Hyperliquid

Introduction

Cerebras announced its IPO issue price at $185 a share on May 13th, against books reportedly 20x oversubscribed. Thirty million shares cleared at an implied market capitalisation above $48 billion, the largest US technology offering of the year. Only, a fraction of this allocation reached retail accounts.

The reason is structural. Underwriters distribute the bulk of any hot IPO to existing institutional clients: hedge funds, sovereign wealth funds, pension funds, and asset managers that route flow through the underwriting banks all year. Retail brokers receive a sliver, and the users of those brokers compete for that sliver through lotteries and minimum-balance gates. In a deal as hot as Cerebras, most retail accounts either received nothing or received insignificant allocations. The bulk of retail demand was routed through secondary markets where they bought the asset at a price well above where institutions were filled.

As a way around this limitation, sophisticated investors have historically turned to SPVs, or Special Purpose Vehicles. These are business entities formed for the purpose of pooling money from various investors to meet the minimum buy-in demands. While platforms like Hiive, Forge, etc. have made access to SPVs easier, they are generally not retail friendly. Further, with the news of Anthropic deeming them disallowed, the SPV workaround may be reaching the end of its lifespan.

[embed anthropic tweet on pre-IPO market position]

Prime brokers at the major banks write bespoke forward contracts on pre-IPO equity for hedge fund and family-office clients, but those require a prime-brokerage relationship, large credit lines, and seven-figure minimums.

Pre-IPO perpetuals close that access gap. Retail-accessible, continuously priced, and deep enough to absorb the size that matters. They are, by some distance, the cleanest mechanism retail has to participate in Pre-IPO summer on equitable terms.

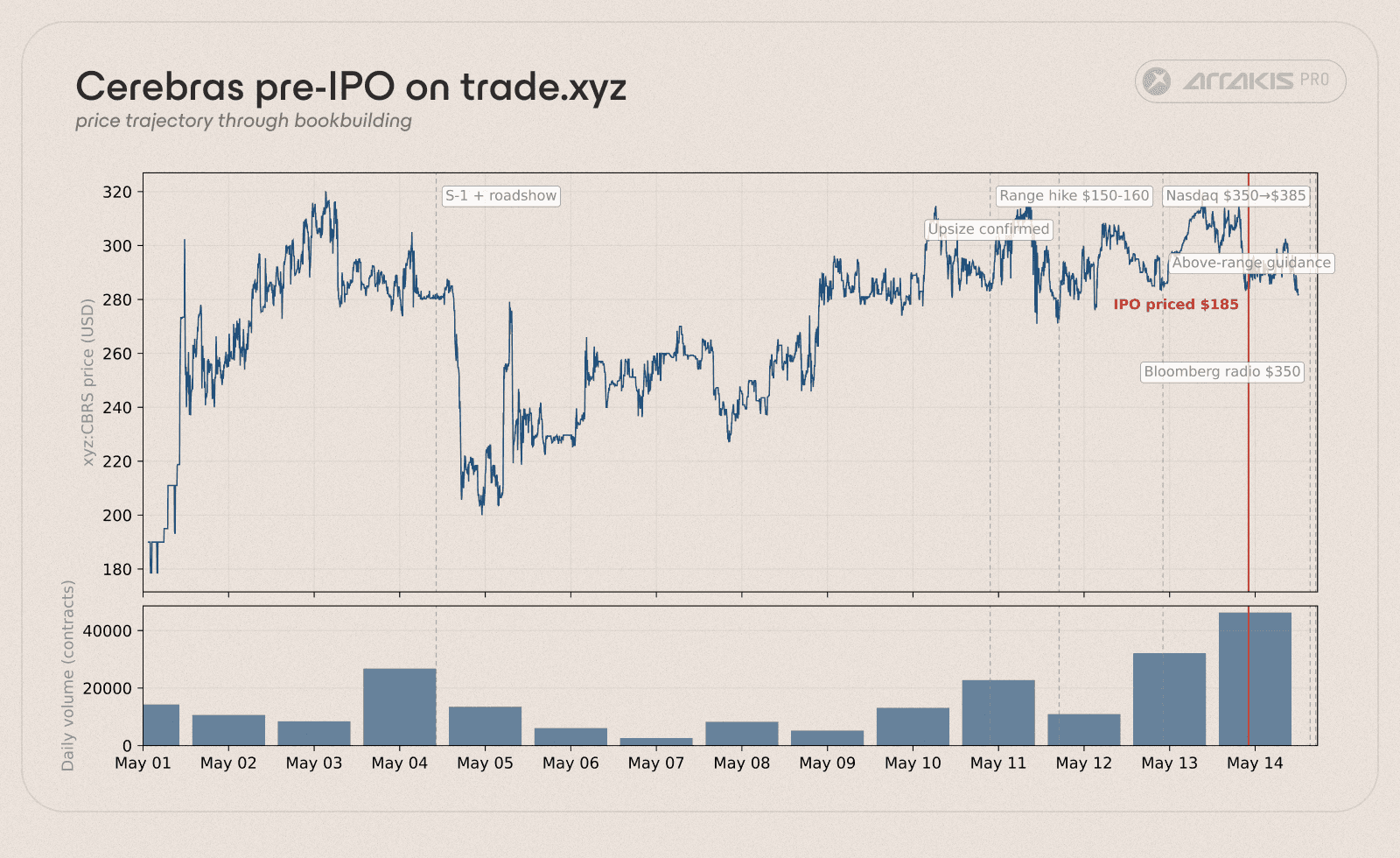

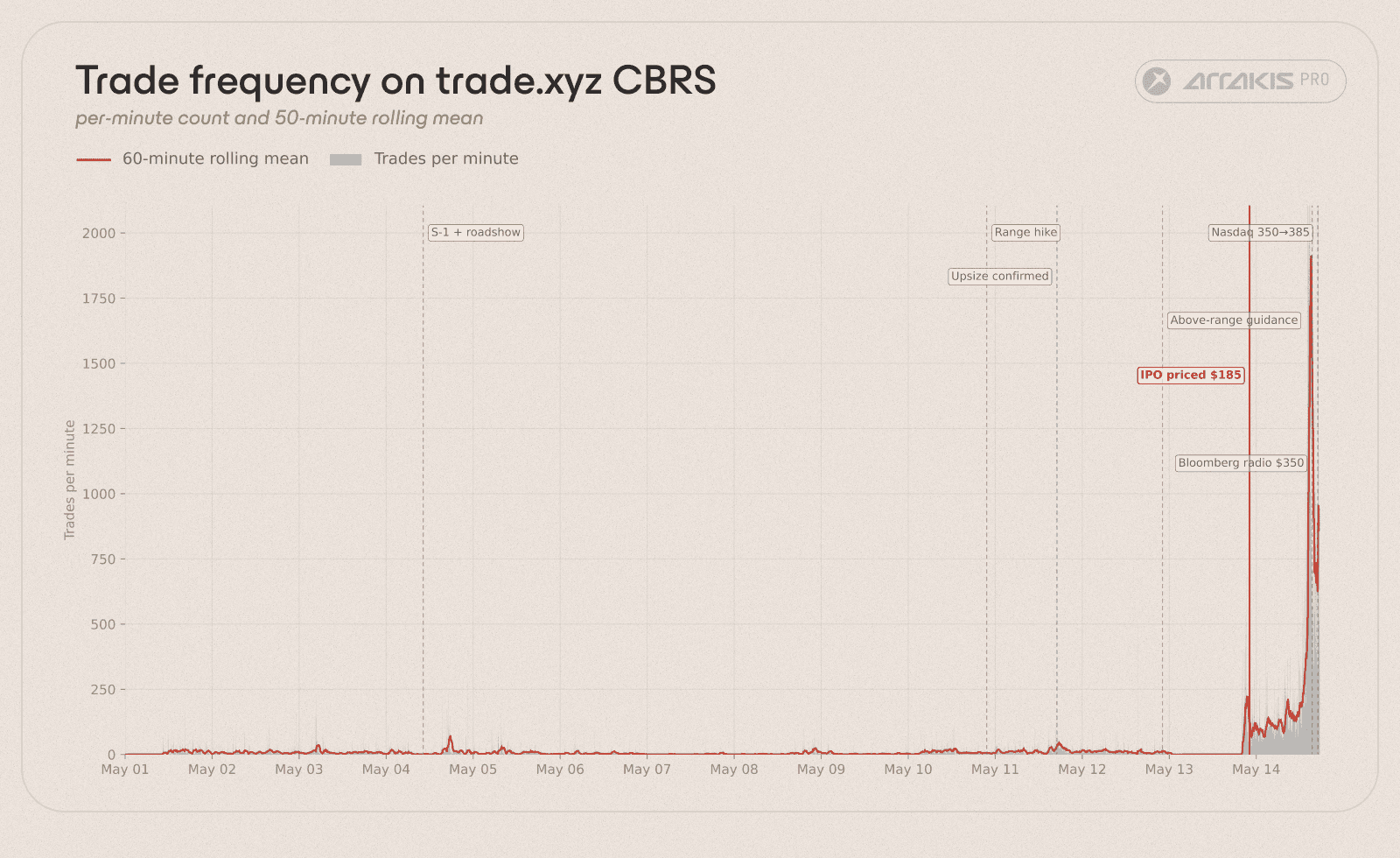

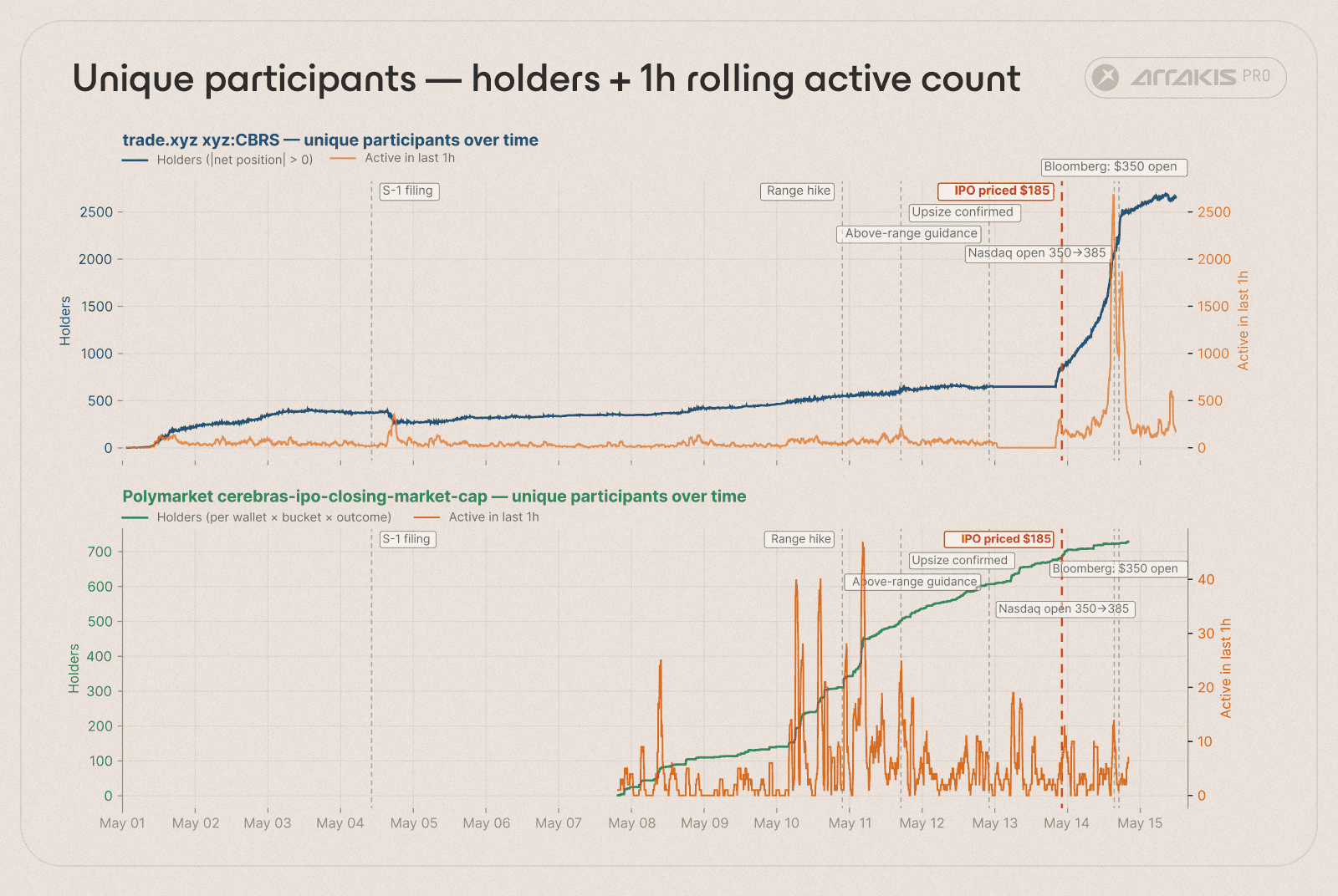

From 01:30 UTC on May 1, when the contract was first quoted, through the evening of May 13, when Cerebras priced and the perp converged toward its post-conversion mark, the trade.xyz CBRS perpetual was the only continuous retail-accessible CBRS price-discovery venue in the world. It quoted through every meaningful event in the bookbuilding window: the S-1 amendment, the range hike, the upsize, the pricing guidance. By the time Cerebras priced, the contract's twelve-day mid had absorbed every available datapoint and was quoting a price the underwriter's range could be measured against.

$CBRS is the first of many. The IPO pipeline through the next twelve to twenty-four months is dense with US tech and AI names: Stripe, Klarna, Databricks, Discord, OpenAI, xAI, Anthropic, and SpaceX are among the issuers expected to come to market. Each of these names will clear an institutional allocation that retail cannot reach, list at a Day-1 mark above the issue price, and leave most retail accounts buying into the secondary tape at a premium they did not get to set.

Pre-IPO perpetuals close this access gap. Retail-accessible, continuously priced, and deep enough to absorb the size that matters. They are, by some distance, the cleanest mechanism retail has to participate in this IPO summer on equitable terms.

What is a Pre-IPO Perpetual?

A Pre-IPO Perpetual (IPOP) is a cash-settled perp market that references the anticipated post-listing price of a pre-IPO company. Holders take exposure without holding a share, an allocation right, or any claim against the issuer. The instrument converts the discrete signals of the IPO process (filings, range updates, secondary prints, pricing wires) into a single continuous price.

A general prep market marks against an external oracle: a spot reference, futures basis, or index. A pre-IPO contract has no such oracle because the stock does not trade yet. Trade.xyz solves this with an internal pricing mechanism similar to the one its other perps run over weekends, when reference markets are closed. The oracle is a thirty-minute exponentially weighted moving average that advances via the market's own previous prices.

For pre-IPO contracts, trade.xyz applies a 0.005× funding multiplier on @HyperliquidX's funding rate formula, 1% of the 0.5× multiplier on a standard HIP-3 equity perp. Funding exists to pull a perp back toward its fair value anchor, but a pre-IPO contract has no fair value to pull it toward. Suppressing funding lets the market sit at large premiums or discounts for days without bleeding to carry, which is the only way the contract can express a forward view that diverges from any near-term reference price.

Discovery Bounds cap where the market can trade, to prevent a single order from running the book during low-liquidity periods while leaving headroom for the price to move on news events.

Once the underlying lists and regular-way trading begins on Nasdaq, the IPOP converts to a standard externally-priced equity perpetual with the conventional 0.5× funding multiplier. From that point, the perp marks against listed CBRS the same way xyz:TSLA marks against listed $TSLA.

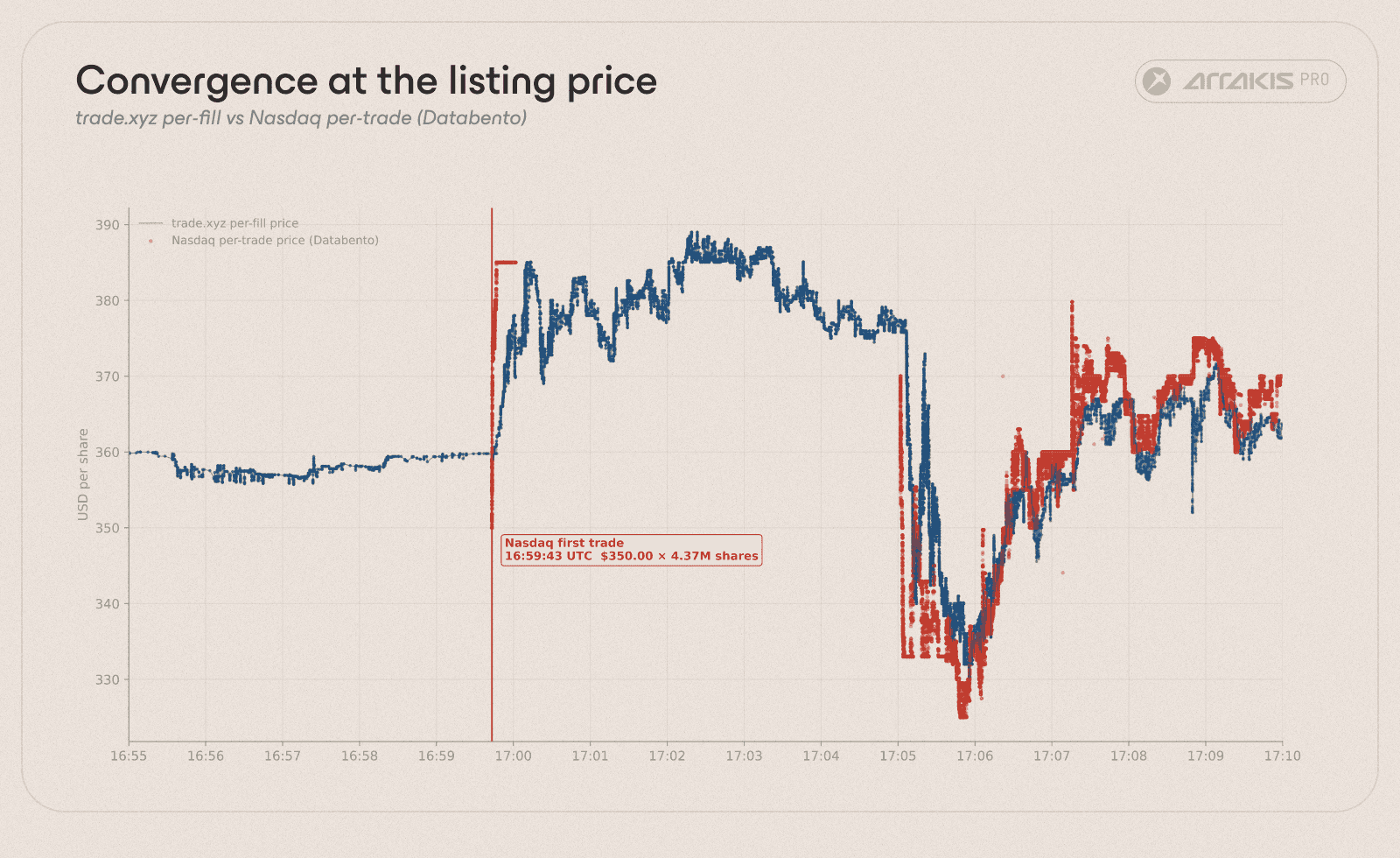

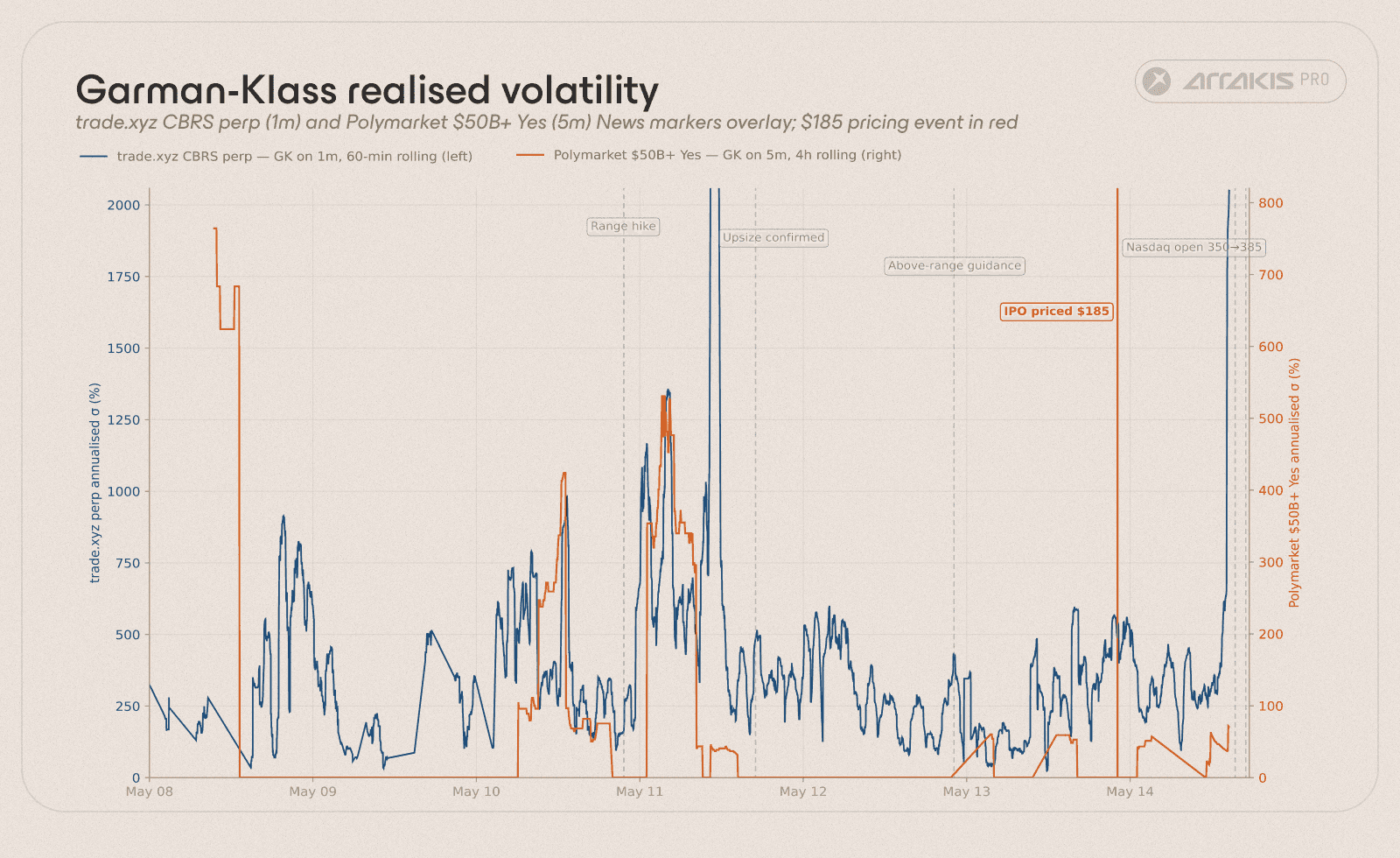

How Trade.xyz Tracked $CBRS's Listing Price

Trade.xyz deployed the CBRS perpetual at 01:30 UTC on May 1, three weeks before the listing date. The initial orderbook showed deployer-placed resting bids stepped between $50 and $125 with no asks. The first trade printed at $190 against the first deployer asks at 01:33 UTC. By the close of trading on May 3, three full days before the S-1 was amended, the contract had traded as high as $320.

The S-1 amendment landed on May 4 at 10:14 UTC with an initial range of $115 to $125, well below where the perp was already trading. The contract sold off to roughly $200 over the next twenty-four hours as informed leverage unwound, a move that ran through a two-hour cluster of more than nine hundred long-side liquidations during the 16:00 to 17:00 UTC window. By the end of the week it had ground back to $280 to $300.

The Reuters scoop on the upsized range hit the wire on the evening of May 10 at 21:39 UTC: $150 to $160 against an enlarged 30M-share offering. The perp's reaction was effectively flat. It was already trading at $307, almost twice the new range high. The May 11 session confirmed the upsize and added a further $1.68M of fresh short interest from a cohort of fourteen named wallets. Price closed near $290.

On the evening of May 12 Bloomberg reported pricing guidance tracking above the $150 to $160 range. The perp drifted higher over the following twenty-four hours and closed at $307 on May 13 at 20:01 UTC. Pricing landed at $185 a share roughly an hour later. The contract moved from $310 to $284 in the eighty-nine minutes between the pricing wire and 21:29 UTC, an 8.4% adjustment on roughly 8,600 contracts of post-news volume.

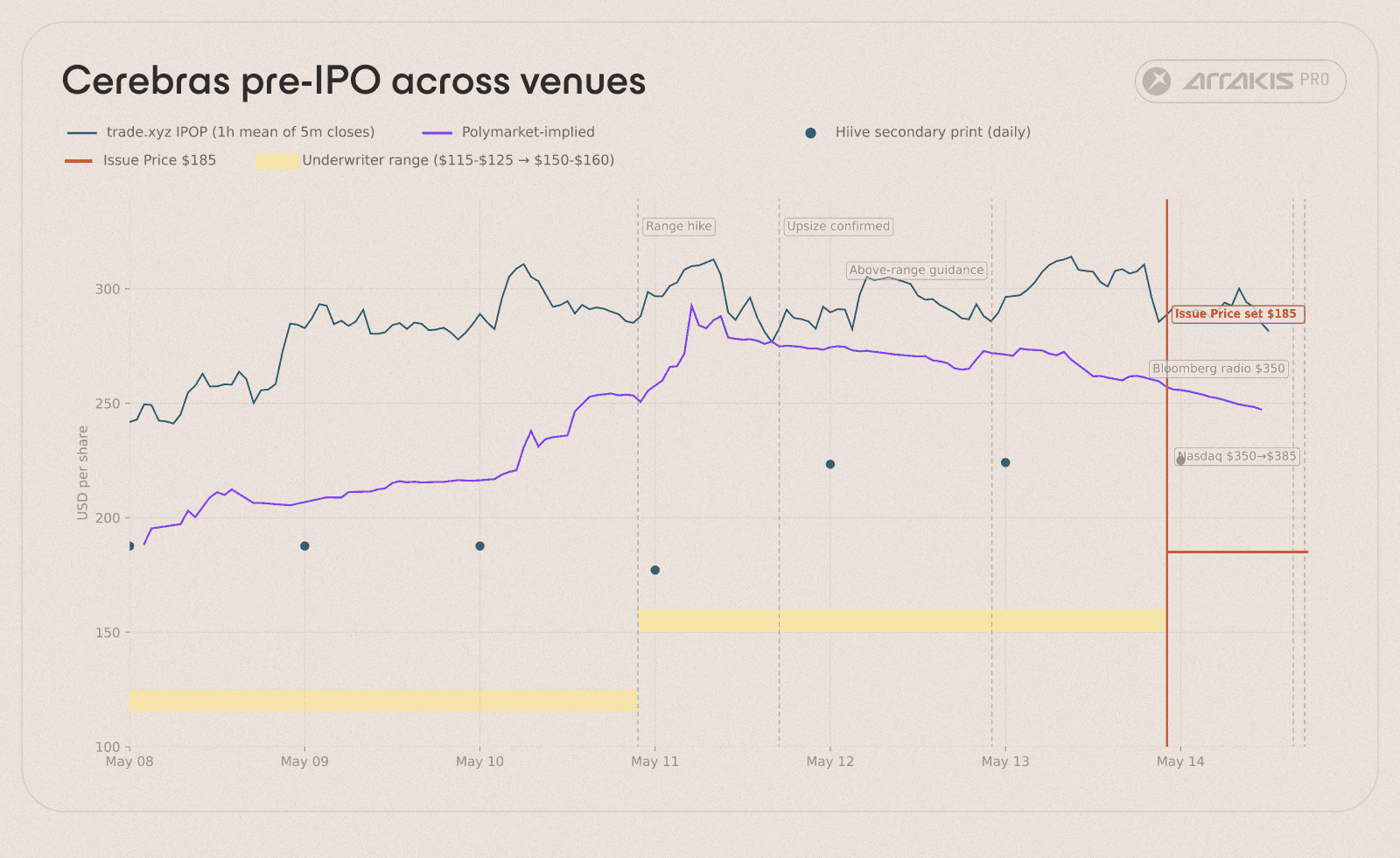

Three venues offered continuous quotes on Cerebras through the bookbuilding window: the trade.xyz HIP-3 perpetual on Hyperliquid, the Day-1 closing market-cap binaries on Polymarket, and the SPV trades on Hiive. Each of these traded at different price levels.

Polymarket: the implied close price

Polymarket was the only other retail accessible venue to take directional bets on the $CBRS price as it listed a "$CBRS closing market cap" market.

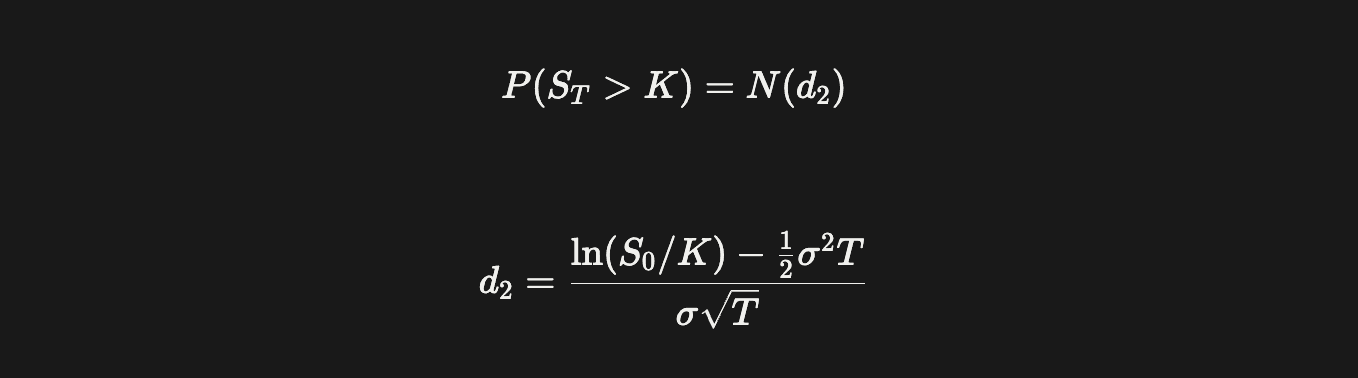

We decomposed the implied probability from this Polymarket into an estimate of expected close prices which requires assuming or forecasting Volatility of $CBRS for its first trading day.

This was done by looking at prior oversubscribed AI/tech IPOs and assuming CBRS follows a similar volatility regime on its first trading day.

Treating this as a digital option, and plugging in Black Scholes fair pricing equation:

where S₀ is the implied current fair price, K = $228 is the strike, and T ≈ 1 day to expiry. Solving for S₀ at the 95.8% implied probability across the historical band of comparable Day-1 realised volatilities:

Assumed annualised σ | Implied S₀ (Day-1 close point estimate) |

169% (band floor) | ~$267 |

205% (band median) | ~$276 |

311% (band ceiling) | ~$306 |

For a hot AI IPO with no prior realised volatility to anchor on, the defensible assumption band sits between 169% and 311% annualised. The historical anchor is the cluster of comparable hot tech and AI listings (Snowflake, Coinbase, Roblox, Arm, Astera Labs, Reddit), which cleared Day-1 realised volatilities in that range using the Parkinson high-low estimator on minute-resolution Nasdaq tape.

Listing | Listing date | IPO price | Day-1 close | Day-1 return | Parkinson σ (annualised) |

Snowflake (SNOW) | 2020-09-16 | $120 | $254 | +112% | 308% |

Coinbase (COIN) | 2021-04-14 | $250 | $328 | +31% | 311% |

Roblox (RBLX) | 2021-03-10 | $45 | $69.50 | +54% | 203% |

Arm (ARM) | 2023-09-14 | $51 | $63.59 | +25% | 178% |

Astera Labs (ALAB) | 2024-03-20 | $36 | $62.03 | +72% | 169% |

Reddit (RDDT) | 2024-03-21 | $34 | $50.44 | +48% | 207% |

Day-1 annualised realised volatility for comparable hot tech and AI IPOs, computed via the Parkinson high-low estimator. Band 169% to 311%, median 205%, mean 229%.

Taking the median 205% as the central anchor places the Polymarket-implied Day-1 close at roughly $276, about ten per cent below the trade.xyz perp's $307 pricing-eve mark. The contract on Polymarket is asking a different question from the perpetual on trade.xyz. The Polymarket binary is a probability of a closing-day market-cap threshold, conditional on the deal pricing at all. The trade.xyz perp is a forecast of the executable mid after the IPOP converts to a standard equity perpetual. The two prices can differ by a wide margin without either being mispriced relative to its own question.

Hiive: the price after a lockup

Hiive prints sit at the opposite end of the bookbuilding window. Through the last week of April, secondary trades on Hiive cleared at $102 to $107. The reason the print sat well below the perp's quote is structural rather than informational. Buyers on Hiive take delivery of pre-IPO shares, but are subject to long lockup terms. The holder cannot exit when the underlying first lists, instead having to . They have to wait six months, and sometimes longer, before the position is liquid. The price the Hiive market clears at therefore embeds a discount for the realised volatility of the asset across the lockup window, against an expected listing path that includes a meaningful probability of a Day-1 overshoot fading by the time the lockup unwinds. Trade.xyz had no lockup. Polymarket had no lockup. Hiive was the only quote of the three carrying a multi-month inventory risk on the buyer, and the spread between the Hiive print and the perp mark is, almost entirely, the price of that lockup.

Comparing the Major Venues

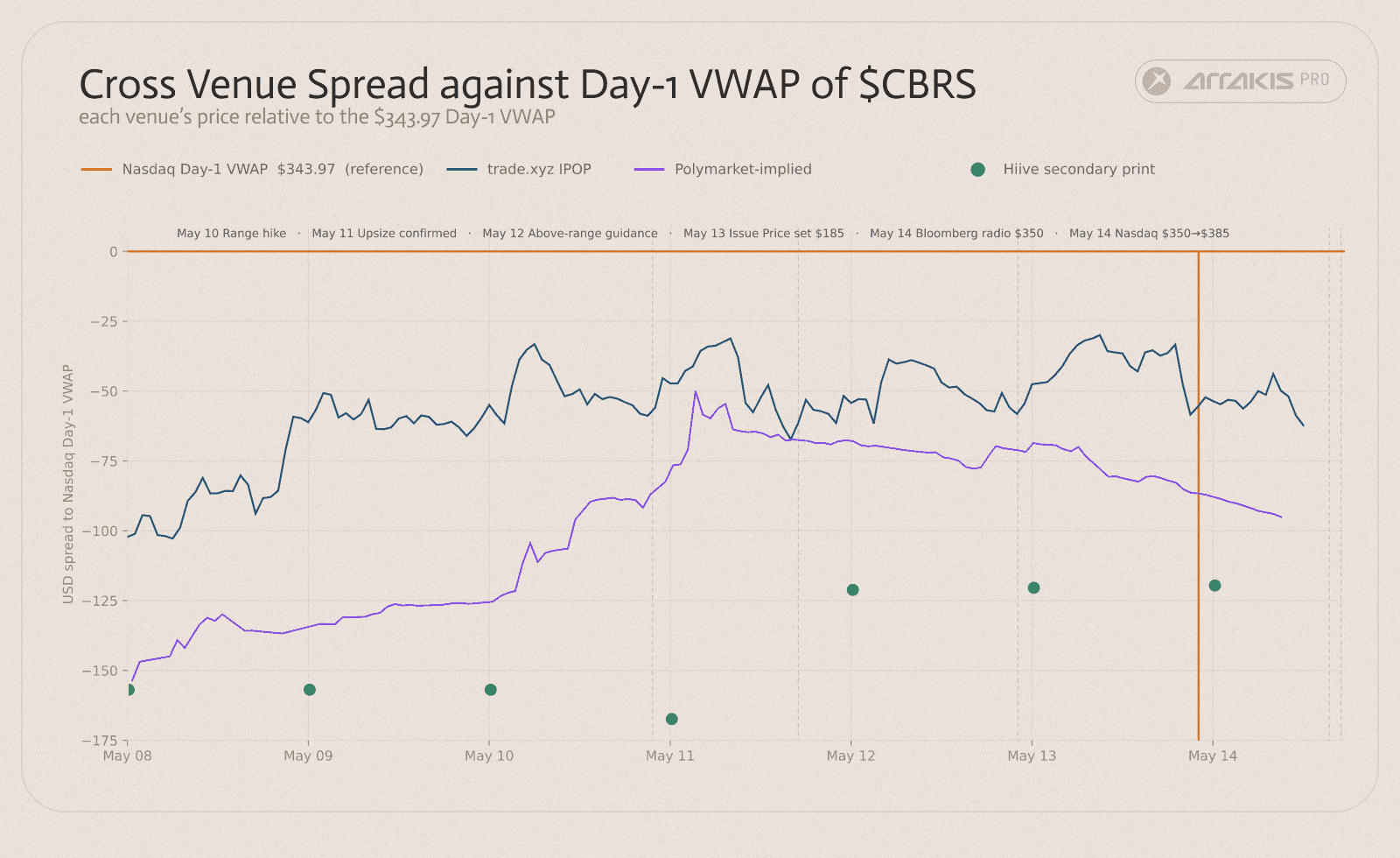

Polymarket anchors on the Day-1 close, the trade.xyz IPOP anchors on the post-conversion mark, and Hiive prices a lockup-discounted secondary share. The cleanest single comparison across all three is Figure 4: each venue plotted as deviation from the realised Day-1 close, the variable each one can actually be measured against. Trade.xyz was consistently closer to the realised post-listing price than either alternative, and it was the only one built to absorb the size that priced the perp's $307 mark.

The trade.xyz contract also requoted on news in real time. Bloomberg's report on the evening of May 12 that the range looked likely to clear above $160 was absorbed within minutes: orderbook quotes re-anchored higher, taker volume turned in the same direction, and the contract closed May 13 near $307 against an underwriter range still tracking $150 to $160. The same pattern repeated through the pricing wire itself, with the perp converging toward its post-conversion mark before the listing bell rang.

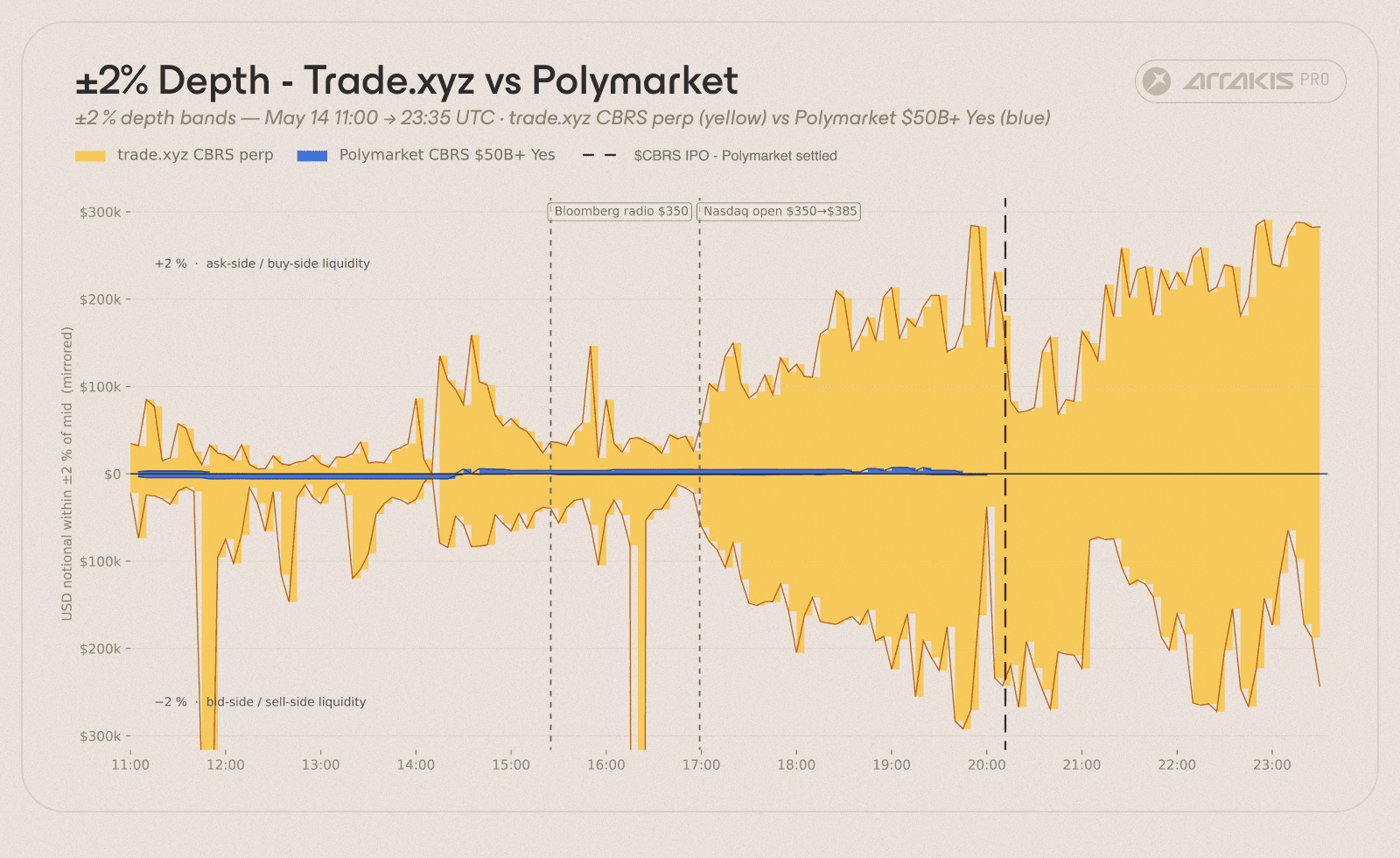

Liquidity

Trade.xyz was the deepest CBRS book of the three venues by an order of magnitude, which is why it held its quote through the pricing-day volume surge.

For any trader with meaningful size, Polymarket was untradable. Binary outcome markets clear in tens of thousands of dollars at the top of book during quiet hours. A hundred-thousand-dollar conviction on the Day-1 close would walk the Polymarket book through more than five hundred basis points of impact to fill. The same trade on trade.xyz filled at twenty to thirty basis points.

This is why $70.7M of total notional cleared across 208,854 fills on the perp over twelve days, and why the same window on Polymarket cleared a fraction of that. Depth on the perp held through every news event, and the contract absorbed institutional-scale conviction without dragging its quote off the running fair value.

A continuous quote, retail-accessible execution, and a book deep enough for six-figure conviction trades to fill without dragging the mark: trade.xyz was the only venue that combined all three.

The Winners and Losers

Market-structure analysis explains how the venue priced. It does not say who came out ahead. The participants who captured the largest leverage-adjusted returns over the bookbuilding window are the cleanest read on whether the access thesis held in practice.

We took the top ten wallets by percentage return on margin on xyz:CBRS, defined as realised PnL divided by entry-price notional adjusted for each position's effective leverage. Every address was passed through Arkham Intelligence, with a recursive backtrace on the first inbound funder for any wallet that carried no direct identity tags.

# | Address | % return on margin | Realised PnL | Identity |

1 |

| +268.4% | $36,411 | Polymarket + ENS + Twitter |

2 |

| +178.8% | $19,590 | ENS |

3 |

| +138.8% | $19,001 | Funded by a Polymarket account |

4 |

| +134.2% | $8,053 | Polymarket |

5 |

| +133.9% | $5,539 | Unattributed (Bybit deposit) |

6 |

| +133.7% | $6,073 | Polymarket |

7 |

| +133.5% | $15,378 | ENS |

8 |

| +118.0% | $12,306 | Unattributed (OKX deposit) |

9 |

| +116.3% | $52,710 | Polymarket |

10 |

| +105.0% | $9,294 | Polymarket |

Eight of the ten wallets carry a retail-shaped Web3 identity profile. Five resolve to Polymarket-active accounts. Two hold ENS names. One is triple-stacked across Twitter, Polymarket, and ENS. One is itself unattributed but was funded by another Polymarket-named wallet. The remaining two have no on-chain identity beyond a centralised exchange deposit, one from Bybit and one from OKX, which is the same shape the rest of the table presents minus a public handle. None of the ten resolves to an institutional desk, a known market maker, or a fund.

This is the access asymmetry from the introduction showing up in realised PnL. The Cerebras allocation cleared overwhelmingly to clients of the underwriting banks at $185 a share. The continuous price-discovery venue that ran in parallel to that allocation placed its biggest leverage-adjusted gains in wallets that match the demographic the underwriting process screened out. The traditional shape on a hot IPO is that institutions receive the allocation and retail buys the secondary at a premium. On the trade.xyz perp the order was inverted: the wallets that would not have received a share allocation captured the most upside on the only continuous market that priced the deal in real time. The House all Finance thesis is partly about who gets to trade. On this contract, the answer was the audience the venue was designed to reach.

Conclusion

Traditional financial markets are full of products the average retail consumer cannot reach. Pre-IPO exposure is the cleanest illustration of that asymmetry. Oversubscribed IPOs clear overwhelmingly to clients of the underwriting banks, the secondary market opens at whatever price retail demand can sustain against the institutional cost basis, and the venues that exist to bridge that gap (SPV platforms, forward contracts, prime-broker derivatives) replicate the access conditions of the primary market rather than dissolve them.

Hyperliquid is moving in a direction that flattens that gradient. The IPOP design is one of several primitives the venue is shipping to bring instruments that have historically been institutional-only into a retail-accessible perpetual form. A retail account on a HIP-3 deployer pays the same fee schedule as a hedge fund on the same contract, and both fill against the same book. The thesis the project keeps coming back to is that Hyperliquid intends to House all Finance, and the CBRS perp is the first hot US tech IPO that ran through that infrastructure end-to-end.

Cerebras priced on May 13 at $185 above its raised range with books reportedly twenty times oversubscribed. The trade.xyz CBRS perpetual cleared $70.7M of pre-pricing notional across 208,854 fills and 2,148 distinct addresses over twelve days. It tracked the underwriter's range through every meaningful event, absorbed institutional-scale conviction without breaking its quote, and converged toward its post-conversion mark within minutes of the pricing wire. The first major US tech IPO with a continuous pre-IPO perpetual on a Hyperliquid deployer happened twelve days ago. There are more coming. Welcome to Pre-IPO summer.

Hyperliquid.