Deep Dive

TL;DR

The method used to distribute tokens determines how much sell pressure hits the market, when it arrives, and whether liquidity can absorb it. Most teams size each mechanism independently: an airdrop here, an exchange allocation there, a pre-sale on top. The result is compounding sell pressure that overwhelms thin markets in the first 48 hours. The tradeoff is not which mechanism is best. It is which combination, sized together against available liquidity, matches your resources and timeline.

Cost Basis and Sell Pressure

Before evaluating distribution mechanisms, it helps to define the two variables that determine their outcomes.

Cost basis is what a token holder paid to acquire their position. It shapes sell behavior because it sets the threshold at which selling becomes rational. An airdrop recipient with zero cost basis has no financial downside from selling immediately. A pre-sale participant who paid $0.50 per token needs the price above entry to justify holding, but will still sell once the unrealized gain is large enough to take profit. An exchange that received tokens as a listing allocation treats them as revenue to be converted.

But cost basis alone does not determine sell pressure. Supply allocations have a major role to play.

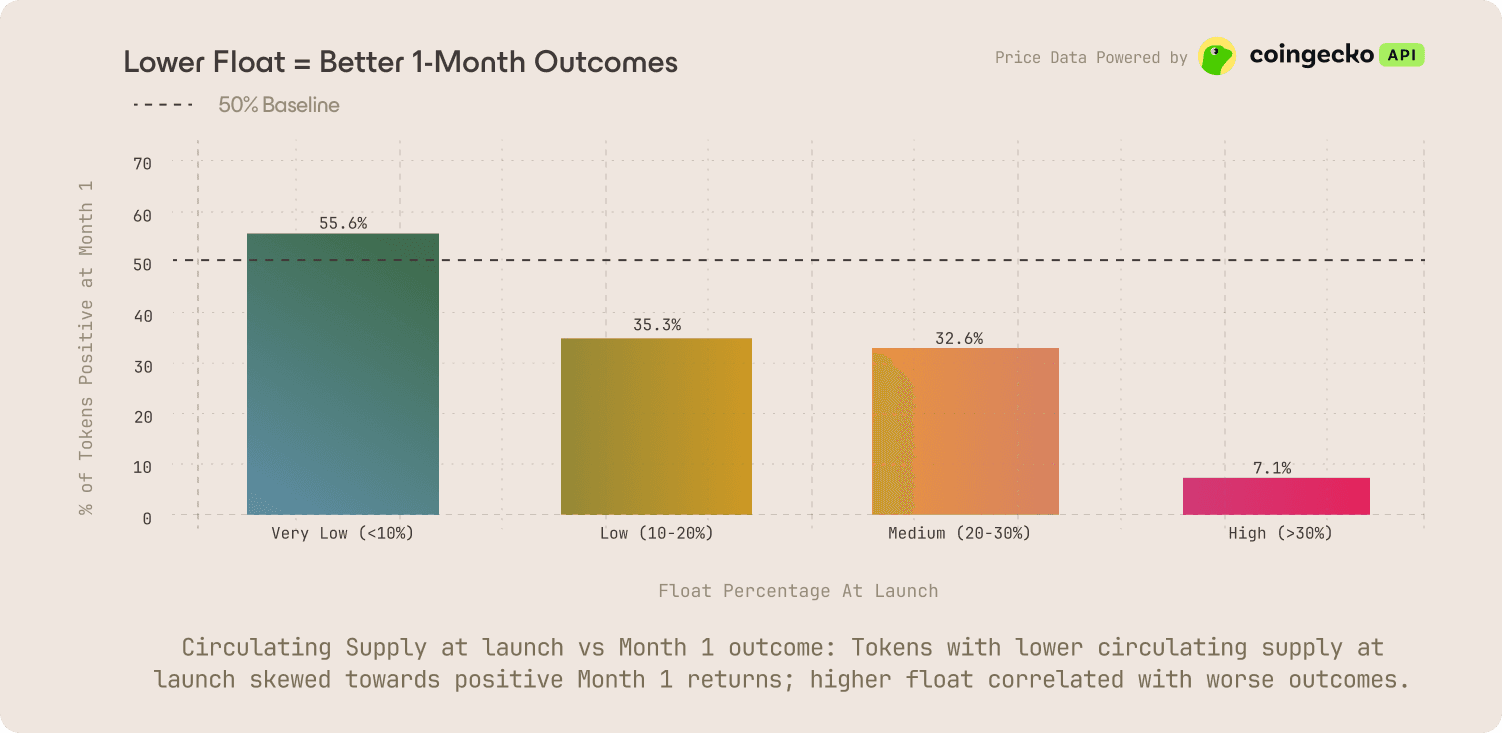

Sell pressure is the aggregate effect of individual sell decisions hitting the market against finite liquidity. A 3% airdrop and a 5% airdrop produce the same per-recipient incentive; both have zero cost basis. The difference is the total volume of selling that hits the order book, and whether liquidity can absorb it. A well-designed airdrop with excessive allocation still overwhelms thin markets. A poorly designed airdrop with conservative sizing can survive.

Every distribution mechanism produces a different cost basis in the hands that receive tokens, and a different volume of sell pressure against the available liquidity. Cost basis determines who sells and when. The size of the allocation relative to liquidity depth determines what happens to the price.

What Are Token Distribution Mechanisms?

There are four major types of token distribution mechanisms founders opt for at launch. Each creates structurally different sell pressure, at different times, with different retention profiles.

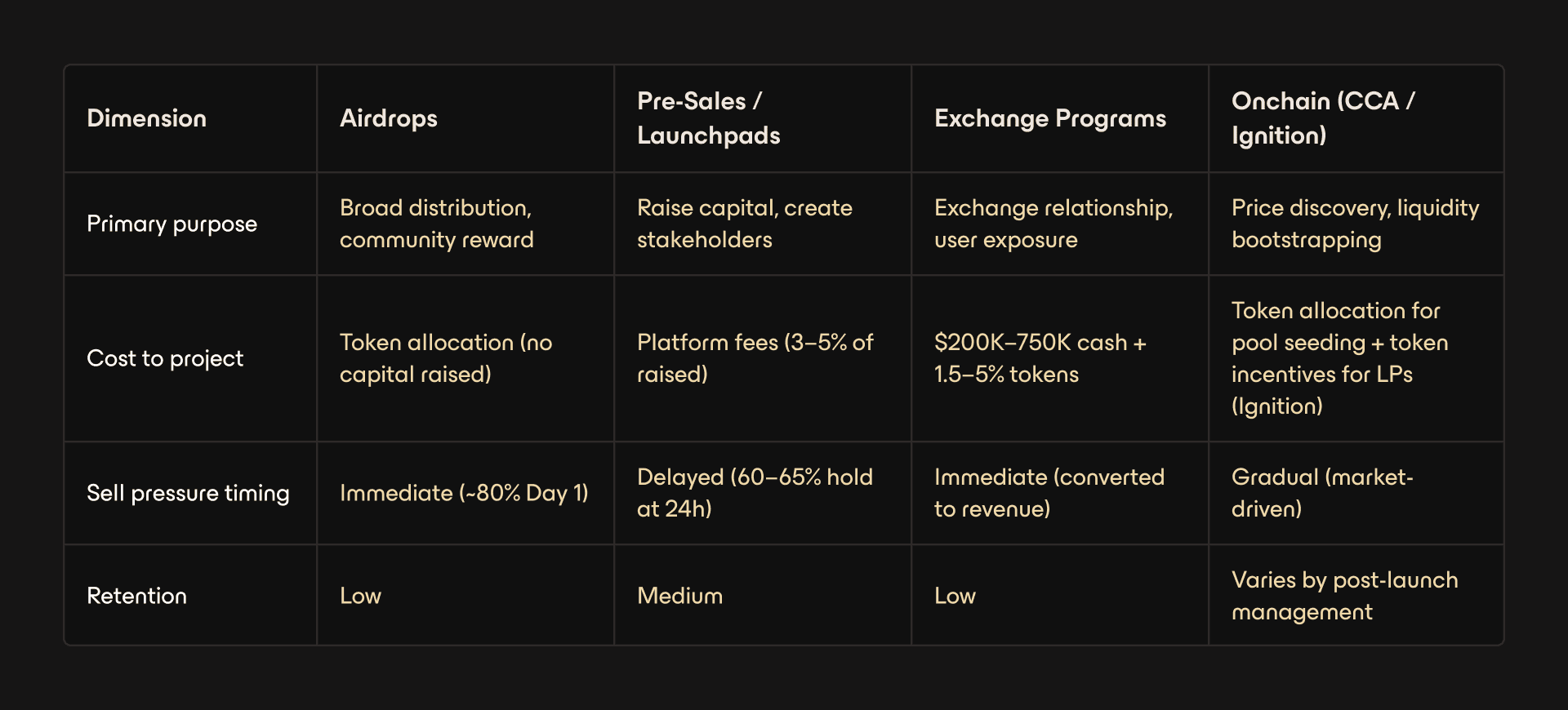

Airdrops distribute tokens to existing users based on historical behavior. Recipients receive tokens at zero cost basis. The primary purpose is broad distribution and community reward.

Pre-sales and launchpads exchange tokens for capital before TGE. Participants acquire tokens at a known price and have skin in the game. The primary purpose is raising capital while creating a stakeholder base.

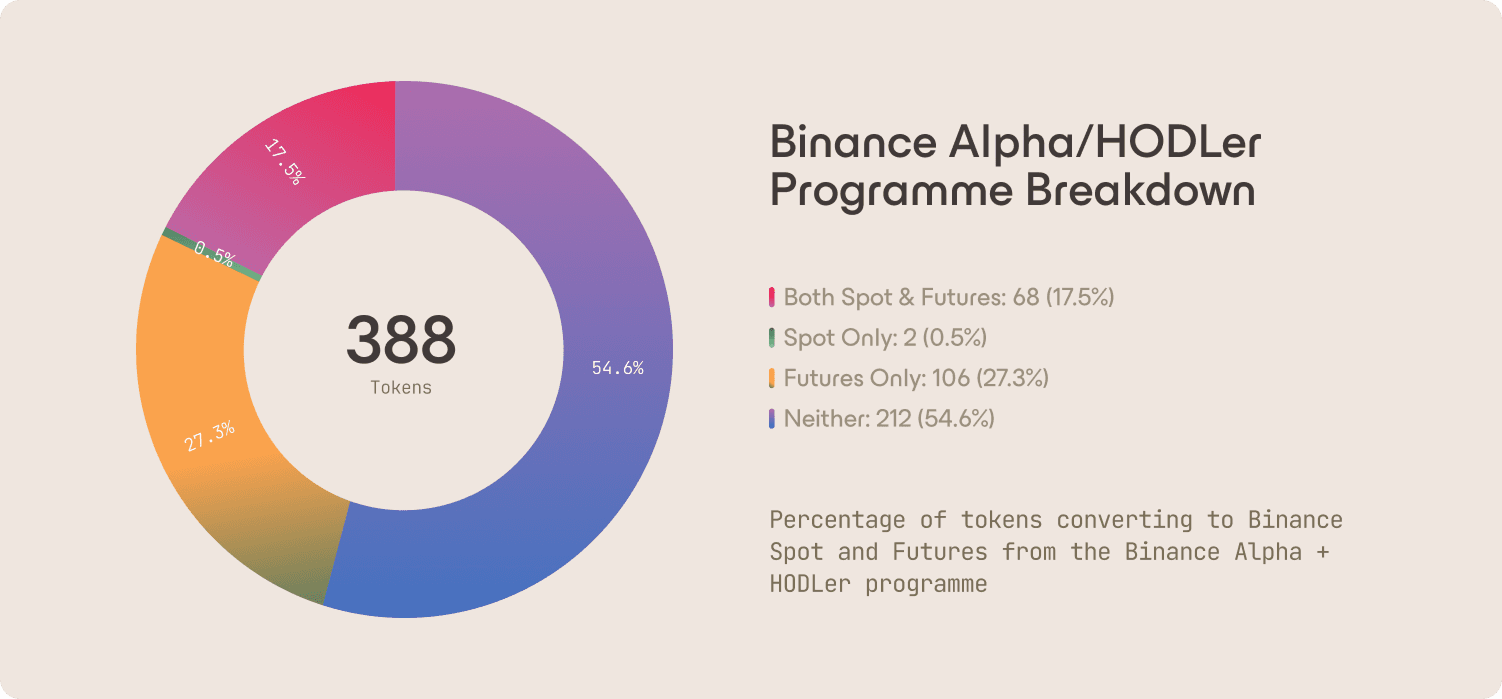

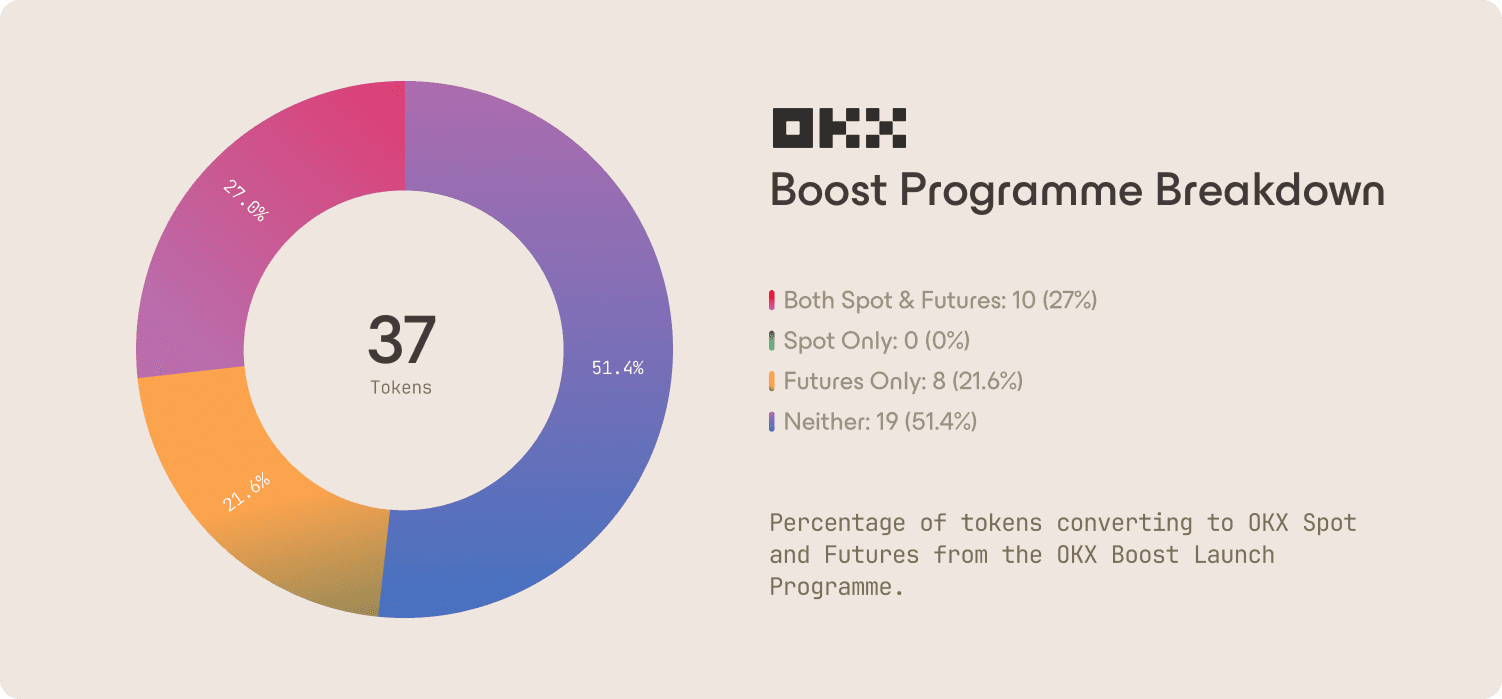

Exchange-affiliated programs allocate tokens to centralized exchanges in return for listing access, user exposure, and marketing. Programs like Binance Alpha, OKX Boost, and Bybit Token Splash are the most common. The primary purpose is distribution reach and exchange relationships.

Onchain launch mechanisms use smart contract-based auctions to establish market-driven prices and seed liquidity permissionlessly. Uniswap Continuous Clearing Auctions (CCA) and Aerodrome Ignition are the leading approaches. The primary purpose is transparent price discovery with automatic liquidity bootstrapping.

These are not interchangeable. Each answers a different need and carries a different cost in sell pressure.

How Does Each Mechanism Affect Sell Pressure?

Airdrops

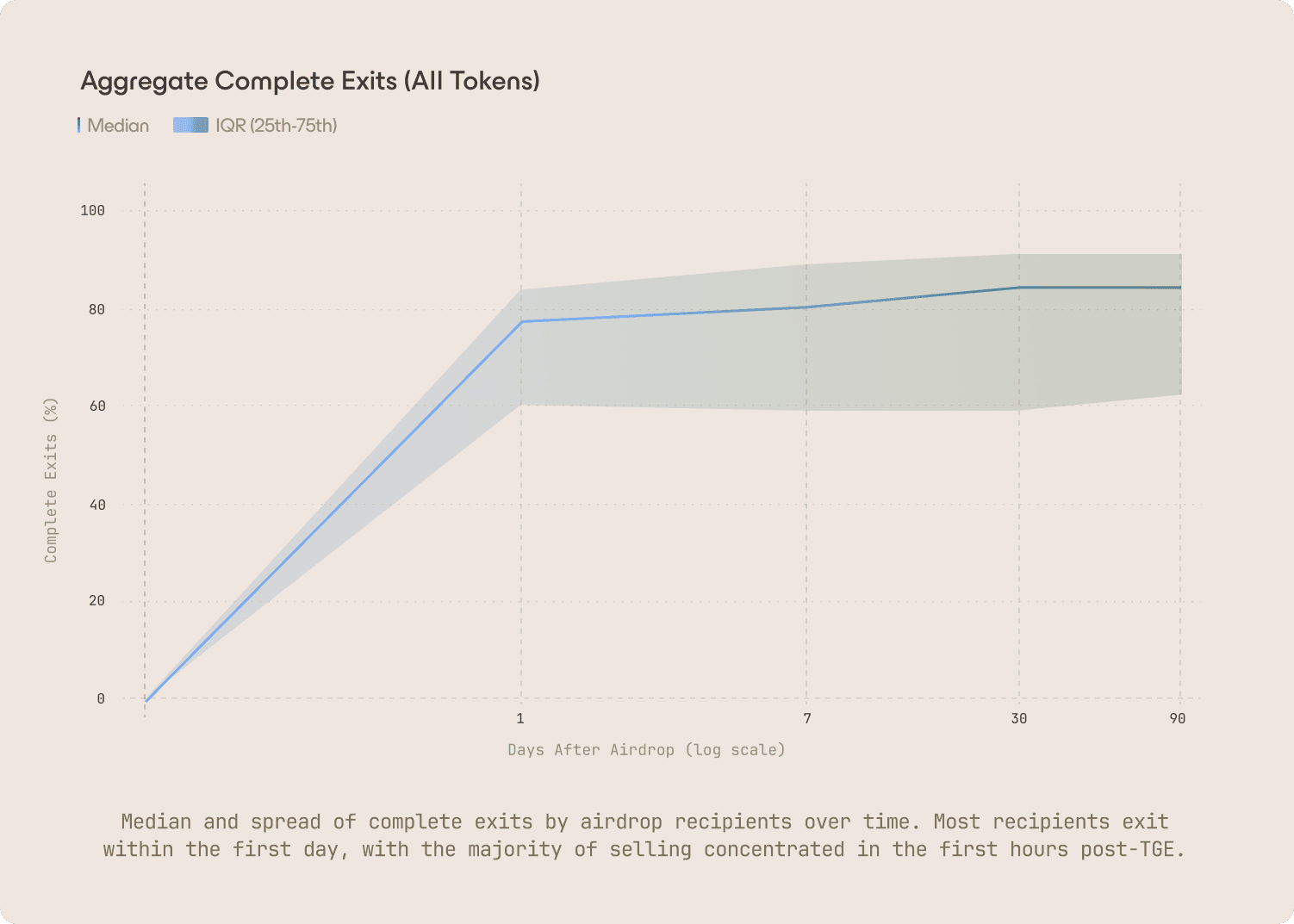

Airdrops produce the most immediate sell pressure of any distribution mechanism. Recipients have zero cost basis, and the rational action for most is to sell immediately.

Our analysis of the largest airdrops of 2025 confirms this: up to 80% of recipient addresses completely exited within the first day.

The baseline assumption should be that most of an airdrop will be sold. Design levers exist: sybil filtering, call option mechanisms, and revenue-based allocation models have each produced measurably better retention in specific launches. But none eliminate the structural reality of zero cost basis. The question is not whether airdrop recipients will sell, but how many and how fast.

Sizing follows directly: treat the airdrop allocation as immediate sell pressure and size it to what your day-one liquidity can absorb. Larger is not better if it collapses confidence in the first 48 hours.

Pre-Sales and Launchpads

Pre-sale participants show meaningfully different behavior. Data from CoinList indicates 60–65% retention after 24 hours, compared to 20–30% for airdrops. After 30 days, roughly 40% still hold. Cost basis changes incentives.

However, retention erodes with price appreciation. If the token rises sharply post-launch, sell pressure increases regardless of acquisition method.

A structural consequence that most teams underestimate: projects running multiple pre-sale rounds at different valuations create internal cohort dynamics. Later-round participants effectively provide exit liquidity for earlier rounds with lower cost bases. Each cohort has a different price at which selling becomes rational.

The pre-sale must be fully subscribed. Undersubscription signals to the broader market that participants offered early access at favorable terms still chose not to participate. Size conservatively relative to realistic demand.

Exchange-Affiliated Programs

Exchanges monetize launches through direct cash payment, token allocations, or the expectation of trading fees once listed. The most common programs today are Binance Alpha, OKX Boost, and Bybit Token Splash. The token allocations for marketing programs, trading competitions, and listing requirements should be modeled as immediate sell pressure. These tokens are typically converted to operating revenue.

Depending on the program, projects should expect to allocate $200K–750K in stablecoins and 1.5–5% of token supply. Projects should also keep in mind that there is a risk of impermanent loss as they’re acting as the LP. In many cases, participation does not guarantee a Spot listing outcome.

A dynamic multiple founders reported in our interviews: exchanges may use pre-sale capital as leverage. Knowing capital has been raised, they push for higher fees or larger allocations. Founders should be prepared for this and willing to walk away from unfavourable deals.

Onchain Launch Mechanisms

Onchain mechanisms are structurally different from the other three. They are the only distribution approach that simultaneously handles price discovery, token distribution, and liquidity bootstrapping.

Uniswap CCA extends uniform-price auctions into continuous time. A project commits a portion of their token supply to an auction that runs over hours, days or weeks. Bidders place orders specifying a maximum price per token and total budget. Each bid is streamed into sub-bids across all remaining blocks after submission. At the end of each block, a clearing price is set: the highest price where cumulative bids meet or exceed that block's token allocation and all bidders receive the same token price. As demand builds against fixed supply, price rises, rewarding early bidders with a better average price and reducing sniping, gas wars, and timing games. Upon clearing, proceeds can automatically seed a liquidity pool at the final price. Aztec Network's December 2025 TGE demonstrated the model at scale: ~$59M raised from 16,741 participants with 30–40% lower volatility than comparable formats.

Aero Ignition activates Aerodrome's flywheel as part of a TGE strategy. A project first deposits a small portion of its token supply as incentives for a pool on Aerodrome. veAERO holders then vote for the pool to earn those tokens, directing AERO rewards that will stream the following week. Voters then receive their token rewards and AERO begins streaming to the pool. Liquidity providers, which can include the veAERO voters themselves, deposit two-sided liquidity to earn AERO rewards. Deep liquidity enables the pool to capture volume and generate trading fees, which attract future votes/AERO rewards. With sufficient depth and distribution via Aerodrome, price discovery can occur onchain via the Aerodrome pool even when running alongside CEX listings.

In both cases, long-term outcomes are determined by how liquidity is operated once the distribution phase ends. Arrakis works with issuers before launch to ensure that protocol-owned liquidity delivers efficient markets with concentrated depth at the trading price, and durable fee capture from day one. Teams planning a CCA or Ignition launch should treat liquidity management as part of the launch planning itself, not something to figure out after trading begins.

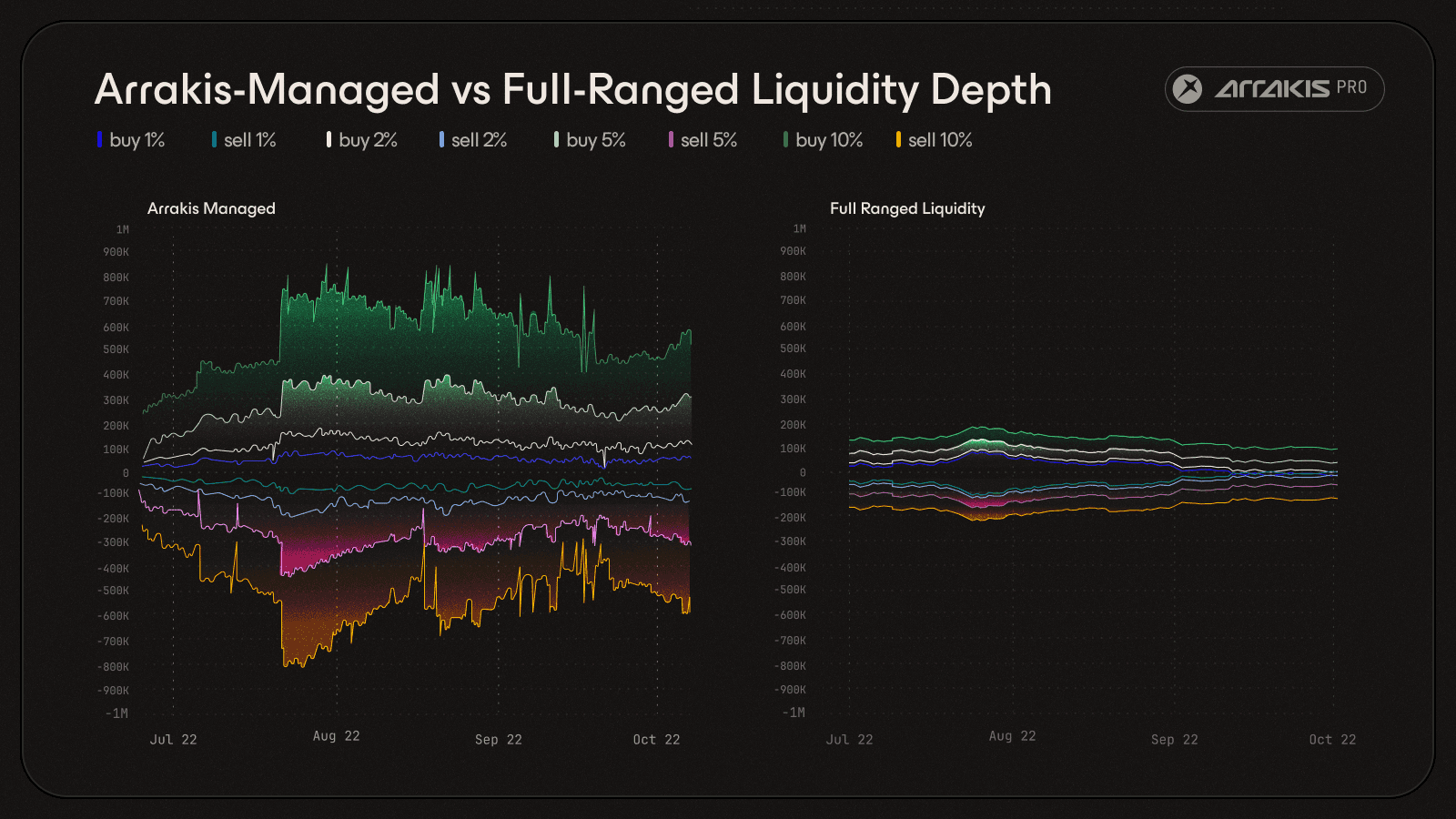

Concentrated management (left) delivered up to 3× greater depth per dollar deployed versus passive full-range positioning (right) for VSN on Uniswap.

Why Do Most Teams Underestimate Total Sell Pressure?

Three structural dynamics work against founders who size each mechanism independently:

The mechanisms compound against the same supply. Distribution mechanisms, exchange allocations, and market maker loans all draw from the same circulating supply. A project at $100M FDV with 10% float, a 5% airdrop, 3% exchange allocation, and 2% market maker loan faces ~$8M in potential sell pressure from $10M in circulating supply.

Sell pressure is quantifiable; buy pressure is not. Analysis by Simplicity Group of 50,000+ data points from 40 major 2025 launches found that social media engagement has a near-zero correlation of just 0.038 with price performance. VC funding showed no statistically significant correlation with returns. Every distribution decision creates measurable sell pressure that arrives immediately at TGE. Durable buy pressure in the form of utility-driven demand, integrations, and revenue-backed buybacks, builds over time and cannot be front-loaded. Founders should size distributions conservatively based on how much sell pressure day-one liquidity can absorb. To simulate sell pressure at TGE, use Delphi’s Sell Pressure simulator.

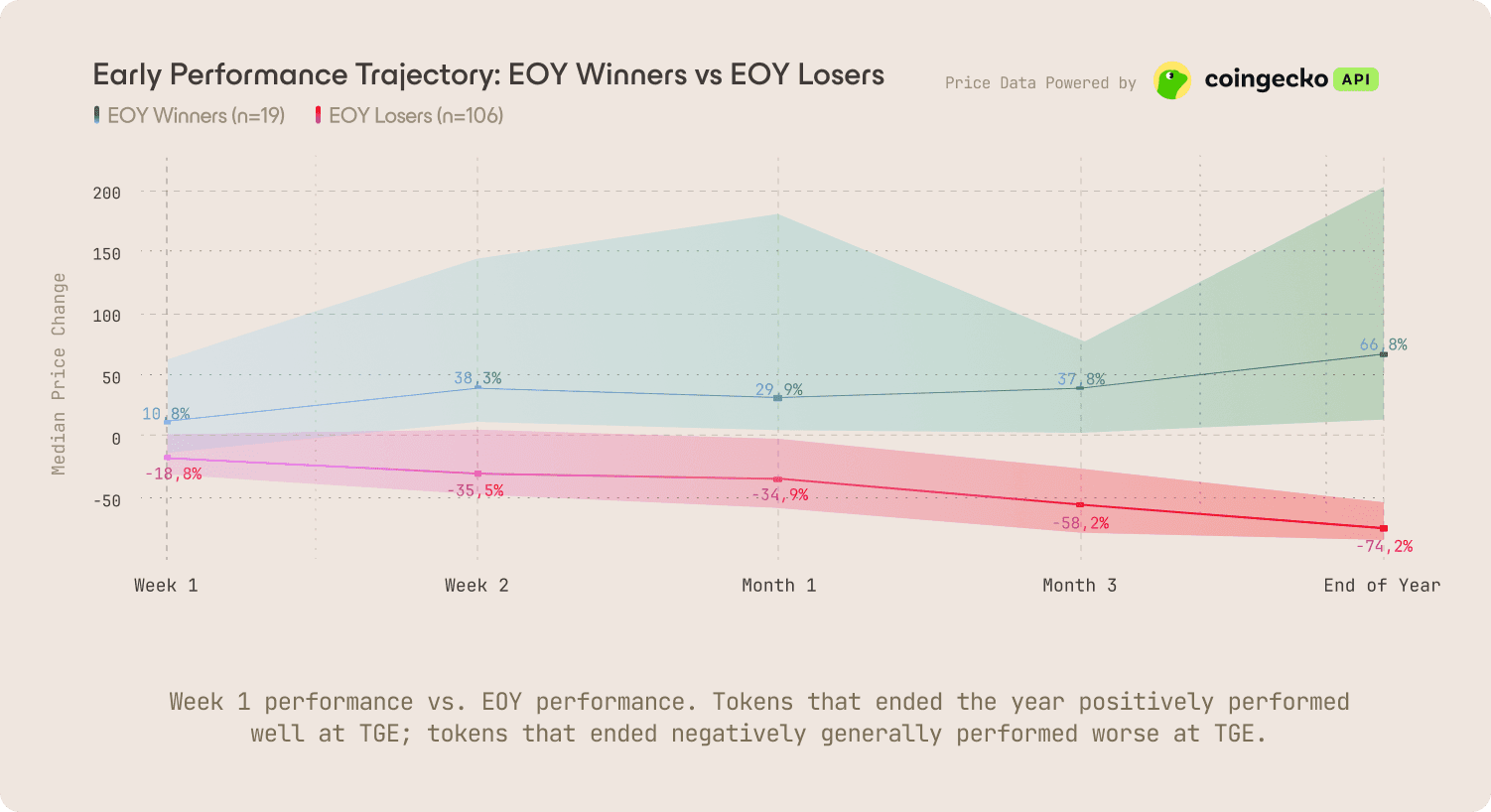

Week 1 is nearly irreversible. Our analysis of 125 token launches in 2025 found that only 9.4% of tokens declining in their opening week recovered to positive returns by year-end. 85% ended the year negative. A positive first week does not guarantee success: 72.5% of tokens that rose in Week 1 still ended the year negative. But a negative first week is nearly fatal. The structural decisions that determine the outcome are made months before TGE. Their consequences arrive in the first 48 hours.

The sizing process works in a specific order. Exchange allocations are typically non-negotiable; establish those constraints first. Assess market maker and liquidity needs next. What remains is the maximum airdrop or pre-sale capacity. Work backward from what your liquidity can absorb, not forward from what feels generous.

How Should Founders Compare Distribution Mechanisms?

Practical Considerations

No single mechanism is optimal. Most successful launches combine two or three, each serving a different function.

Airdrops make sense when the project has a large existing user base to reward and sufficient liquidity to absorb the resulting sell pressure. Protocols with limited retail dependency may skip airdrops entirely; it’s not a prerequisite for TGE.

Pre-sales make sense for early-stage projects that need capital and credibility. Projects with established products, users, and revenue may gain less from sharing economics with an intermediary.

Exchange programs make sense when the exchange relationship delivers meaningful distribution reach. The math should work on a cost basis: if the exchange historically delivers thin volume, the allocation is misspent regardless of the listing exposure.

Onchain mechanisms make sense for projects that value transparent price discovery and want to bootstrap protocol-owned liquidity from day one.

In contrast to airdrops and pre-sales, both exchange programs and onchain mechanisms create functioning DEX spot markets as part of the distribution event. The difference is ownership and transparency: onchain mechanisms produce protocol-owned liquidity with permissionless price discovery, while exchange programs create markets on terms and infrastructure controlled by the exchange.

The right combination depends on resources, timeline, and sell pressure tolerance. There is no universal template.

What Are the Key Lessons for Founders?

Onchain mechanisms solve distribution and price discovery simultaneously. CCA and Aerodrome Ignition bootstrap a functioning market as part of the distribution event itself. But distribution is phase one, active liquidity management is phase two.

Cost basis determines sell behavior; allocation size determines market impact. Zero cost basis (airdrops) produces immediate selling. Positive cost basis (pre-sales) produces delayed selling. But a conservatively sized airdrop can outperform a generous pre-sale if the total sell pressure exceeds what liquidity can absorb.

Size backward from what your liquidity can absorb, not forward from what feels generous. The question is not "how much did Hyperliquid airdrop?" It is "how much combined sell pressure from airdrops, exchange allocations, and market maker loans can our liquidity absorb in Week 1?" Start with exchange commitments (non-negotiable), add market maker needs, then allocate whatever remains. The sum of all sell pressure, not any single allocation, determines whether Week 1 is survivable.

Week 1 is nearly irreversible. Only 9.4% of tokens that declined in their opening week recovered by year-end. A strong launch is necessary but not sufficient for success, while a weak one is nearly unrecoverable. Getting the sizing of distribution mechanisms based on realistic sell pressure right can meaningfully change outcomes.

The full sizing framework and a recommended week-by-week timeline are in our Practical Guide to TGE. To structure liquidity for your launch, schedule a call with the Arrakis team.

Thanks to Uniswap, Delphi, and CoinList for their contributions to this article.

Disclaimer

This article is provided for informational and educational purposes only. Nothing in it constitutes financial, legal, tax, investment, or professional advice. Market conditions, deal structures, and fee terms referenced here reflect information available at the time of publication and are subject to change. Readers should independently verify all figures and terms with relevant counterparties before making any decisions. Arrakis makes reasonable efforts to ensure accuracy but does not warrant that all information is complete or current.