Research

Hyperliquid

And the Opportunity HIP-3 Missed

We've been covering HIP-3 oil markets across our previous pieces, documenting how tokenised perpetual futures on Hyperliquid became the only live oil price discovery venue during weekend CME closures, how four independent deployers (Trade.xyz, Kinetiq, Felix, Dreamcash) built competing oil markets, and why 24/7 permissionless oil trading matters in a geopolitical crisis.

HIP-3 oil perps rolled their contracts earlier this month, moving away from the most volatile, and perhaps the most consequential oil futures expiry in years. The May WTI contract expires on April 22nd. ICE Brent June (BZM6) expires April 30th. Both are in backwardation, with futures trading below physical spot. The convergence mechanics that pull futures toward physical at expiry are set to take effect, and HIP-3 traders won't be on the front-month contract when they do.

Banks and institutional desks roll early because they take long-term macro views and want to avoid expiry volatility. In crypto however, volatility is the product. Traders on Hyperliquid would want to be on the front-month contract precisely because it represents the most immediate settlement of oil prices. The early roll took this option off the table. Later in this piece, we outline specific product designs, including a front-month perp and a Dated Brent market that would capture exactly these dynamics.

1. What's Happening at the Strait of Hormuz

The Toll Booth

The Strait of Hormuz handles roughly 20% of global seaborne oil. Since mid-March 2026, Iran has blockaded the Strait of Hormuz, potentially charging $1 per barrel of crude for transit through a corridor around Larak Island in Iranian territorial waters.

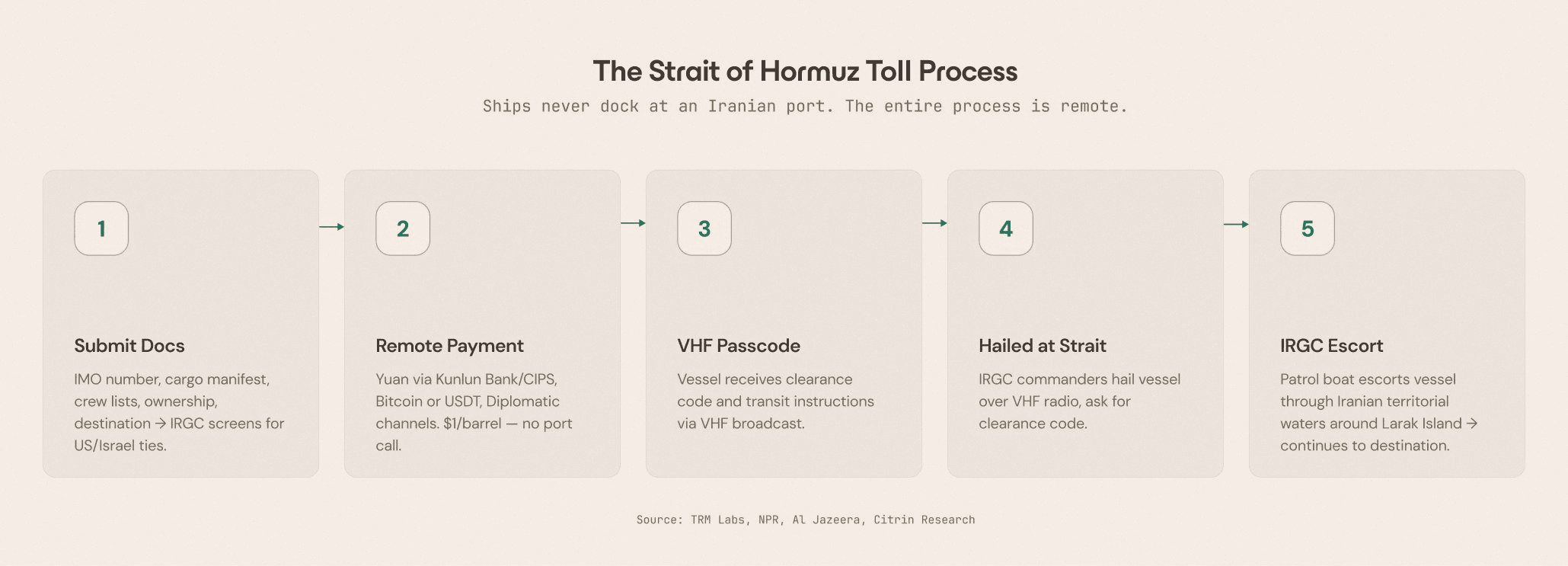

Here's how this works, step by step. Ships never transit at an Iranian port, documentation, payment, and clearance are all handled remotely.

Before transit: Ship operators contact IRGC-linked intermediaries and submit documentation: IMO number, cargo manifest, crew lists, ownership structure, destination. The IRGC screens each vessel for ties to the US or Israel.

Payment (remote): Settled before the ship reaches the strait, with no port call involved. Tankers can email cargo details to Iranian authorities, who levy a toll and instruct crews on how to settle in Chinese yuan routed through Kunlun Bank via CIPS (China's cross-border payment system).

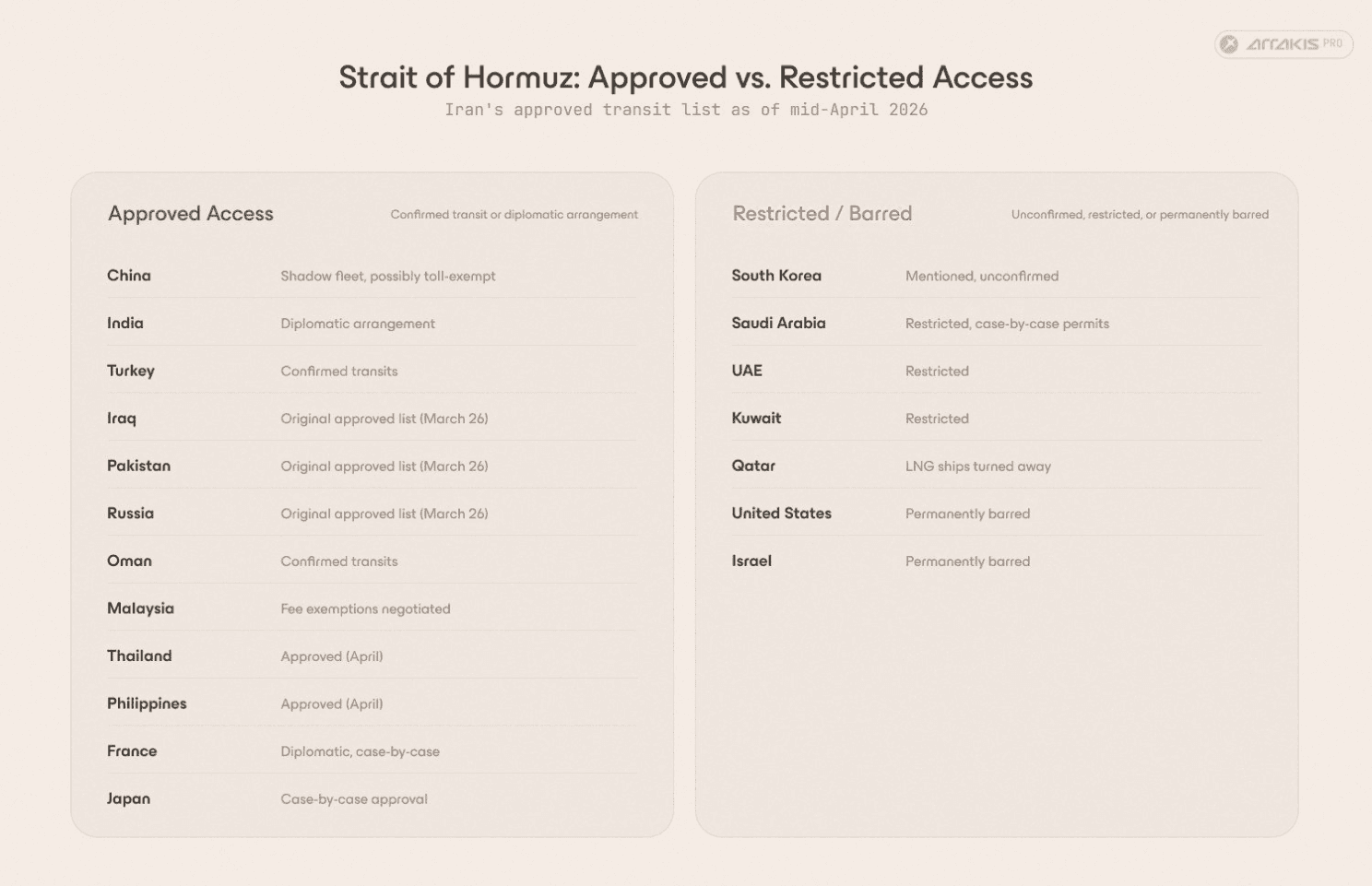

Bitcoin and possibly USDT are also accepted modes of payment. Diplomatic channels are a dominant mechanism for non-Chinese vessels, with some countries negotiating passage by unfreezing sanctioned Iranian assets so governments avoid paying Iran directly. India secured passage through a diplomatic arrangement, and France appears to have done the same. Chinese vessels may pass without paying at all.

Clearance: After payment, the vessel receives a VHF-broadcast passcode and transit instructions.

At the strait: IRGC commanders hail the vessel over VHF radio and ask for the clearance code. If approved, an IRGC patrol boat arrives and escorts the vessel through Iranian territorial waters around Larak Island.

The passageway runs through Iranian territorial waters but, critically, ships never dock at an Iranian port at any point in this process. They transit through territorial waters and continue to their destination, a distinction that is important in routing through the US blockade.

Citrini Research sent a field analyst to the strait in early April, operating from a speedboat 18 miles off the Iranian coast, where they engaged in manual vessel counts and conversations with captains and smugglers across Ras Al Khaimah and Musandam. Their 56-page report described the toll booth mechanics two weeks before the FT covered the $1/bbl payments: https://www.citriniresearch.com/p/strait-of-hormuz-a-citrini-field

The Strait of Hormuz toll process. Ships never dock at an Iranian port. The entire sequence, from documentation to IRGC escort through the Larak corridor, is conducted remotely.

Why Ships Use the Larak-Qeshm Pass

Pre-war, normal Traffic Separation Scheme (TSS) traffic flowed through much wider shipping lanes. Current routing is almost exclusively through the narrow Larak-Qeshm pass, a deliberate choice by ship masters.

Before the ceasefire, at least one Omani-flagged tanker was struck by Iran. The IRGC claims to have blockaded the traditional channels, and running them means no escort and no safety guarantee. The $1/barrel toll buys certainty: guaranteed safe passage with IRGC escort through a monitored channel is worth far more than $1/barrel to a ship carrying 2 million barrels. No IRGC-cleared vessel has been hit.

Insurance reinforces the choice. Marine war-risk insurers withdrew all Hormuz coverage. But Lloyd's of London syndicates are evaluating conditional war-risk policies specifically for toll-paying vessels, offering more attractive premiums for the IRGC-approved channel than the peacetime routes.

Official Iranian notice detailing approved transit corridors through the Strait of Hormuz, issued April 8 (Source: Iran's National Security Commission)

The US Blockade, and the Loophole

Trump's stated position (April 14): "Seek and interdict" every vessel in international waters that paid a toll to Iran. "No one who pays an illegal toll will have safe passage on the high seas."

CENTCOM's actual enforcement criteria: Ships "entering or departing Iranian ports," a scope considerably narrower than the administration's public stance.

The loophole: toll-paying ships transit through Iranian territorial waters but never call at an Iranian port. The entire toll process is remote. Ships paying the toll and sailing through the IRGC corridor without touching an Iranian port appear to fall outside CENTCOM's stated enforcement scope.

The roughly 6 vessels CENTCOM turned back were leaving actual Iranian ports: shadow fleet ships suspected of transporting sanctioned crude, AIS spoofers, and vessels that had called at Iranian ports. In the first 24 hours of the blockade, 20+ ships transited freely through the IRGC corridor, going to and from non-Iranian ports, even though many are believed to have paid Iran's toll.

While clear details are unavailable, enforcement appears concentrated in the Gulf of Oman rather than at the chokepoint itself. The Rich Starry tested the blockade and was turned back, but outside the strait. CENTCOM reports not a single shadow fleet vessel has transited since the blockade. That's their stated success metric: shadow fleet interdiction, not toll-payer interdiction.

Whether the gap between the administration's stated objectives and CENTCOM's operational criteria persists, narrows, or closes is among the most consequential variables in this market. If CENTCOM's criteria expand to target all toll-payers, that represents a major escalation. If the current framework persists, it remains quietly permissive for oil flow.

Chinese and Indian vessels continue transiting. Diplomatic arrangements provide dual cover: Iranian approval and sovereign shield from US enforcement, as documented by TRM Labs.

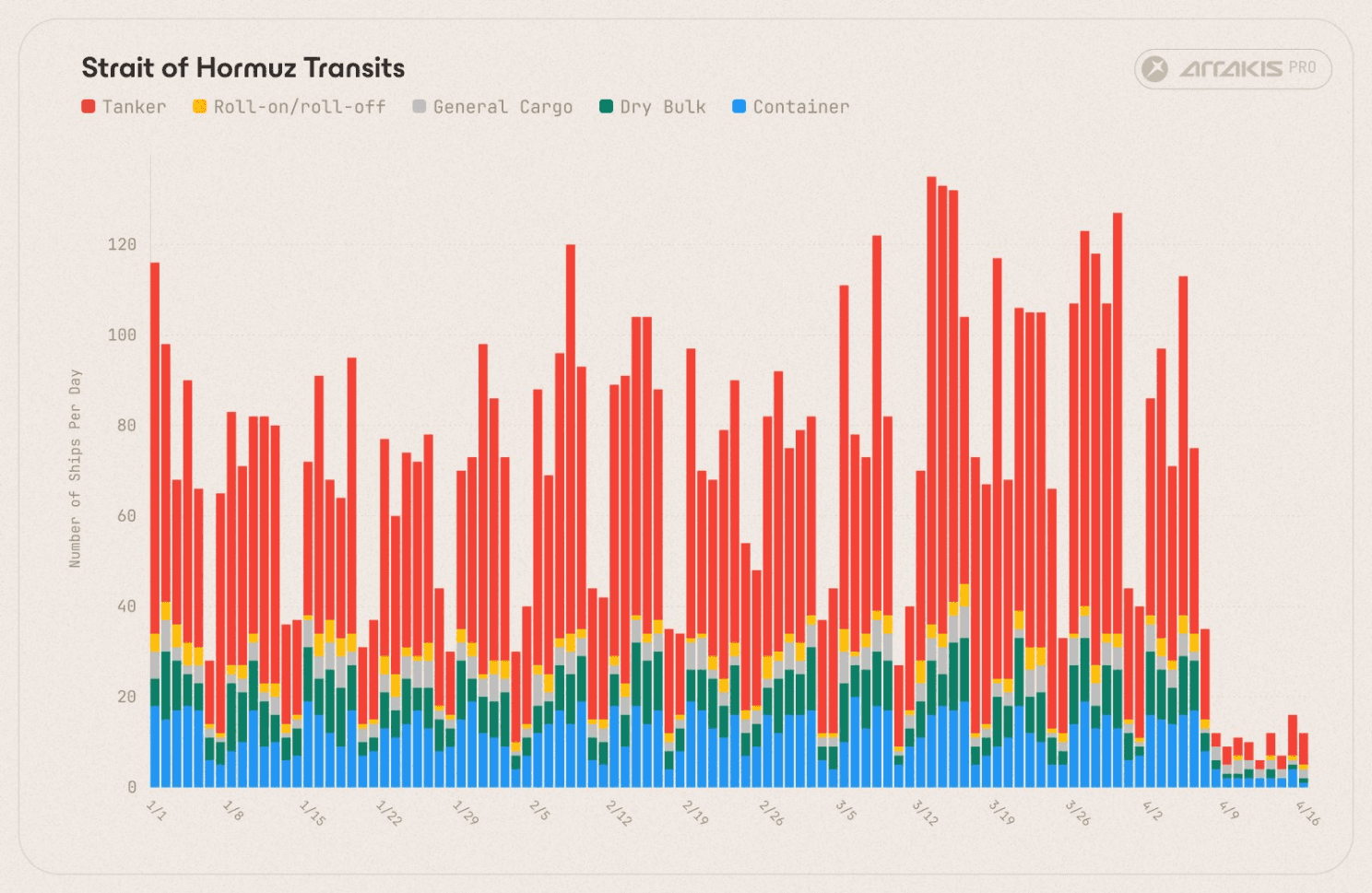

Daily strait transit volume with key event annotations. AIS-based counts may understate actual traffic by roughly 50% (per Citrini's manual vessel counts). Source: House of Saud

Timeline

April 8: Ceasefire agreed (Islamabad talks). Iran required to reopen. Formalised the toll booth instead.

April 22 (Tue): May WTI futures last trading day. Settles via physical delivery at Cushing, Oklahoma. Weekend events before this date will likely determine the direction of convergence.

April 22: Ceasefire expires.

April 30: BZM6 (ICE Brent June futures) last trading day. Cash-settles against ICE Brent Index.

2. The Price of Oil Is Not What You Think It Is

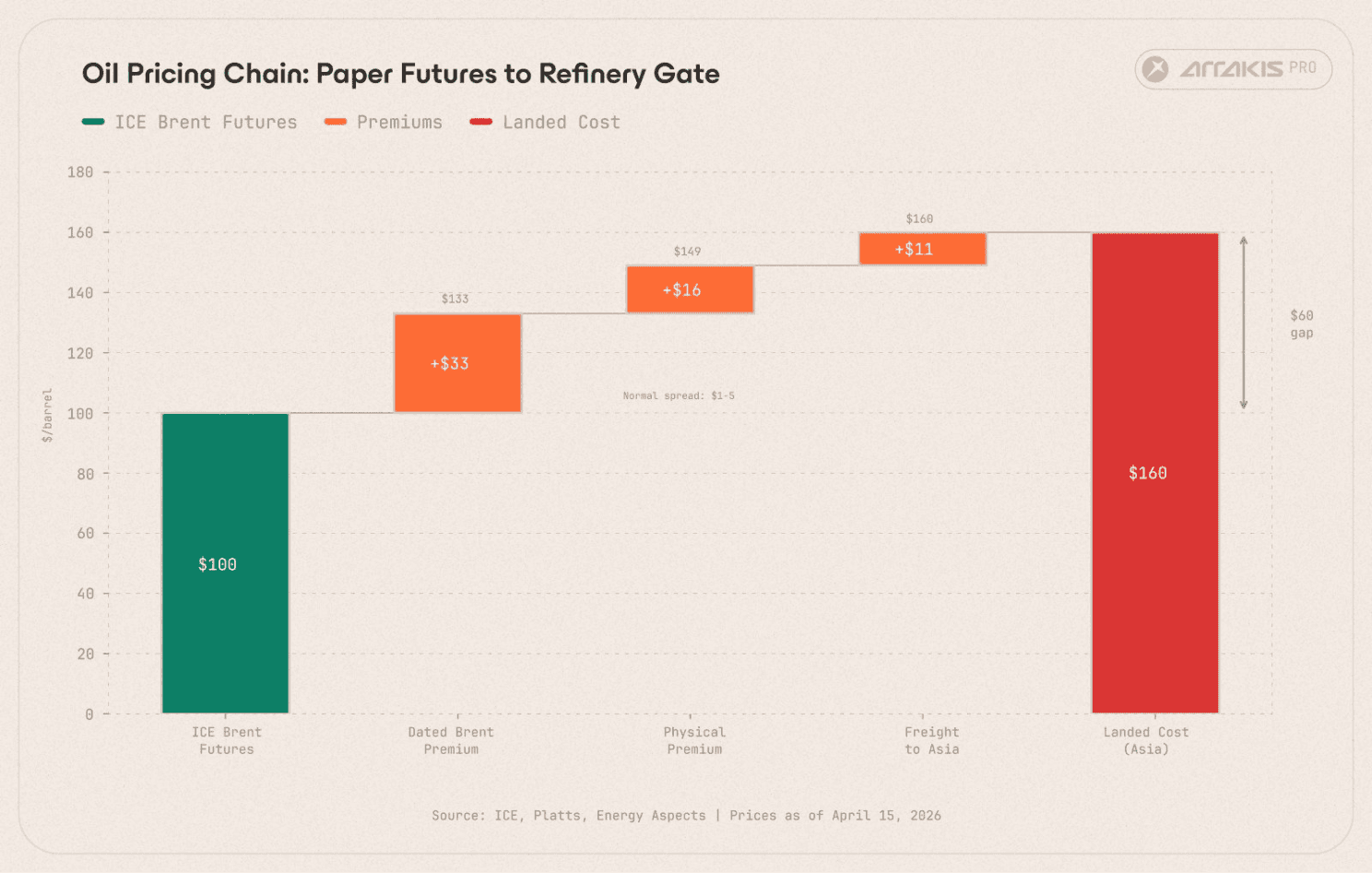

The Pricing Chain

The $90-100/bbl figure on a trading terminal or HIP-3 is a paper futures price. At contract expiry, futures converge to their physical settlement benchmarks: WTI to Cushing spot and Brent to the ICE Brent Index, which tracks Dated Brent.

Layer | What It Is | Price |

|---|---|---|

ICE Brent June futures (BZM6) | Paper contract. Expires April 30. Cash-settled. What HIP-3 Brent oracles reference. | ~$100-102 |

WTI May futures (CLK6) | Paper contract. Expires ~April 22. Physical delivery at Cushing, OK. What HIP-3 WTI oracles reference. | ~$95-98 |

WTI Cushing spot (physical) | Physical oil at Cushing, Oklahoma. What WTI futures converge to at expiry. | ~$100.72 |

Dated Brent (Platts assessed) | Global physical benchmark. Assessed from real cargo trades, 10-30 day loading window. 75% of global traded crude prices off this number. | ~$133 |

Outright cargo (North Sea Forties) | Dated + physical premium ($15-20). What a European refinery buys. Exceeded the 2008 peak on April 14. | ~$149 |

Landed cost (Asia) | Outright + freight. What an Asian refinery pays at the gate. | ~$160 |

Illustrative figures of oil and crude related futures contracts across all layers of the crude oil market.

The full supply chain spread, from paper futures to refinery gate, is $60/bbl, which is pushing towards some of the most extreme spreads in paper to spot oil markets have seen since 2008.

Oil pricing chain from paper futures to Asian refinery gate. The $60 spread reflects full supply chain costs; the convergence gap that futures settle against is ~$33 for Brent and ~$3-5 for WTI. Source: ICE, Platts, Energy Aspects. Prices as of April 15, 2026.

When you trade oil on HIP-3 markets, you're trading the paper futures price at the top of this chain.

What Is Dated Brent and Why Should You Care

Dated Brent is a basket of crudes (BFOETM: Brent, Forties, Oseberg, Ekofisk, Troll, plus WTI Midland) assessed daily by S&P Global Energy from real cargo trades with loading dates 10-30 days ahead. It's the benchmark 75% of global traded crude prices against, with over $1 trillion per year in contracts linked to this single assessment.

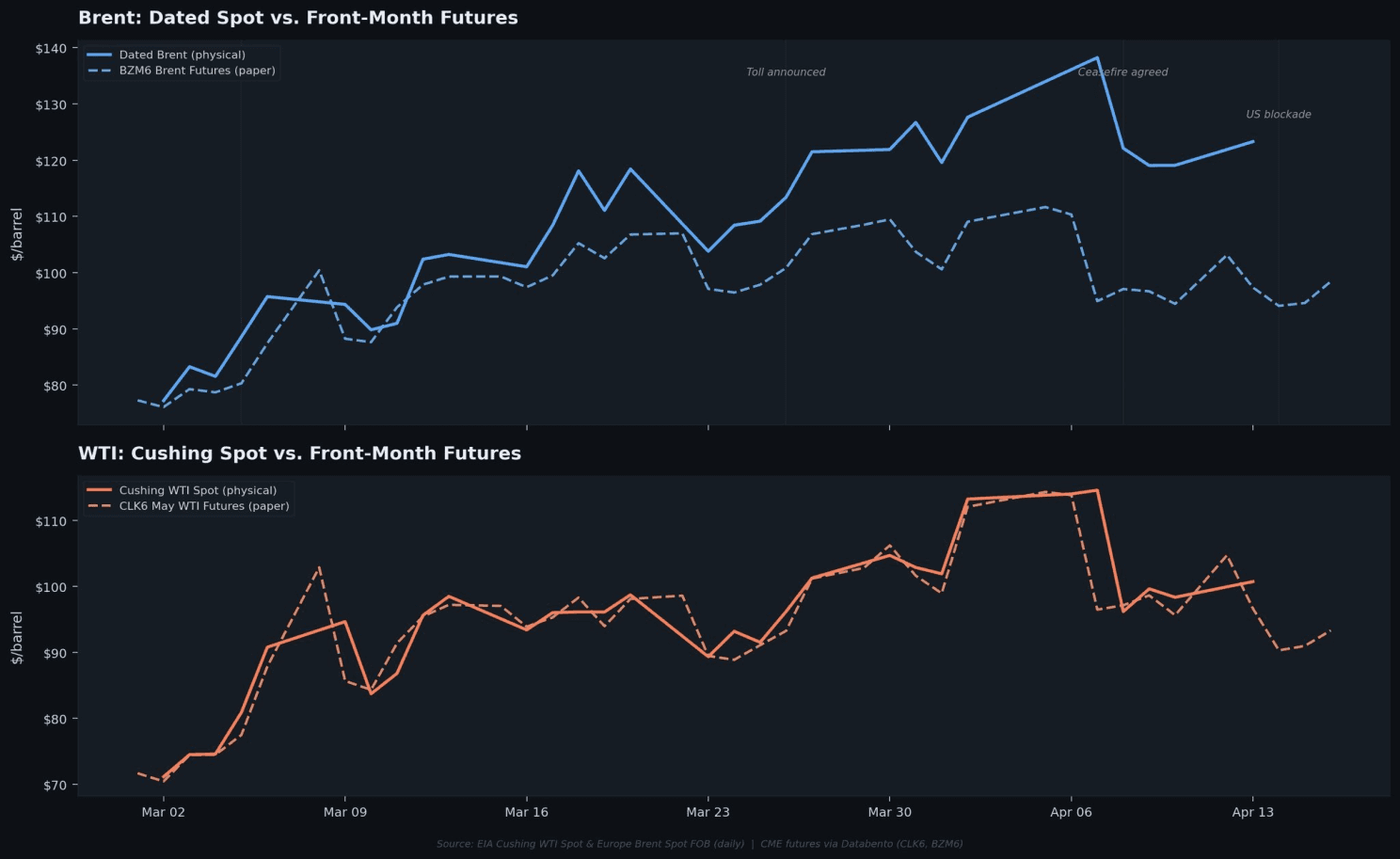

Dated Brent and Cushing WTI spot prices (solid) vs. their front-month futures contracts (dashed) since March 2026. Brent physical pulled sharply above futures as the Hormuz crisis deepened; WTI spot and futures track more closely, reflecting insulation provided by US domestic supply. Source: EIA.gov spot price timeseries, CME futures via Databento

Backwardation: Why the Spread Exists

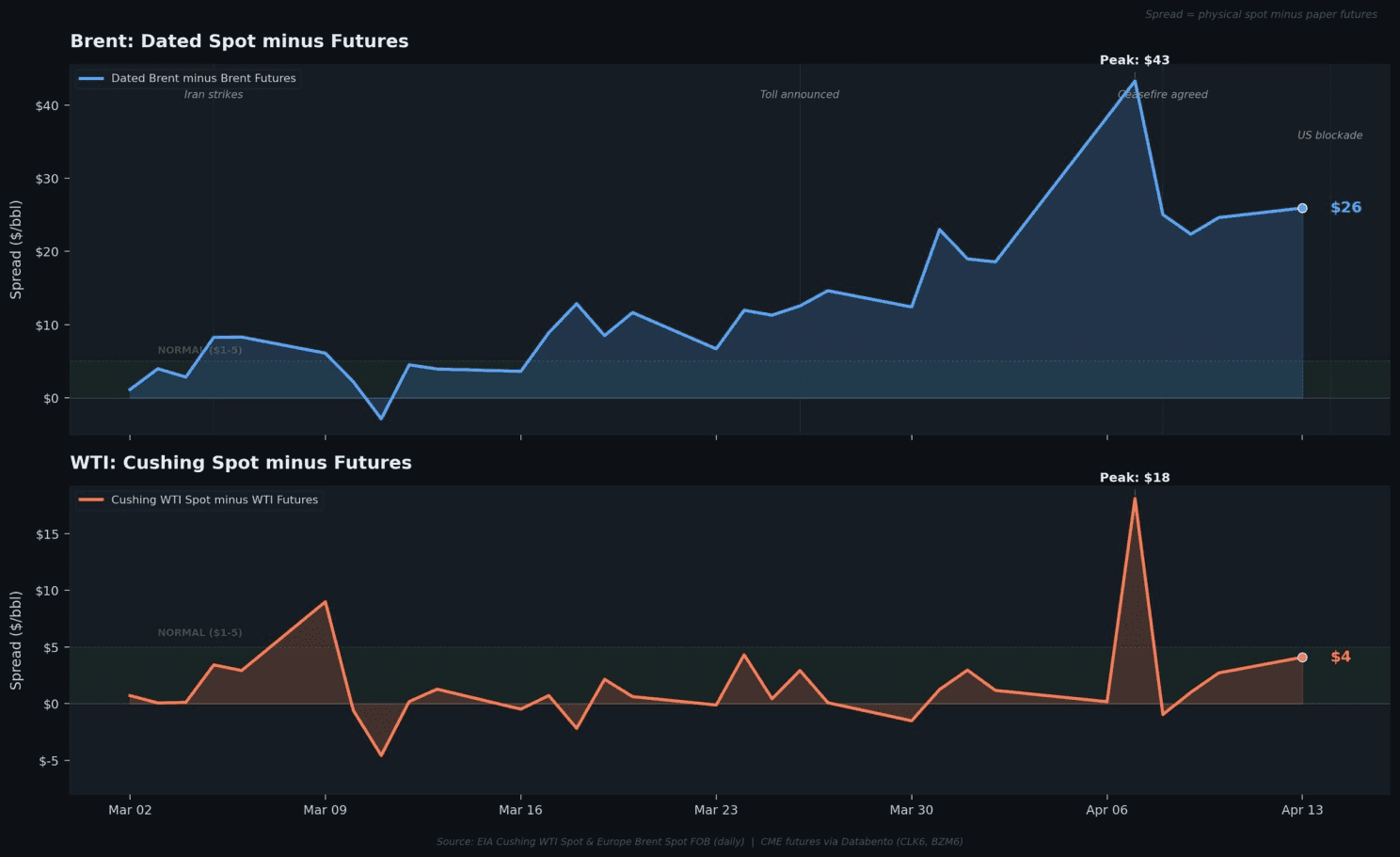

Backwardation means near-term physical prices are far above longer-dated futures. The current backwardation is among the most extreme in the recent decades.

Here's how the mechanics work.

Physical/spot reflects scarcity right now. Refiners need barrels today. A refinery shutdown costs roughly $5 million per day. They pay whatever it takes. European refining margins have turned negative at -$6.45/bbl (week of April 6), meaning refiners are paying more for crude than they earn from products, and they're still buying.

Futures reflect expectations for tomorrow. Markets expect some resolution. Longer-dated contracts carry less panic premium.

The spread is the curve pricing the time dimension. Crude barrels are scarce today. Contracts with expiries in the future assume some normalisation.

Both WTI and Brent are in backwardation. However, WTI's backwardation is smaller because US domestic supply (Permian Basin to Cushing pipeline network) cushions against Hormuz disruption. But also, WTI's convergence mechanism is more direct: it settles via physical delivery, not a cash index. More on this in Section 4.

The convergence gap: physical spot minus paper futures for Brent (top) and WTI (bottom) since March 2026. The Brent spread blew out from a normal $1-5 to a peak of $43, while WTI's gap stayed smaller due to Cushing's Permian pipeline cushion. Source: EIA.gov spot price timeseries, CME futures via Databento

3. Why the Gap Can't Be Arbitraged Away

If you've spent time in crypto, a $60 gap between two expressions of the same asset sounds like free money. Somebody should arb it. Here's why they can't.

The One-Sided No-Arbitrage Bound

In contango (futures above spot), arbitrage is mechanical. Buy spot oil, store it, sell forward. The spread can't exceed carry costs (storage + financing + insurance) because anyone with capital and a storage tank can enforce the ceiling.

In backwardation (spot above futures), there is no equivalent mechanism. Closing the gap requires "shorting physical oil": selling barrels you don't own. No mechanism exists for this at scale:

There is no centralised oil custodian (no DTCC equivalent for crude)

There is no organised oil lending market

Oil is a consumption commodity. Once refined, it ceases to exist.

Extreme backwardation can persist for long durations with no natural arbitrage force to compress it.

Three Forces Widening the Spread

The spread is being actively widened from both sides.

Force 1: Physical scarcity. The root cause. Hormuz at under 15 ships per day versus 60+ pre-conflict. If transit is still at this rate by end of April, the net hit to global commercial oil stocks is estimated at 10.6 million barrels per day.

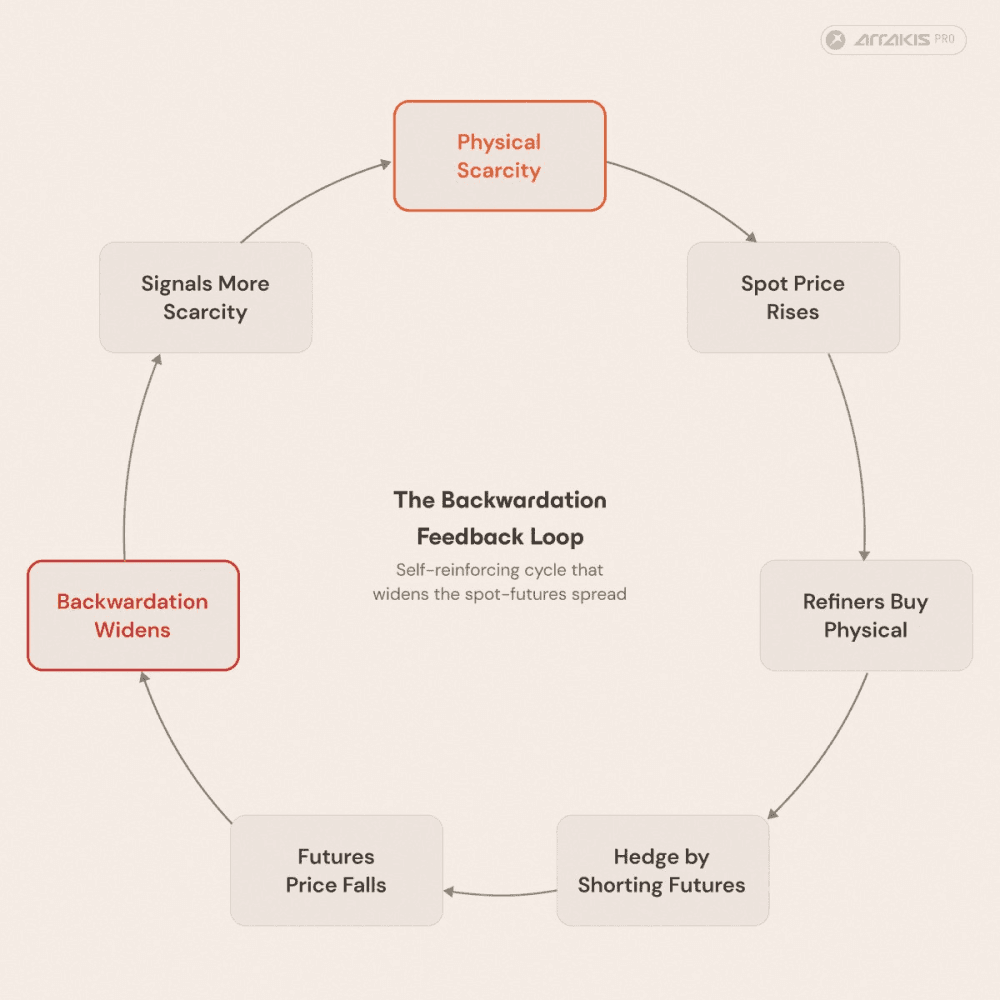

Force 2: The consumer hedge amplifier. Refiners buy physical crude at $149 because they must. A shutdown costs $5M per day. The buying is inelastic. Having bought expensive physical, they hedge by shorting futures. Every hedged barrel is a sell order in futures with no corresponding buy order, pushing futures down and widening backwardation. A wider backwardation signals more scarcity to the next buyer, triggering another round of panic buying and hedging that widens the spread further. The market amplifies its own scarcity signal through the feedback loop between physical procurement and financial hedging.

The backwardation feedback loop. Refiners' inelastic physical buying and subsequent futures hedging creates a self-reinforcing cycle that widens the spot-futures spread from both sides. Source: Oxford Energy Institute

Force 3: The destocking spiral. In backwardation, holding inventory loses money versus selling now. Holders sell immediately, which draws down inventories, reduces supply, pushes spot higher, and incentivises more selling. Prior to the week of April 13th, global average VLCC indices hit the highest levels since at least 2008, making floating storage prohibitively expensive and accelerating the drawdown.

Result: spot is pushed up by panic buying and destocking. Futures are pushed down by hedging flow.

The China Card

China acquires crude at a significant discount to open-market prices, primarily through purchasing Iranian oil via a shadow fleet that Citrini Research documented during its field reporting. Chinese vessels were observed in the Larak-Qeshm pass on April 2nd, and sources indicated they may transit without paying the toll at all.

The result is a significant cost basis advantage over European refiners paying the $149 North Sea premium, derived from access to sanctioned Iranian crude.

If the US succeeds in blockading all ships going through Iranian ports, China may be forced to bid up crude in the North Sea, which would increase both BFOETM and Indian Basket prices and push Asian and European crude costs higher still.

4. The Convergence: How Paper Meets Physical

Futures are currently trading below physical crude. At expiry, they must converge. Here's how this would work for both WTI and Brent, and why the mechanism differs.

WTI May (CLK6), expires April 22 (Tuesday)

WTI settles via physical delivery at Cushing, Oklahoma. If you're short WTI at expiry and don't close, you must deliver physical barrels to Cushing. If you're long, you must accept delivery.

The futures price must converge to the Cushing spot price because at expiry they become the same thing: actual oil at a specific location. WTI doesn't settle against a forward cargo assessment like Brent. It settles against the physical barrels of crude at Cushing at the time of expiry.

The WTI backwardation is smaller than Brent's because Cushing is supplied by the Permian Basin pipeline network, not tankers through Hormuz. US domestic supply cushions the spot price, but the convergence is more mechanical and more immediate. What happens over the weekend of April 18th, ahead of Tuesday's expiry, will likely determine the direction of that convergence.

ICE Brent June (BZM6), expires April 30

Brent settles via cash settlement against the ICE Brent Index, derived from physical BFOETM trading activity during the final trading days. The Index is a physical-derived number, but it can settle at a discount to the North Sea cash spot market because the Index calculation methodology averages over a window and may not capture the full spot premium. If Dated Brent is at $133, the Index will be directionally closer to that price, but the relationship isn't as tight as WTI's physical delivery mechanism.

Additionally, Brent backwardation is larger because it reflects the global physical market (Hormuz-exposed), not just US domestic supply.

WTI May (CLK6) | ICE Brent June (BZM6) | |

|---|---|---|

Expiry | ~April 22 (Tue) | April 30 |

Settlement | Physical delivery, Cushing OK | Cash, ICE Brent Index |

Convergence to spot | Direct. Futures = Cushing spot at expiry. | Indirect. Index derived from BFOE activity. |

Backwardation | ~$3-5 (Cushing cushioned by Permian) | ~$31-33 (global physical market) |

Can settle at discount to spot? | No. Physical delivery IS spot. | Yes. Index methodology may not capture full spot premium. |

HIP-3 relevance | Already rolled past this contract | Already rolled past this contract |

Spot vs. futures convergence paths for Brent and WTI. At expiry, WTI converges directly to Cushing spot via physical delivery; Brent converges to the ICE Brent Index derived from physical BFOE trading.

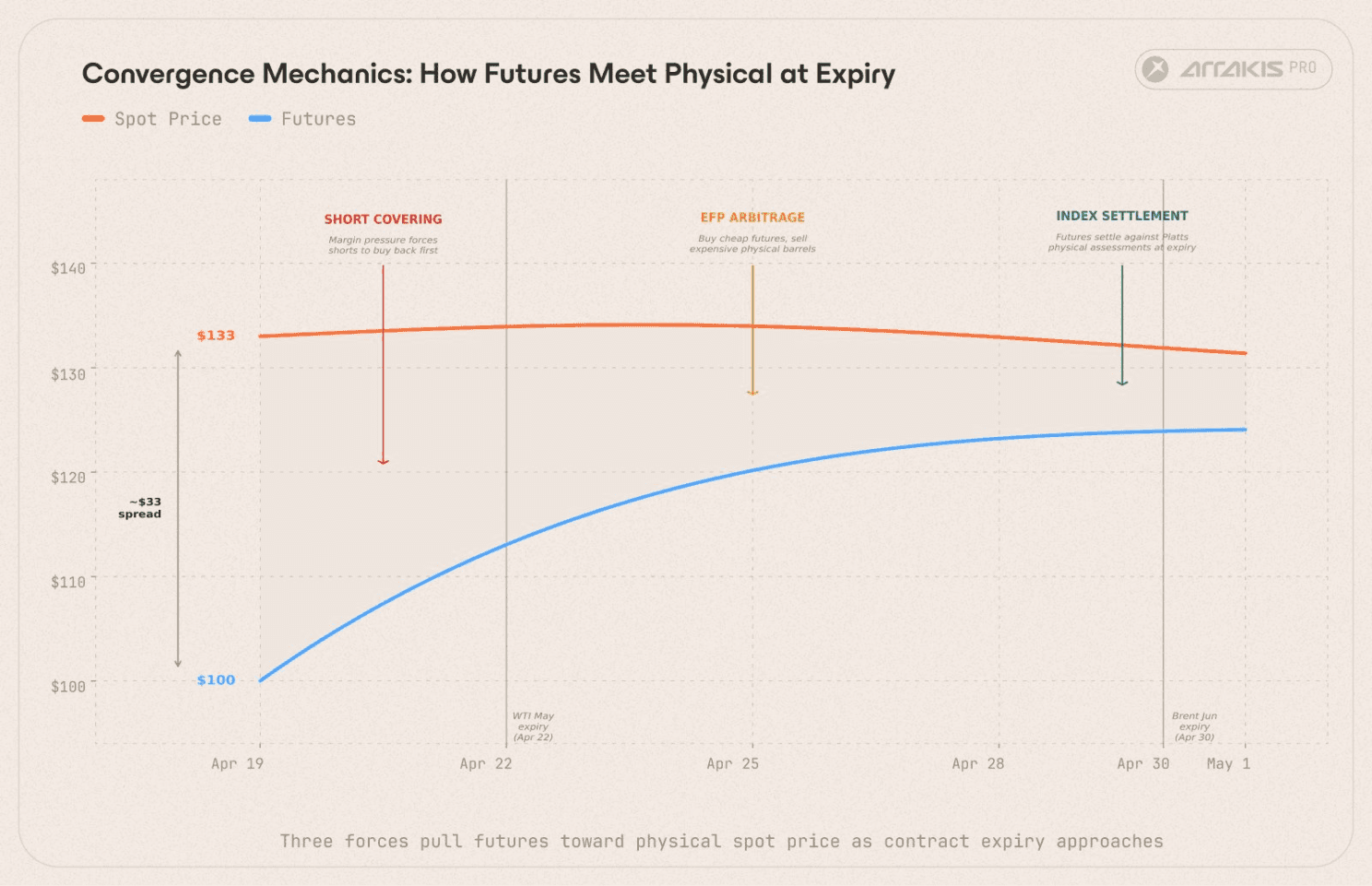

Three Forces Pull Brent Futures Up

Force 1: Index settlement. The destination is set by physical. If Dated Brent remains at $133+, the ICE Brent Index on April 30 will tend closer to spot. Every open futures position settles there.

Force 2: EFP arbitrage. Traders buy cheap futures, sell expensive physical, and use EFP (Exchange of Futures for Physical) swaps to convert paper into physical. The long paper cancels the short physical. Locked-in profit minus EFP cost. Executing at scale requires aggressive futures buying, which pushes the price up and closes the gap.

Force 3: Margin-driven short covering. While futures shorts don't borrow anything (unlike equity shorts), and can in theory hold to cash settlement, margin mechanics create economic pressure to close early. Daily variation margin bleeds capital as the price moves against them. Exchanges have raised initial margin requirements during this crisis. Volatility-targeting models at institutional desks auto-reduce position size when realised volatility spikes. Institutional stop-losses trigger buybacks. Each wave of covering pushes the price higher, increasing margin pressure on the next cohort, which triggers more covering. It cascades.

The three mechanisms reinforce each other. Index settlement sets the destination. EFP arbitrage pulls futures toward it. Margin-driven covering accelerates the move.

Illustrative only. This diagram shows the three forces that typically pull futures toward physical spot at expiry. It's not a prediction of how convergence will play out. With event-driven volatility this extreme, convergence could possibly occur through spot falling toward futures (e.g. a ceasefire or deal that eases physical scarcity) rather than futures rising to current spot levels.

5. The Lost Opportunity: What HIP-3 Missed

How HIP-3 Oil Perps Work

HIP-3 perps don't expire. Their oracle references ICE Brent or WTI futures. When the actively referenced futures contract gets pulled up by convergence mechanics, the oracle reprices, and HIP-3 perps follow.

The issue: HIP-3 markets roll their underlying contract reference early in the month, moving from the front-month (nearest expiry) to the next month. This is standard practice in institutional finance. Banks and macro desks roll early because they take long-term directional views and don't want the volatility, liquidity fragmentation, and settlement risk around contract expiry.

By the time of writing, HIP-3 oil markets have already rolled past both the May WTI and June Brent front-month contracts.

Why This Matters

The front-month contract is where the convergence happens. It's where the spread between futures and physical gets mechanically closed through index settlement, EFP arbitrage, and margin-driven short covering. The front-month is where realised volatility spikes.

In traditional finance, avoiding this volatility is a feature. A pension fund rolling its oil exposure doesn't want to be caught in a short squeeze. A bank's macro book wants smooth exposure to oil's direction, not the noise around contract expiry.

In crypto, this volatility is the product. Hyperliquid traders trade volatility. The entire value proposition of 24/7 permissionless perps is that you can express a view when others can't: weekends, holidays, 3am on a Tuesday. Rolling away from the most volatile period of the most volatile oil contract in years is the opposite of what the market is designed for.

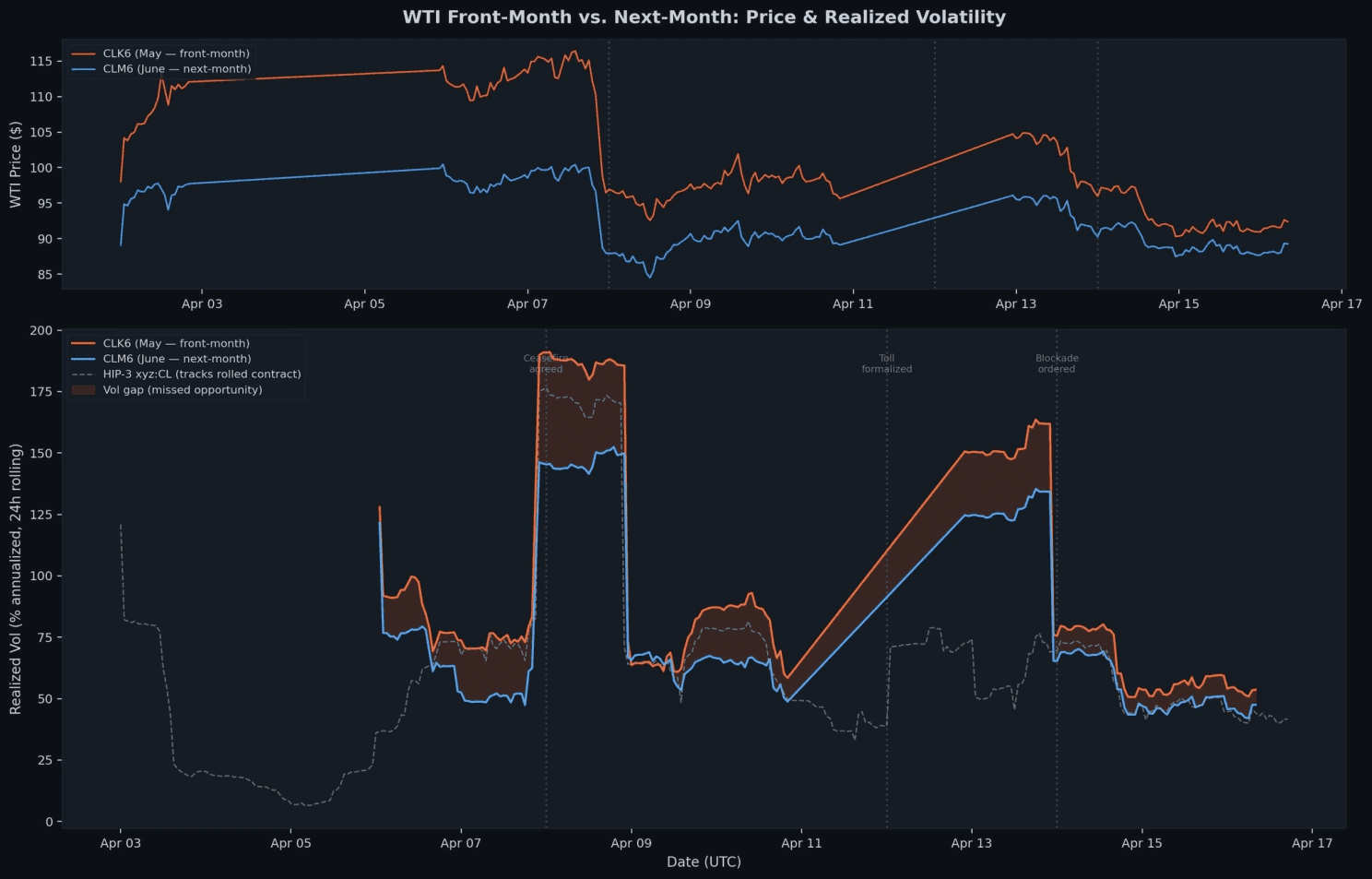

CHART: Realised volatility (annualised, from log returns) of HIP-3 oil markets vs. WTI front-month futures over the past 2 weeks. The volatility divergence, with front-month spiking as expiry approaches while HIP-3 on the rolled contract stays calmer, IS the missed opportunity. Source: HIP-3 candle data via 0xArchive + CME/ICE data

6. The Path Forward: What HIP-3 Could Become

The Immediate Improvement: A Front-Month Perp

The simplest solution would be a new oil perp that rolls its contract reference closer to expiry, with a softened rolling function to avoid discontinuities. Deployers like Felix or Dreamcash, who already operate softening roll logic, could implement this.

The design: the oracle references the front-month contract until closer to expiry (T-3 or T-5 days rather than the current early-month roll). A softening function during the roll window gradually blends the expiring contract with the next month over a defined period to avoid a price jump. Traders who want front-month volatility and convergence exposure trade this market. Traders who prefer the smoother, rolled-early exposure keep the existing markets.

The Bigger Opportunity: Markets That Don't Exist Offchain

HIP-3's real potential isn't replicating CME Group Energy and ICE products onchain. It's creating markets that don't exist in traditional finance at all.

Two candidates that would have been enormously valuable in this crisis:

A Dated Brent perp. Dated Brent is the $1 trillion per year benchmark that 75% of global traded crude prices against. But there is no liquid, tradeable futures contract for Dated Brent itself. Physical traders access it through the CFD market (Contracts for Difference between Forward Brent and Dated Brent), a small, specialist, OTC market with roughly 100 participants worldwide.

A Dated Brent perp on HIP-3 would let anyone express a view on the physical benchmark directly, not through the intermediary of ICE Brent futures. Right now, the Dated-to-futures spread is $30+. That spread is where the real story lives. Making it tradeable on Hyperliquid would be a first. An oracle referencing Platts daily Dated Brent assessments or a real-time physical assessment built from cargo trade data could underpin the market.

A Cushing WTI Spot perp (FOB). WTI futures settle against physical delivery at Cushing, Oklahoma. The Cushing WTI Spot Price is what the settlement converges to, but this spot price isn't directly tradeable as a standalone futures or perp product. You can only get exposure by holding WTI futures through expiry and accepting or delivering physical.

A Cushing spot perp would let traders trade the settlement value directly: the thing that WTI futures converge to, without dealing with physical delivery logistics. A real-time oracle for Cushing spot would need to be constructed, but the underlying data exists.

Both of these are markets traders cannot currently access directly in traditional finance. They trade around them through complex OTC instruments, physical cargo trades, or by holding futures through expiry. Putting them on Hyperliquid as perps would create genuinely new financial products.

Conclusion

The backwardation on oil futures today is among the most extreme since 2008, and how the convergence of major front-month contracts play out over the next two weeks is one of the most closely watched events in commodity trading right now.

HIP-3 markets have grown significantly this year by offering something traditional markets cannot: 24/7, open, trustless oil trading. The possibilities for growth are considerable, particularly with novel offerings that capture high-volatility events in global finance through products that don't exist elsewhere.

As existing HIP-3 deployers and new entrants develop more sophisticated market designs, the infrastructure built during this crisis lays the groundwork for an entirely new class of commodity instruments onchain.

The infrastructure is in place. What deployers build next will determine whether Hyperliquid becomes a permanent venue for global commodity price discovery.