting absorbs short-term imbalances between supply and demand. Without it, participants face wider spreads, delayed execution, and outsized price swings on even modest orders. The liquidity and depth that market makers create directly shapes market stability, price discovery, and overall investor confidence.

Quoting Mechanics

Market makers do not post quotes once. They use automated algorithms to adjust bids and asks dynamically, responding to shifts in supply, demand, and broader market conditions. For a token trading at $1, a market maker might quote a bid at $0.995 and an ask at $1.005 and update those prices hundreds of times per hour. The goal: anyone wanting to buy or sell can do so immediately at a competitive price.

Depth Provision

Beyond posting quotes, effective market makers ensure meaningful liquidity at multiple price levels. It's not enough to have $5,000 of buy orders at $0.995 if a trader wants to sell $50,000 worth of tokens. MMs layer orders throughout the order book so that large trades can execute without causing dramatic price impact.

What Market Makers Cannot Do

Control price or volume. Market makers do not control price or volume. However, MMs holding significant loan inventory can influence short-term price dynamics through trade timing and sizing. Founders should structure agreements with explicit prohibitions on manipulative practices and require verifiable reporting on execution activity.

Create Demand. Market makers provide liquidity, not demand. If no one wants to purchase the token, a market maker cannot create buyers. They can concentrate depth at specific price levels to absorb sell pressure, and many firms offer this as a service, but they cannot generate sustained buying interest that does not exist.

Guarantee outcomes. Any market maker promising price targets or volume guarantees should be treated with skepticism. Those promises are either undeliverable or signal intent to engage in manipulative practices.

How Do Market Makers Earn Revenue?

The textbook answer is the bid-ask spread. A market maker quoting a bid at $1,999.80 and an ask at $2,000.20 captures $0.40 per round-trip trade. At 0.02% per trade, this looks thin. Over thousands of trades per day, those spreads compound into meaningful revenue.

But spread capture is only one revenue stream, and often not the largest.

Market makers operating under loan-and-option agreements (covered in the next section) may earn a meaningful amount of their revenue from inventory trading: buying and selling the loaned tokens in response to price movements, timing entries and exits to capture directional moves. Cross-venue arbitrage, where MMs exploit price differences between exchanges, is another major source.

The capturing the bid-ask spread aligns the market maker's incentive with providing tight, continuous liquidity for the issuer, while the inventory-trading model aligns the market maker's incentive with maximizing trading profit on loaned tokens, which may or may not produce the desired liquidity outcomes the issuer expects.

Staying Delta-Neutral

Market makers aim to remain delta-neutral: earning revenue regardless of whether the asset goes up or down.

Delta measures how much the value of a position changes in response to a $1 move in the underlying asset. A delta-neutral position has no first-order exposure to price direction. Market makers maintain this by hedging across derivatives (options, futures, perpetuals), perpetual futures, maker orders on other venues, and OTC sales.

Maintaining neutrality requires constant monitoring and rebalancing. While hedging protects against small price movements, large or sudden market shifts can still cause losses.

Founders should expect that market makers will sell their token at some point to manage risk. When MMs sell tokens, it is typically done to hedge inventory exposure and acquire quote-side assets for trading, not for predatory reasons. Understanding this model prevents misaligned expectations.

Why Does Every Token Need Professional Market Making?

Three problems make organic market making economically irrational for new tokens:

Adverse selection. Market makers quote prices while facing informed traders: insiders, VCs, and team members with superior information about the token. For small-cap and newly launched tokens, a disproportionate share of incoming orders comes from informed participants. Without pricing models calibrated to this risk, losses can accumulate quickly.

Unhedgeable inventory risk. For BTC and ETH, market makers hedge using derivatives. For new tokens with no derivatives, they carry full inventory risk through extreme volatility. Tokens can drop 90%+ in hours.

No price history. Volatility estimation requires historical data. For newly launched tokens, there is none, making accurate risk pricing nearly impossible.

Without professional market makers, order books stay thin, spreads widen to several percentage points rather than the 0.1-0.3% that enables functional trading, and price impact on even modest trades becomes outsized. The result is a downward spiral: a poor trading experience leads to lower volumes, declining prices, and loss of confidence.

The inverse is equally powerful. Deep liquidity signals asset health, attracts participation from both retail and institutional traders, and creates the conditions for sustainable price discovery.

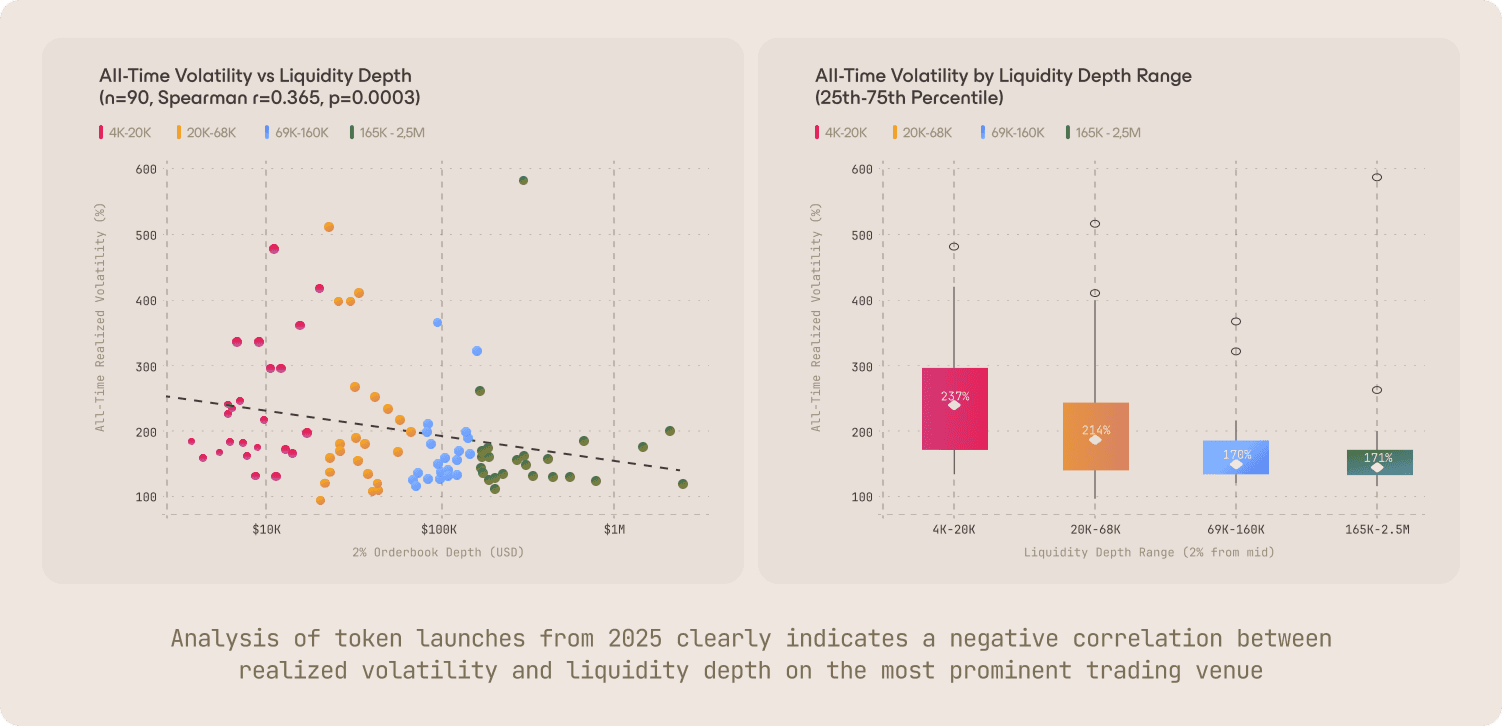

Our analysis of token launches from 2025 confirms a statistically significant relationship between order book depth and price stability. Tokens with less than $20K in 2% depth on their primary CEX venue experienced an average realized volatility of 237% annualized, compared to 171% for those with $165K or more. The relationship flattens above ~$70K in depth, suggesting diminishing returns beyond a baseline liquidity threshold.

How Do Projects Structure Market Making?

The market making landscape splits into two venues, CEX and DEX, each with distinct approaches.

CEX Market Making

Firms like Wintermute, GSR, DWF Labs, Cumberland, and B2C2 represent the dominant model today. Centralized exchanges are the primary venue because they offer high volumes, fast execution, CLOB architecture that allows precise spread control, and the infrastructure where price discovery happens for most assets.

CEX market makers typically engage projects through one of two deal structures:

Loan + Call Option (LOA). The project loans 1-5% of token supply for 12-24 months with call options at multiple strike price tranches. No upfront cash is required from the project, but the market maker holds and controls the inventory, and operations are largely opaque.

A structural consequence: the market maker receives only tokens, no stablecoins. To place buy orders, they often must sell a portion of the loaned tokens first, creating sell pressure during price discovery. Larger loans may produce more selling. A 3% token loan could generate meaningfully more sell pressure than a 1% loan.

Retainer. The project provides both tokens and stablecoins and pays a fixed fee, typically $3-7K per month per exchange. This model offers higher transparency and eliminates the sell pressure created by the LOA model, since the MM receives quote-side capital directly. It requires more upfront capital from the project.

Most projects have surplus tokens but limited cash, which explains why the LOA model remains common. Most MMs are also unwilling to accept pure retainers because they are less financially attractive than the option upside of an LOA.

In either case, the market maker manages custody, strategy, and execution largely offchain and at their discretion.

Practical considerations. Founders should consider using different models across different market makers: an LOA with one and a retainer with another. This diversifies exposure and balances tradeoffs. Do not combine models with the same market maker, as inventory dynamics conflict. Most projects engage two or three MMs across different venues to avoid single-provider dependency and ensure competitive quoting.

DEX Market Making

On the DEX side, two distinct approaches exist:

Passive LP positions. DEXs like Uniswap, Curve, and Balancer enable anyone to deposit assets into AMM pools and provide liquidity permissionlessly. Projects can either seed their own liquidity into passive positions or attract external LPs through token incentive programs.

In both cases, the liquidity is passive. There is no active rebalancing, inventory management, or fee optimization. As prices move, passive LPs lose value through impermanent loss. Capital spread across the entire price curve produces weak depth at the actual trading price. Incentive-funded liquidity also tends to be mercenary: it leaves when rewards dry up.

Active onchain market making. Projects deploy their own capital into smart contract vaults and retain full ownership. Active management is automated and executed onchain through algorithmic strategies. Onchain strategies can deploy concentrated liquidity requiring less quote-side capital upfront, since the vault can start with more project tokens and accumulate the quote asset as trades occur.

This model is non-custodial and transparent: all activity is verifiable onchain. It also supports the full token lifecycle, from TGE bootstrapping through mature liquidity management, without requiring renegotiation at each stage. Arrakis Pro is one example of this approach.

Market Making Approaches Comparison

Dimension | Traditional MMs | Passive DEX Liquidity | Onchain MM (Protocol-Owned) |

Venue | Primarily CEXs; occasionally DEXs | DEXs | DEXs |

Custody | MM holds and controls token inventory | Project or LPs deposit directly into pool; inventory is self-custodied | Project retains custody; delegates active management |

Management | Active, offchain, opaque | Passive (no active rebalancing) | Active, onchain, automated |

Cost Model | Token loan + option or retainer fee | Impermanent loss | Impermanent loss + strategy execution costs |

Transparency | Low (offchain, self-reported) | High (onchain, permissionless) | High (onchain, verifiable) |

Liquidity Depth | Variable; dependent on MM incentive alignment | Low; liquidity dispersed across full price range | High; liquidity concentrated around active trading price |

Why Are Founders Rethinking Market Making?

Several forces are reshaping how founders approach market making.

Growing scrutiny of loan-and-option practices. High-profile discussions around aggressive token dumping, option exploitation, and opaque execution have put the LOA model under public scrutiny. Founders are increasingly aware that while leading firms operate with integrity, the structural incentives of custodial arrangements may carry potential risk.

DEX infrastructure is maturing. Faster block times, declining gas costs, concentrated liquidity designs, and innovations like Uniswap V4 Hooks and HIP-3 markets are narrowing the gap between CEX and DEX trading environments. These developments make onchain venues an increasingly viable option for token issuers.

Real optionality now exists. For the first time, founders have choices across custody, cost, and transparency when structuring their liquidity. The decision is no longer binary: CEX market maker or nothing. Projects can combine approaches across venues, retaining control of their onchain liquidity while engaging CEX MMs for centralized venues.

What Are the Key Lessons for Founders?

Market makers provide liquidity, not demand. If no one wants to buy the token, a market maker cannot fix that. Any promise otherwise is a red flag.

Every new token needs professional market making. Adverse selection, unhedgeable inventory risk, and absent price history make organic liquidity economically irrational.

Understand the trade-offs of each approach. The LOA model may result in inventory trading as a revenue source over spread capture. Retainers align incentives more directly with liquidity provision. Passive LP positions generate no active management. Onchain market making automates the operational function while keeping ownership with the project.

The decision is no longer binary. Projects can blend approaches across CEX and DEX venues, matching each to their resources, risk tolerance, and transparency requirements.

This is the first in a series on crypto market making. The next piece will cover how to evaluate market maker proposals and navigate deal structures: the practical frameworks founders need to negotiate informed terms.

For a deeper look at structuring liquidity for your token launch, read our Practical Guide to TGE, or schedule a call with the Arrakis Team if you’re ready to explore onchain market making.

Disclaimer

This article is provided for informational and educational purposes only. Nothing in it constitutes financial, legal, tax, investment, or professional advice. Market conditions, deal structures, and fee terms referenced here reflect information available at the time of publication and are subject to change. Readers should independently verify all figures and terms with relevant counterparties before making any decisions. Arrakis makes reasonable efforts to ensure accuracy but does not warrant that all information is complete or current.