Case Study

TL;DR

The prevalent Loan and Option Agreement market making model forces projects to give up custody, accept opaque execution, and finance their own liquidity through dilution. Obol rejected this model and deployed protocol-owned liquidity through Arrakis-managed vaults on Uniswap, funded by protocol revenue and fully controlled by the project.

Over a two-month period of broader market weakness, the vault maintained a balanced 50/50 inventory, finished approximately 1% above a hold baseline, and captured over 99% of OBOL's onchain trading volume.

Arrakis lets projects deploy and manage liquidity from wallets they control, turning treasury operations like market making into sovereign, onchain functions.

The Cost of Renting Your Liquidity

Market makers play an essential role in token markets. They ensure tokens stay liquid and that traders experience reasonable slippage across market conditions. For most token projects, working with a market maker is one of the first operational decisions they make.

The most common market making arrangement is the Loan and Option Agreement, where the project loans a percentage of its token supply to a market maker for a fixed contract period. The market maker uses this inventory to quote on exchanges, either deploying their own capital as the quote asset or selling a portion of these loaned tokens to acquire USDC or ETH. For many teams, this is convenient because it removes the need to commit stablecoins or ETH from your own treasury.

However, this model carries a key tradeoff. Your tokens leave your custody for the duration of the agreement. There is no onchain visibility into how they're being used, no real-time controls, and no mechanism to recall them if conditions change. The actual positioning, inventory management, and execution remain opaque. Many market makers sell a portion of the loaned tokens to acquire quote-side inventory, creating direct sell pressure on the asset you are paying them to support. Projects end up financing their liquidity through dilution of their own token supply.

These tradeoffs were once avoidable. Onchain liquidity infrastructure now lets projects deploy and manage liquidity from wallets they control, with complete visibility into how their inventory is being used.

Obol's Protocol Sovereignty Principle

A protocol is sovereign over its liquidity when it custodies the assets, can verify every position onchain, and can adjust or withdraw at any time. No loan agreements, no custody transfers, and complete visibility over how inventory gets deployed.

Obol, the team building Ethereum's next generation Distributed Validator Infrastructure, made this a core operating principle going into 2026, deploying liquidity permissionlessly onchain and building a healthier spot market without ceding custody or control.

From Thesis to Execution

Obol published a public commitment to Protocol Owned Liquidity and consolidated their exchange presence by halting trading on smaller venues to reduce fragmentation. ETH earned from protocol fees was used to acquire 1,706,309 OBOL on the open market over a 15-day execution window, a second treasury operation followed shortly after, acquiring an additional 300,000 OBOL. The acquired OBOL was paired with ETH and deployed into Arrakis-managed Uniswap vaults, increasing liquidity depth for OBOL onchain through infrastructure the project fully controls.

Inventory Management Through Volatility

One of the most common objections to providing your own liquidity is directional risk. If the token price drops, a static liquidity setup accumulates more of the declining asset and sells the stronger one. For a project’s treasury, this is the worst possible outcome: you end up overexposed to your own token on the way down and depleted on your reserve asset.

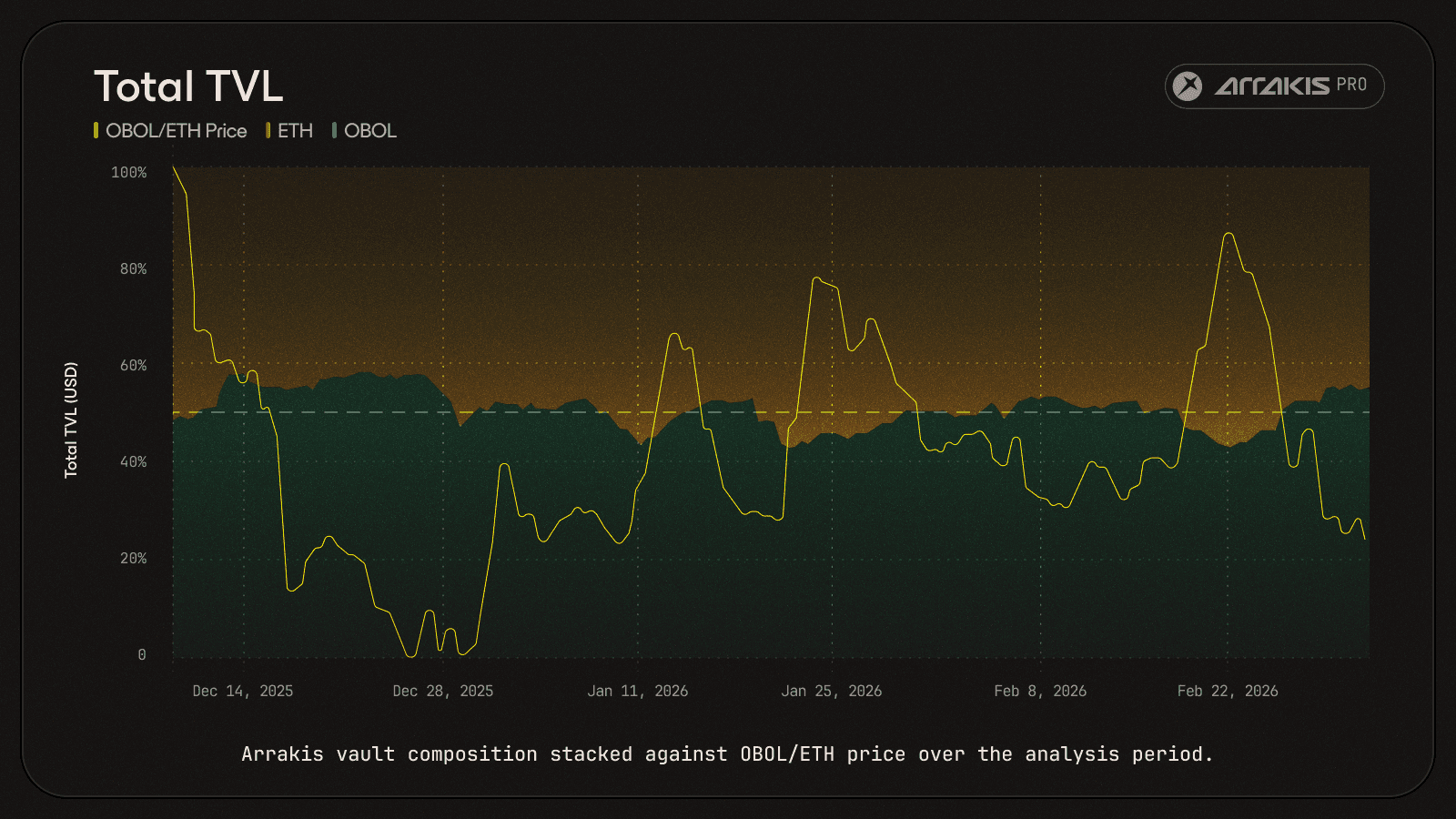

Arrakis vaults handle this differently. Over the period from December 2025 through early February 2026, OBOL experienced downward price action along with the broader market. A static concentrated liquidity position would have passively accumulated OBOL and sold ETH as the price declined, potentially losing all ETH inventory entirely.

The Arrakis-managed vault maintained a roughly 50/50 composition between ETH and OBOL throughout the entire period by actively repositioning its liquidity ranges. Even as OBOL's price declined, the vault avoided the single-sided exposure that a passive position would have suffered, instead rebalancing to acquire more ETH on the way down. The protocol actively improved its reserve position during a drawdown.

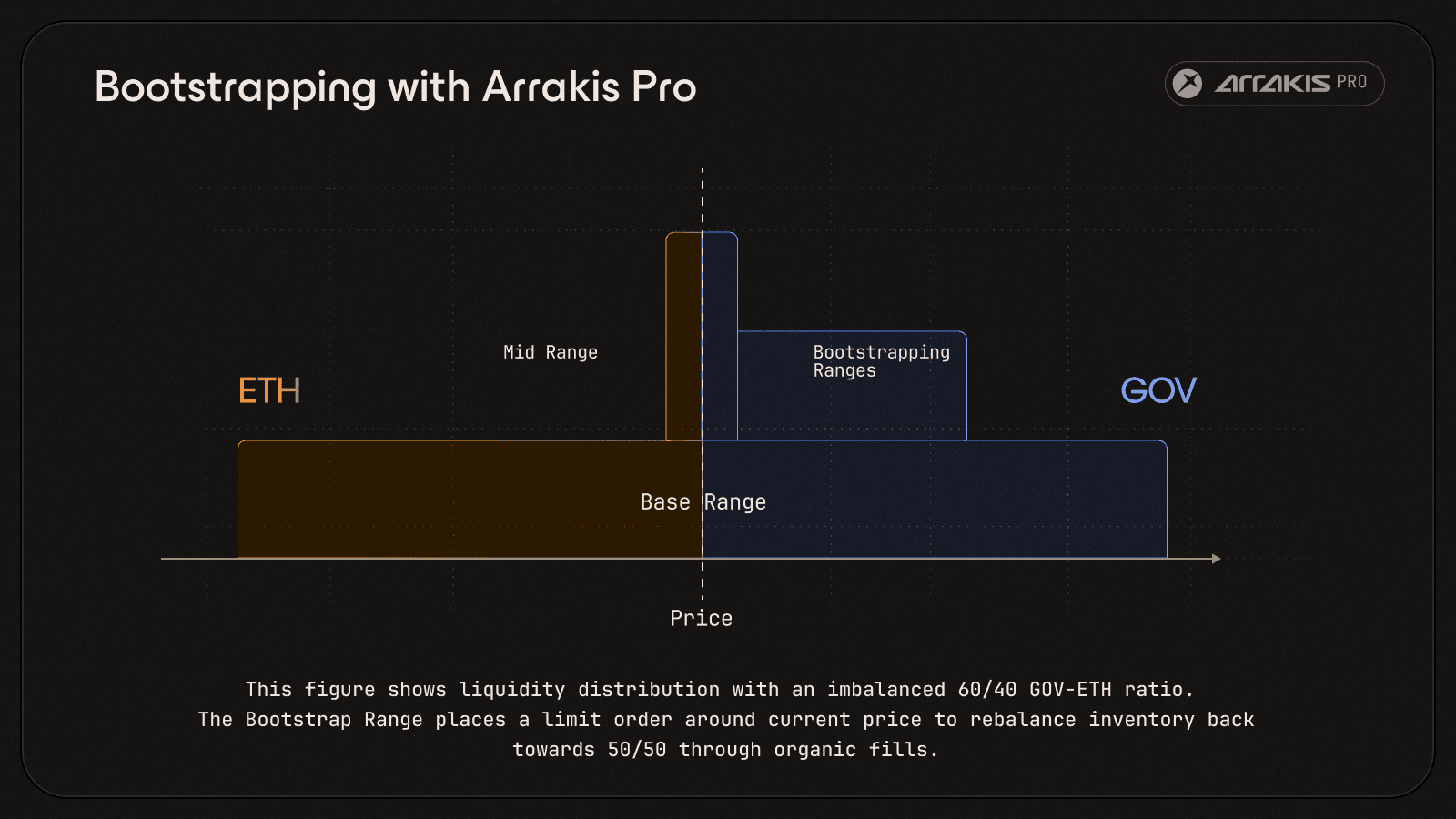

Here's how this works in practice: when inventory drifts beyond the target 50/50 ratio, the vault places a limit order around the current price to rebalance inventory. This is a passive position that executes only when a counterparty fills it through organic trading activity, not through aggressive market orders that could distort the price. Each fill rebalances inventory closer to the 50/50 ratio and earns the vault trading fee. The vault also adapts to market conditions dynamically, tightening ranges and deploying more capital in calm periods and widening ranges when volatility spikes. To learn more about how these strategies work under the hood, check out our deep dive on Arrakis Pro’s liquidity management strategies.

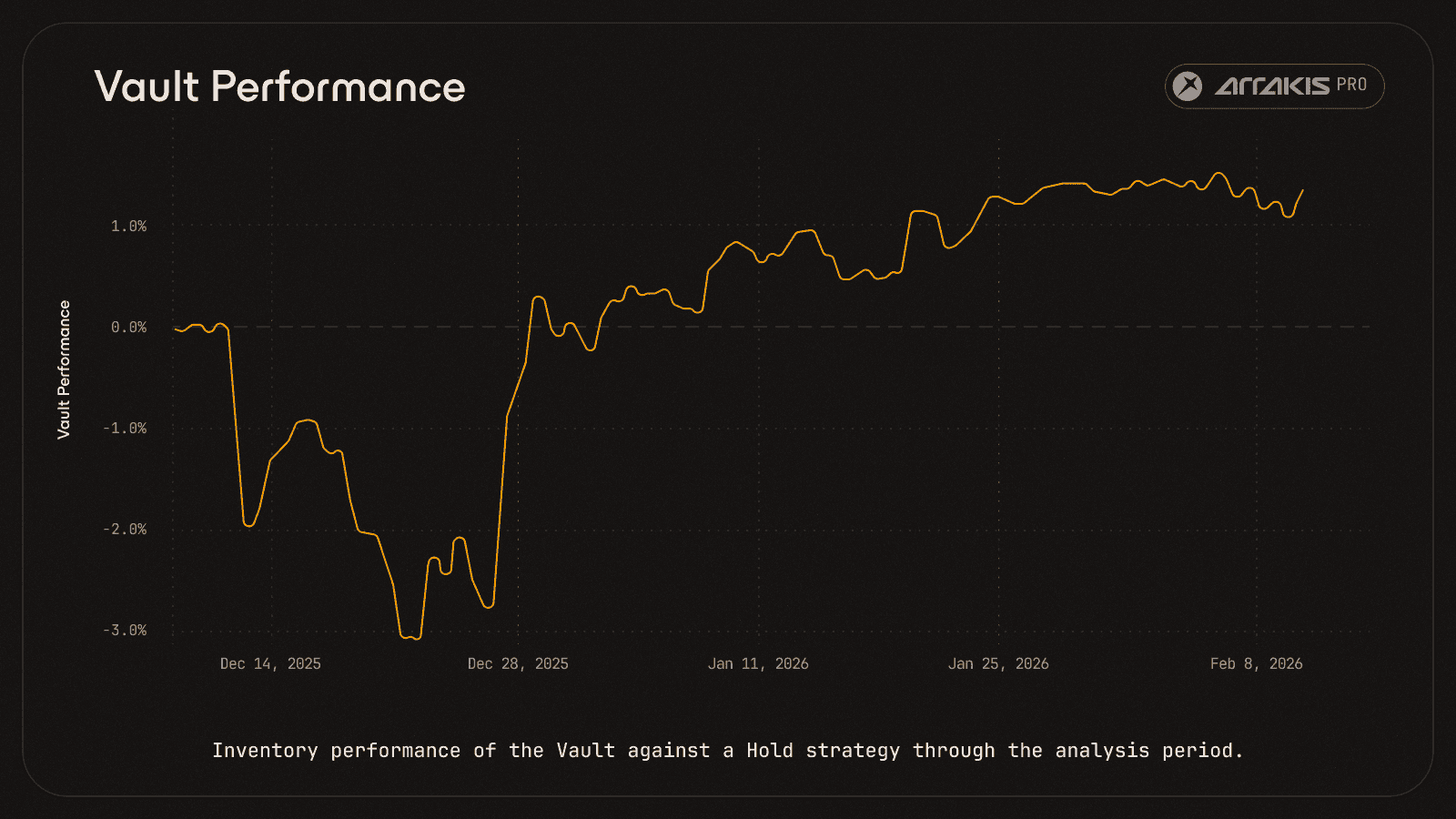

Performance vs. Hold

The result of this inventory management is visible in the vault's performance relative to a passive hold baseline. After an initial adjustment period in mid-December, the vault moved into positive territory and stayed there, finishing roughly 1% above hold by early February. The vault outperformed passive holding by rebalancing surplus OBOL in its inventory to bootstrap ETH.

For a project treasury, this is a relevant benchmark. A passive holder would have absorbed the full drawdown, whereas the actively managed vault converted volatility into a net positive outcome by rebalancing surplus OBOL into ETH throughout the decline. Protocol-owned liquidity, when actively managed, doesn't just provide depth to the market but can also strengthen the treasury's reserve position through volatile conditions.

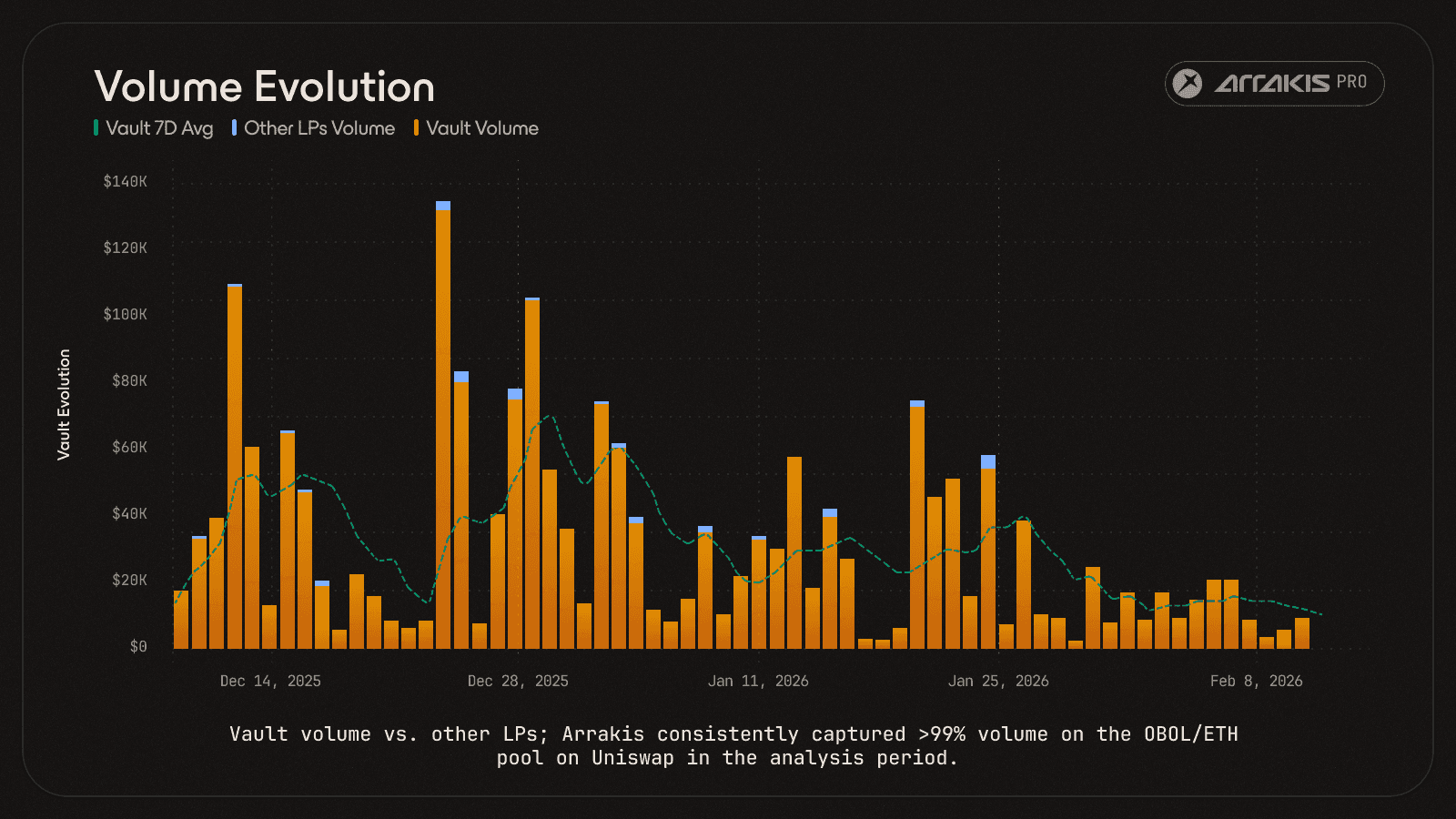

Volume Capture

The vault captured over 99% of trading volume on the OBOL/ETH liquidity pool throughout the period. On most days, other liquidity providers contributed only a small fraction of the total volume, with the Arrakis-managed vault handling the bulk of onchain execution.

Protocol-owned liquidity, when actively managed, can serve as the primary source of onchain depth. The project doesn't need to rely on external LPs to fill the gap.

Owning Your Liquidity Layer

Obol's shift to protocol-owned liquidity demonstrated a concrete pattern. A project can deploy its own spot liquidity, manage it through volatile conditions, capture the majority of trading volume, and retain full custody throughout.

Ethereum was built on the premise that protocols should be permissionless, verifiable, and self-sovereign. That premise should extend to how tokens are traded and how liquidity is managed. Obol’s results show what this looks like in practice: treasury operations running as sovereign, onchain functions rather than outsourced to opaque counterparties.

If you are a token project rethinking your liquidity operations, reach out here.