Deep Dive

TL;DR

How you design your DEX liquidity determines price impact, fee capture, and MEV exposure. Most teams deploy whatever capital remains after CEX allocations into a passive full-range pool and move on. The result is shallow depth where normal sell pressure produces outsized price impact, fee capture falls short, and MEV bots extract value continuously. DEX liquidity is not a single deployment decision. It is a series of design decisions around positioning, ownership, venue, sizing, starting inventory, fees, management, and MEV protections. This guide walks through each one.

Liquidity Depth and Price Impact

When teams deploy DEX liquidity, most treat TVL as the success metric and move on. But TVL measures total capital in the pool, not how much of it sits around the active trading price. A $3M full-range pool can deliver worse execution than a $1M concentrated position.

Slippage is the difference between the price traders expect when they submit a trade and the price they actually receive when it executes. Liquidity depth is the amount of capital available to fill trades at or near the current price. Depth determines price impact: the percentage the price moves when a trade executes.

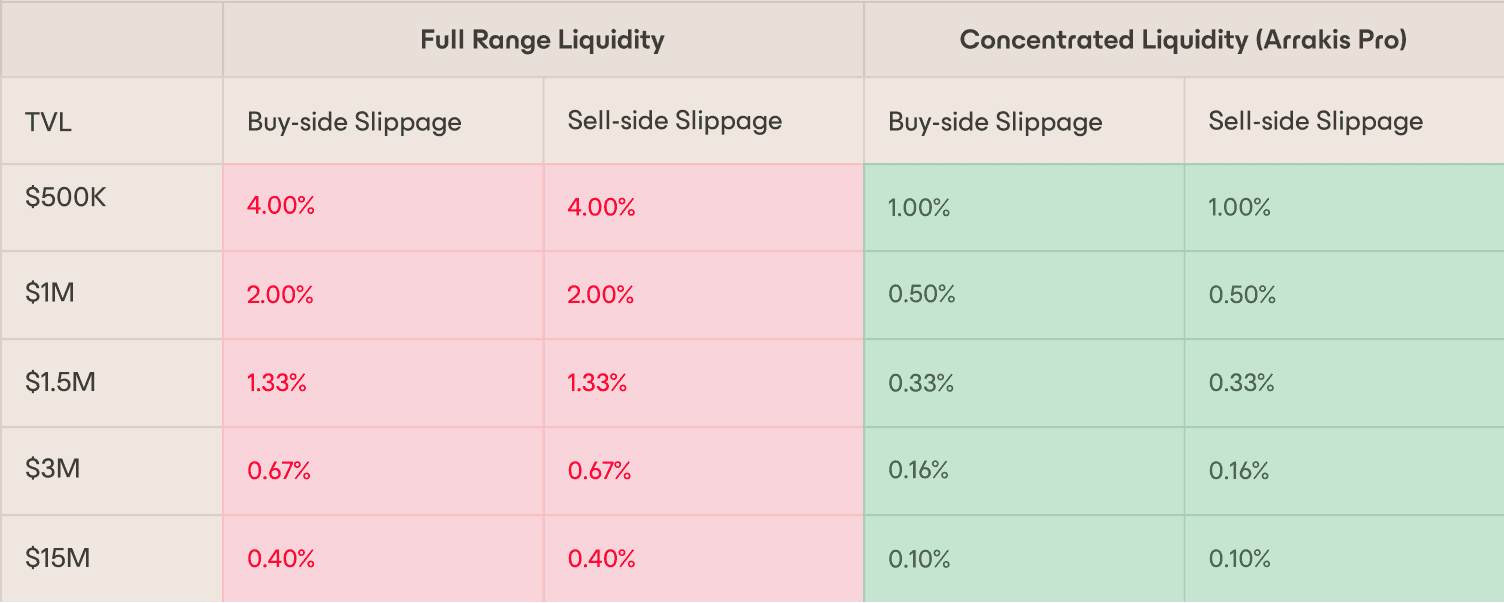

A pool with $500K TVL in a full-range position produces approximately 4 % slippage on a $10K trade. The same trade produces 1 % slippage in a concentrated position via Arrakis Pro.

Slippage and price impact for $10K trades across different TVL amounts (50/50), comparing full-range liquidity against a concentrated liquidity strategy managed by Arrakis Pro.

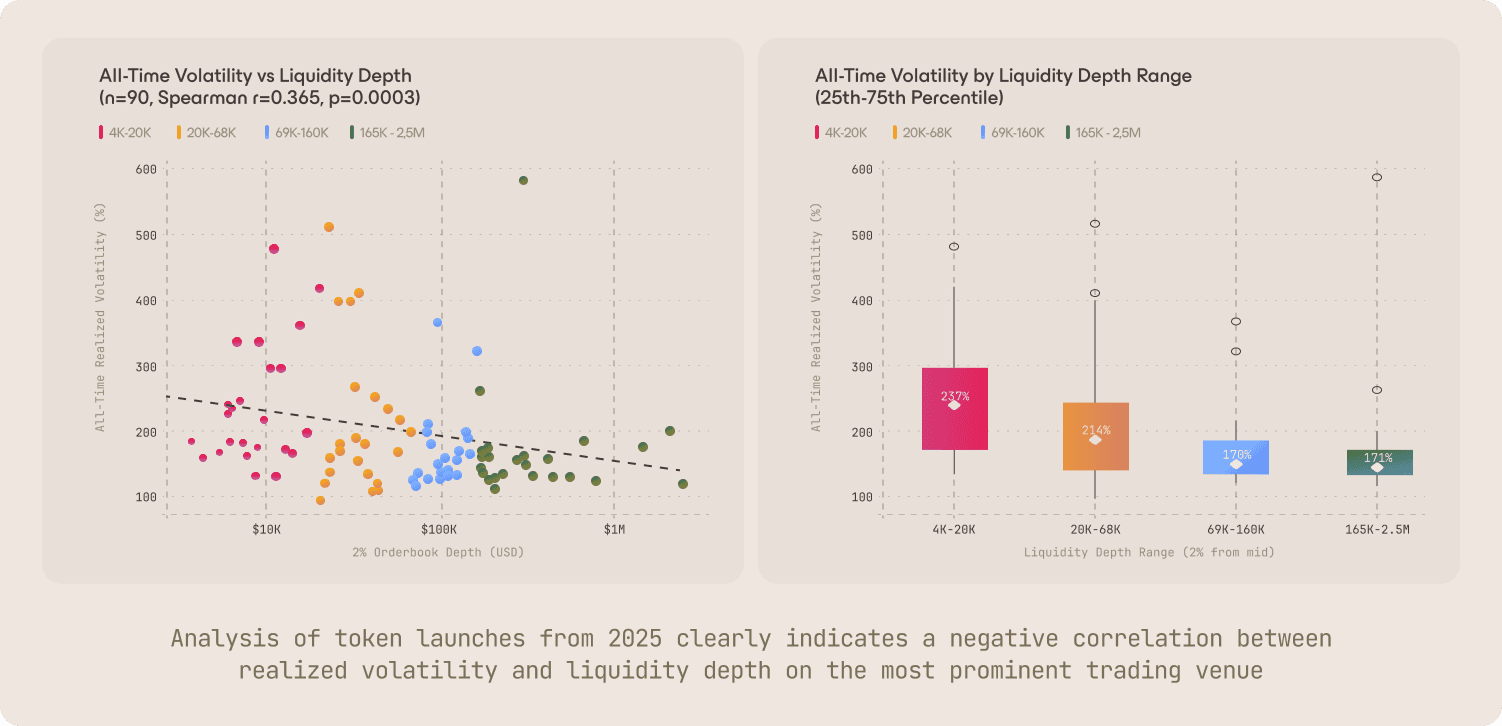

Our analysis of token launches from 2025 confirms a statistically significant relationship between liquidity depth and price stability. Tokens with less than $20K in 2% depth on their primary venue experienced an average realized volatility of 237% annualized, compared to 171% for those with $165K or more.

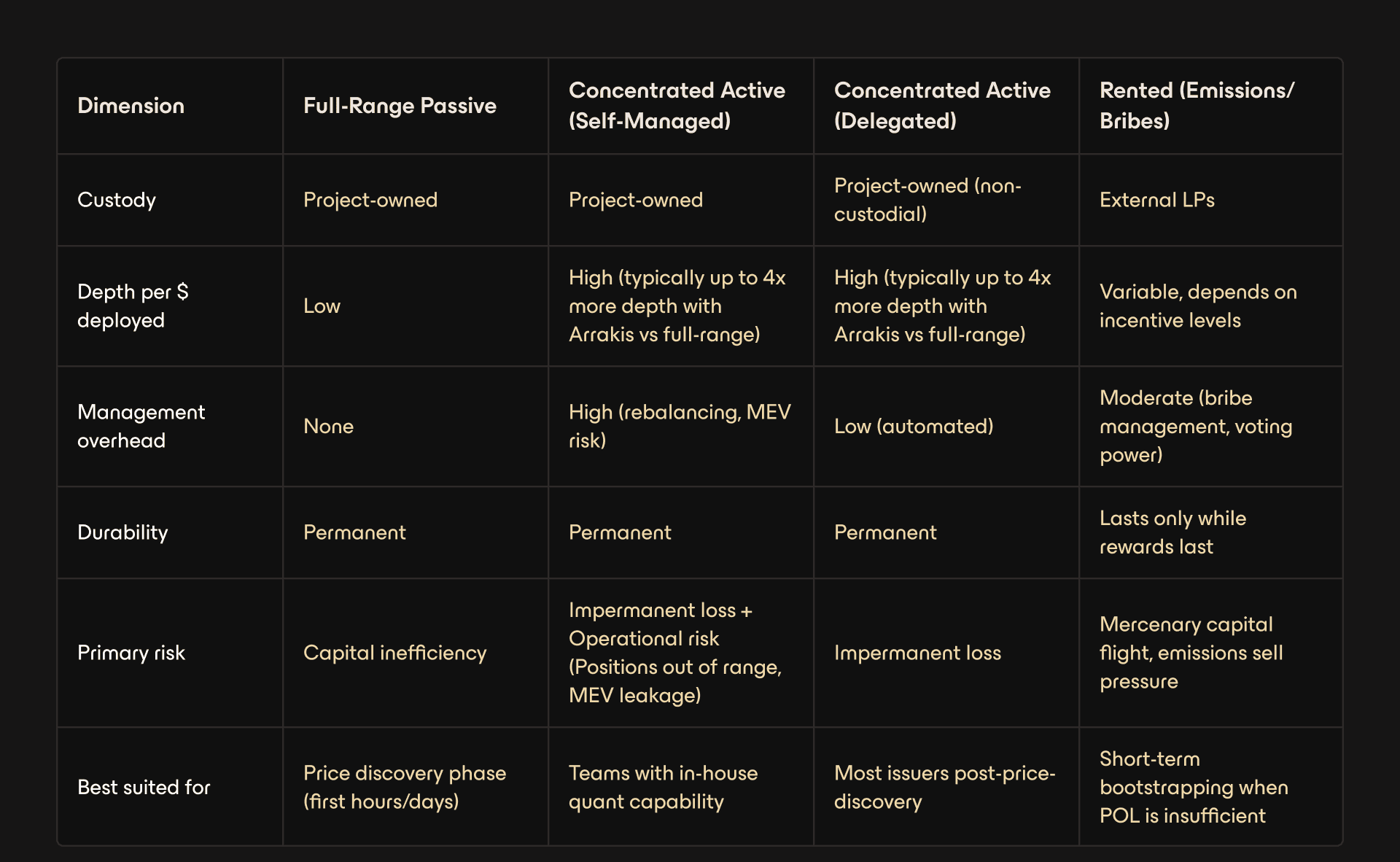

How Is DEX Liquidity Provided?

Two dimensions define how DEX liquidity works: how capital is positioned, and who owns it.

How capital is positioned

Full-range positions spread capital across the entire price curve, from zero to infinity. Simple to deploy and resilient during extreme volatility, making them best suited for the initial price discovery phase when direction is unknown and wide swings are expected.

Concentrated positions deploy capital to a specific price range around the current trading price. Greater depth per dollar, but positions stop working entirely when price moves beyond the range. At that point, the position has fully converted to the declining asset, and the LP faces leveraged impermanent loss. This makes concentrated positions dependent on active management.

Who owns the capital

Protocol-owned liquidity (POL) is capital the project deposits into pools, retaining full custody. Because the protocol itself is the LP, this liquidity does not disappear when incentives expire, external LPs withdraw, or CEX and market maker relationships change. POL can be deployed as either full-range or concentrated.

Rented (incentivized) liquidity is capital attracted from external LPs through token emissions or bribes. This typically attracts mercenary LPs who chase APRs and exit once rewards are claimed. It also adds sell pressure from LPs dumping their emission rewards.

Every DEX liquidity position sits at the intersection of these two choices. A full-range POL position optimizes for durability and simplicity. A concentrated POL position optimizes for depth per dollar but requires active management. A rented position offloads capital requirements but introduces external dependencies and is often too expensive to maintain sustainably, as projects typically overpay for the liquidity they attract.

The right combination depends on your launch phase, treasury composition, and operational capacity.

Should You Own or Rent Your Liquidity?

This is the most consequential structural decision, and it should be made before sizing.

Rented liquidity carries recurring costs and the mercenary-LP dynamics covered above. The capital cost of POL is lower than renting because the project seeds its own depth rather than paying a recurring cost to attract it.

The primary risk of POL is impermanent loss. Impermanent loss functions like a stock buyback: the pool accumulates the project's token at progressively lower prices. For example, if a project deploys POL in a concentrated range of $0.80–$1.20 and the token drops from $1.00 to $0.80, the pool gradually converts its ETH or stablecoins into the project's token across that range. The project ends up holding more of its own token, purchased at an average cost between $0.80 and $1.00. If the token recovers, the IL reverses and the tokens accumulated at lower prices are now worth more. This reframe turns range-setting into a treasury decision: set ranges at prices where the project is comfortable buying its own token. If you would not buy back at the implied range price, the range is too aggressive.

Renting makes sense in one scenario: when a project lacks sufficient treasury capital to seed meaningful depth on its own and needs to attract external LPs as a bridge to protocol-owned positions. Even then, the goal should be transitioning to POL as the project accumulates quote assets through trading fees and bootstrapping.

Where should you deploy?

Three structural choices set the boundaries of your market.

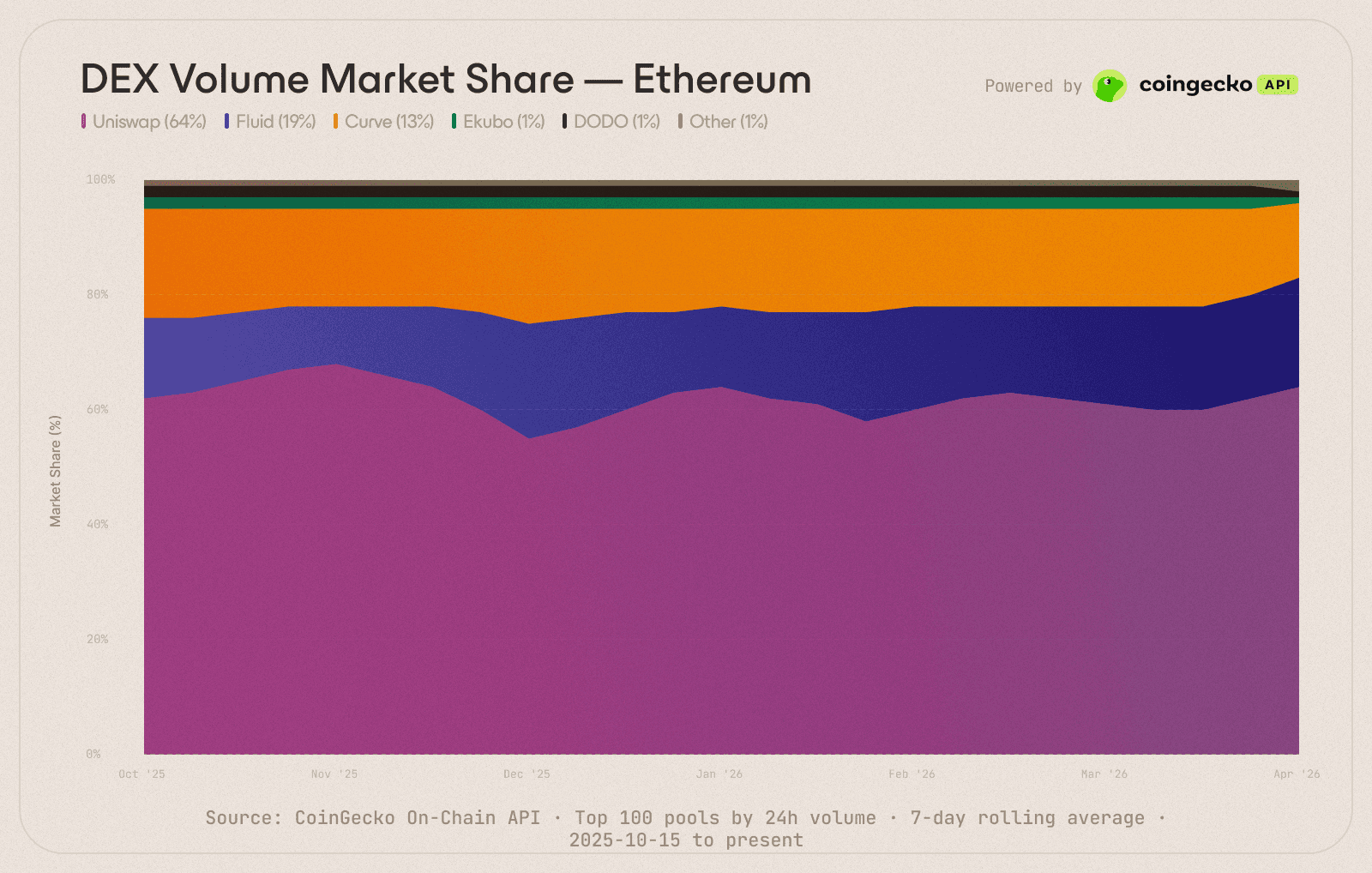

Which DEX: On Ethereum, Uniswap commands the majority of DEX volume (64 %). The Uniswap frontend remains the most used DEX frontend, making Uniswap the default venue for organic retail flow. Aggregators route to the best execution across all venues, but the Uniswap frontend advantage on Ethereum is structural and worth prioritizing.

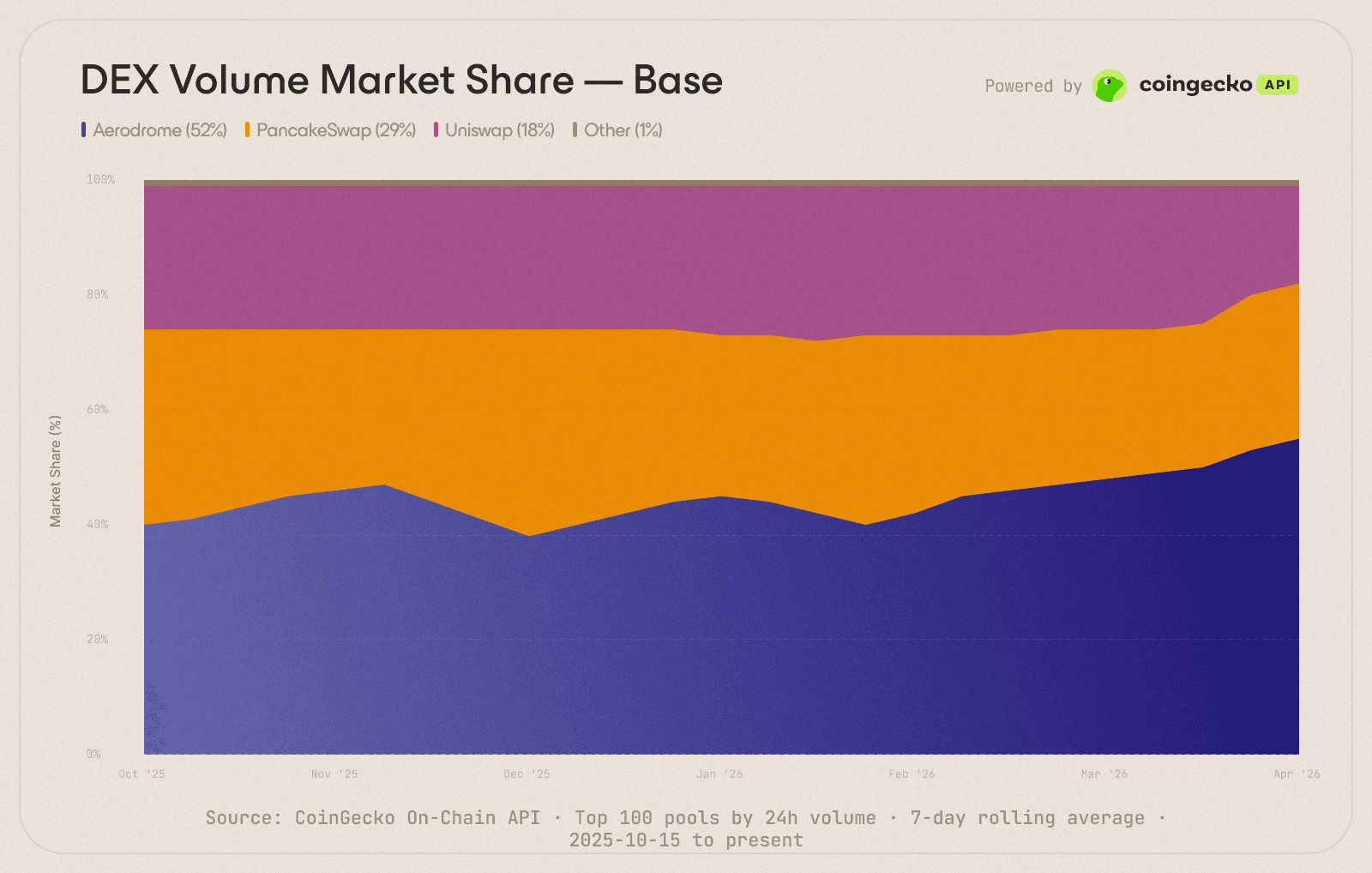

On Base, Aerodrome commands the majority of DEX volume (52 %) and is natively integrated into the main CoinBase app: DEX swaps initiated by Coinbase users route through Aerodrome pools. Aerodrome’s emissions model also directs AERO rewards to LPs, which can exceed trading fee revenue. This makes it effective for attracting external liquidity to newer or lower-volume pools.

On BNB Chain, PancakeSwap commands the majority of DEX volume, averaging $1.5B daily in Q4 2025 and holding 56-77% chain market share throughout the year, according to Messari Research. PancakeSwap's distribution extends across the Binance ecosystem, with Binance Wallet supporting PancakeSwap across BNB Chain, Ethereum, Base, Arbitrum, Linea, zkSync Era, Polygon zkEVM, and opBNB.

Which chain: Deploy where your users and product already exist. If your token is used within a product deployed on a particular chain, that token must be available on that chain. Bridged tokens introduce friction and fragment liquidity.

Which quote asset: ETH pairs produce less impermanent loss for governance tokens because both assets tend to move in the same direction. Stablecoin pairs expose the full price divergence between the governance token and a stable reference, increasing IL. For RWAs and yield-bearing assets, stablecoins are the natural pair. Some projects deploy both and bootstrap volumes on their token through arbitrage between both pools.

How much capital do you actually need?

How the capital is structured matters more than how much is deployed. A team with concentrated positions can match the depth of a much larger passive deployment.

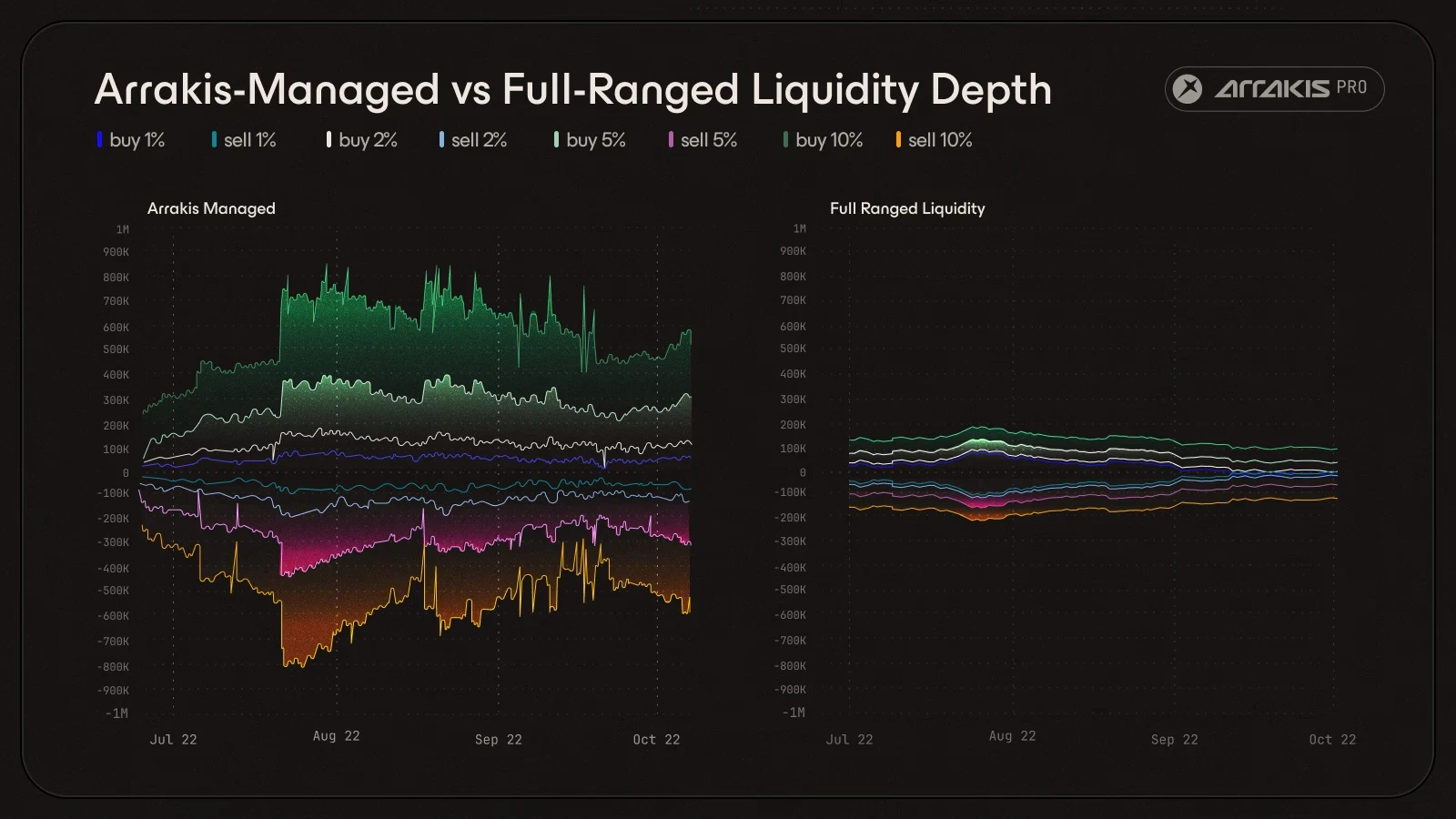

In a full-range position, capital is spread from zero to infinity. A $1M full-range position still produces approximately 2% price impact on a $10K trade. Concentrated positions focus capital around the current price. The tighter the range, the greater the depth per dollar. Arrakis-managed positions typically deliver 3-4x greater depth per dollar deployed and up to 4x lower slippage versus full-range positions.

Slippage and price impact for $10K trades across different TVL amounts (50/50), comparing full-range liquidity against a concentrated liquidity strategy managed by Arrakis Pro.

Two case studies illustrate the gap.

For VSN on Uniswap, concentrated management delivered up to 3x greater depth versus passive full-range positioning, and the Arrakis-managed pool became the deepest spot market for VSN, overtaking the primary CEX by over 55% at 1-2% depth.

When Morpho transitioned from self-managed positions to actively managed concentrated liquidity, sell-side price impact on $5K trades dropped from 0.45% to 0.16%, a 60% reduction, with 27% less TVL ($3.10M vs. $4.26M).

Size backward from sell pressure: estimate day-one selling, benchmark against price impact thresholds, then determine your minimum depth. If CEX commitments reduce available capital below that minimum, the DEX pool cannot absorb it and price impact increases.

How should you handle starting inventory?

If the treasury already holds sufficient quote-side capital, starting at 50:50 is the ideal configuration. It skips the accumulation phase entirely and lets the pool move straight into active depth management. For most projects this isn't an option. Treasuries are denominated almost entirely in their own token, and deploying two-sided liquidity requires quote assets (ETH or stablecoins) that the project does not have. Two configurations solve this without dilutive OTC rounds or market-selling the token.

Starting with mostly your token (80-100%). Arrakis' Bootstrap strategy deploys liquidity in asymmetric ranges weighted toward the project token. The strategy captures upside volatility to convert tokens into quote assets. Each time the price moves up, the position converts tokens to ETH or USDC, then rebalances to capture the next move. The token doesn't need to trend upward; it just needs to be volatile. Over time, the position migrates toward a balanced ratio through natural trading flow. Best when the treasury holds little or no quote asset and the team wants to avoid dilutive OTC rounds.

Liquidity Bootstrapping Pools (LBPs). Weighted pool ratios that shift gradually from token-heavy (e.g., 90:10) toward the quote asset (e.g., 50:50) over a defined period. The shifting weight creates a declining price curve that lets buyers enter at progressively lower prices, providing price discovery and accumulating quote assets simultaneously. Best when the team wants explicit, time-boxed price discovery before permanent liquidity goes live.

Quote asset inventory needs to be configured before the first trade. Bootstrapping only works if the position is live when initial buy pressure arrives. Projects that launch without quote-side capital cannot absorb sell pressure from day-one sellers, and they cannot retroactively capture the buy-side flow they missed.

(Projects using onchain launch mechanisms like Uniswap CCA or Aerodrome Ignition have inventory seeded as part of the launch event itself. See Token Distribution Mechanisms 101 for how those work; the design decisions in the rest of this guide apply equally to the pools they produce.)

What fee structure should your pool use?

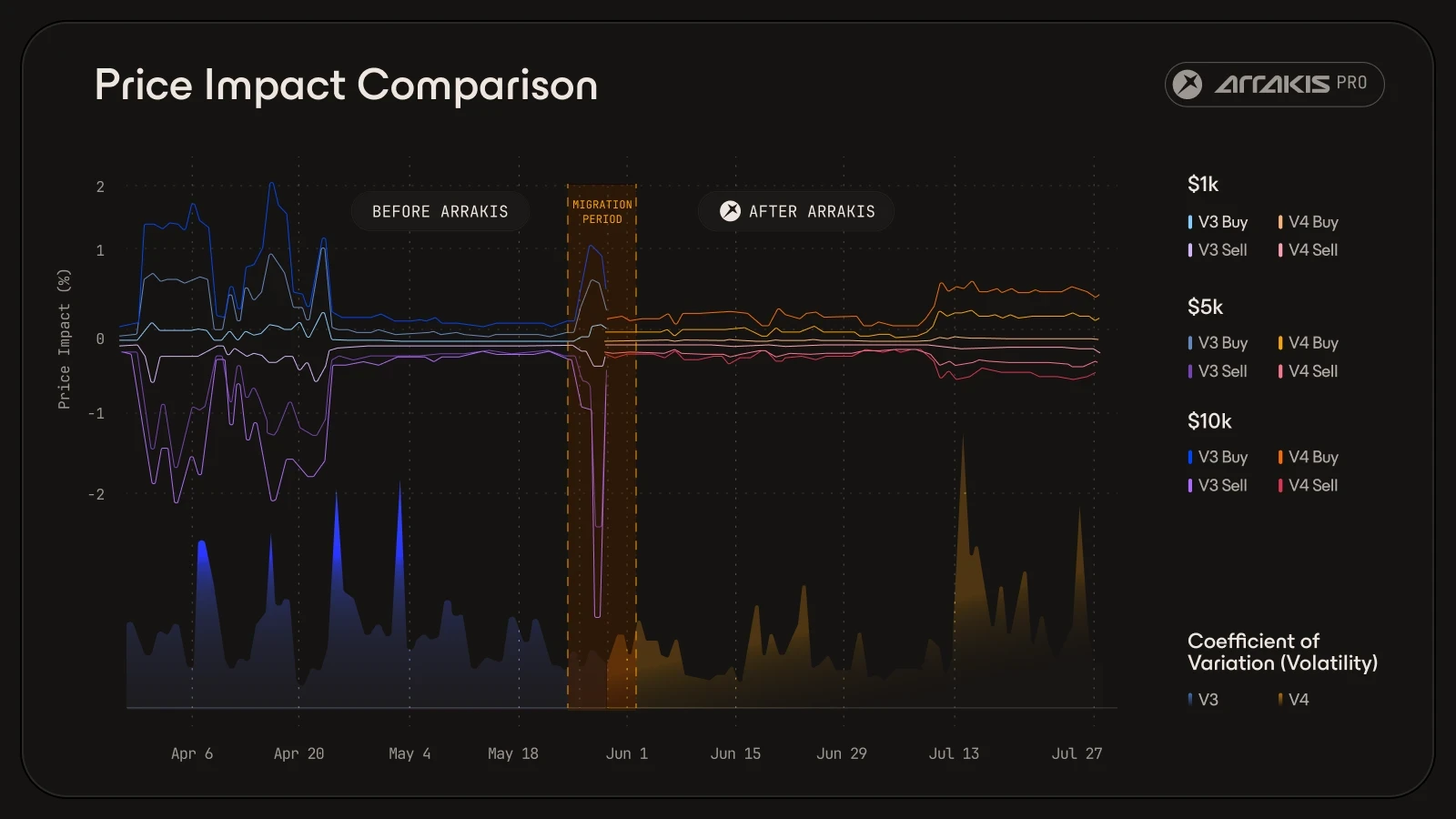

Static fee tiers (0.05%, 0.30%, 1.00%) create a structural problem. During volatile periods, fees are too low relative to price movement, and arbitrageurs extract value faster than fees accumulate. During calm periods, fees are too high, and organic traders route elsewhere.

Dynamic fees adjust in real time. Volatility spikes push fees higher, making arbitrage unprofitable. Calm periods pull fees lower, attracting organic volume. Imbalanced inventory triggers per-side adjustments so that trades rebalancing the pool become cheaper.

Pools with dynamic fees capture a higher percentage of trading fees. Static pools leak a significant share to arbitrage. On Uniswap V4, the Arrakis Pro Hook enables dynamic fee models that adjust based on volatility and momentum.

Fee strategy also depends on timing. Launch at higher fee tiers at TGE: aggregators have no competing lower-fee pools to route to on day one, and higher fees compensate LPs for volatility risk while filtering out arbitrage. Migrate to lower tiers as trading stabilizes. Dynamic fee hooks can automate this transition.

How often should positions be adjusted?

Concentrated liquidity is not set-and-forget. Three conditions trigger a position adjustment, without creating liquidity walls that distort the market or overriding natural price discovery.

Price movement. When the trading price moves, liquidity per tick around the active price determines depth. If the price shifts into a thinner part of the range, or out of range entirely, depth drops and capital sits idle where no trades occur.

Inventory drift. As trades flow through the pool, the balance between token and quote asset shifts. Lopsided inventory means the pool cannot absorb trades evenly on both sides.

Volatility changes. Calm markets reward narrow positions with more depth per dollar. Volatile markets punish them with higher risk of going out of range. A position designed for one regime underperforms in the other.

Delegated onchain management automates execution while keeping assets protocol-owned and all activity verifiable onchain.

How do arbitrageurs and MEV bots extract value from your pool?

Unprotected pools subsidize arbitrageurs with the project's treasury capital. Two forms of extraction primarily erode capital.

Loss Versus Rebalancing (LVR). Arbitrageurs trade against stale pool prices when the broader market moves.

Reverse LP sandwich attacks. An MEV searcher swaps a large amount into the pool right before an addLiquidity transaction, inflating the price. The LP deposits at the inflated price, and the searcher swaps back, extracting quote assets at the LP's expense.

Four design choices mitigate these risks.

Dynamic fees that increase during volatile periods make arbitrage unprofitable.

CEX-aware pricing incorporates offchain data so the pool does not wait for arbitrageurs to correct its price.

Private mempools keep position changes hidden from bots that scan public mempools, reducing the surface area for sandwich attacks.

Price range parameters on addLiquidity transactions revert the transaction if the pool price has moved, mitigating reverse LP sandwich attacks.

None of these protections are defaults. They require deliberate configuration at pool creation or through hooks layered on top.

How do you know if your liquidity is working?

TVL alone tells you almost nothing about market quality. A pool with substantial TVL in a full-range position can still deliver poor execution. Three metrics tell you whether your capital is doing useful work.

Price impact at standard trade sizes. How much does the pool price move on a $10K buy or a $50K sell? This is the most direct measure of liquidity depth. Lower price impact means the pool can absorb larger trades without moving the market.

Volume and fee capture. How much trading volume is the pool attracting, and how much fee revenue does it generate? A pool with high volume relative to its TVL is working efficiently. Low volume signals that traders are routing elsewhere.

Impermanent loss. How much value has the position lost relative to simply holding the assets? If fees and volume don't justify the IL, the capital would be better deployed elsewhere.

What Are the Costs of Getting DEX Liquidity Wrong?

Four consequences compound when DEX liquidity is designed suboptimally.

Every dollar of treasury capital does a fraction of the work it could. Concentrated, actively managed positions deliver greater depth per dollar (up to 4x more with Arrakis Pro) than passive full-range deployments. A team that deploys $5M passively is producing the market-impact equivalent of $1.2M to $1.7M managed concentrated. The rest is effectively unused capital.

Normal trading produces outsized price impact in passive full-range pools. The volatility data is unambiguous: pools below $20K in 2% depth ran at 237% annualized volatility in 2025 versus 171% for pools above $165K (see the chart above in “Liquidity Depth and Price Impact”).

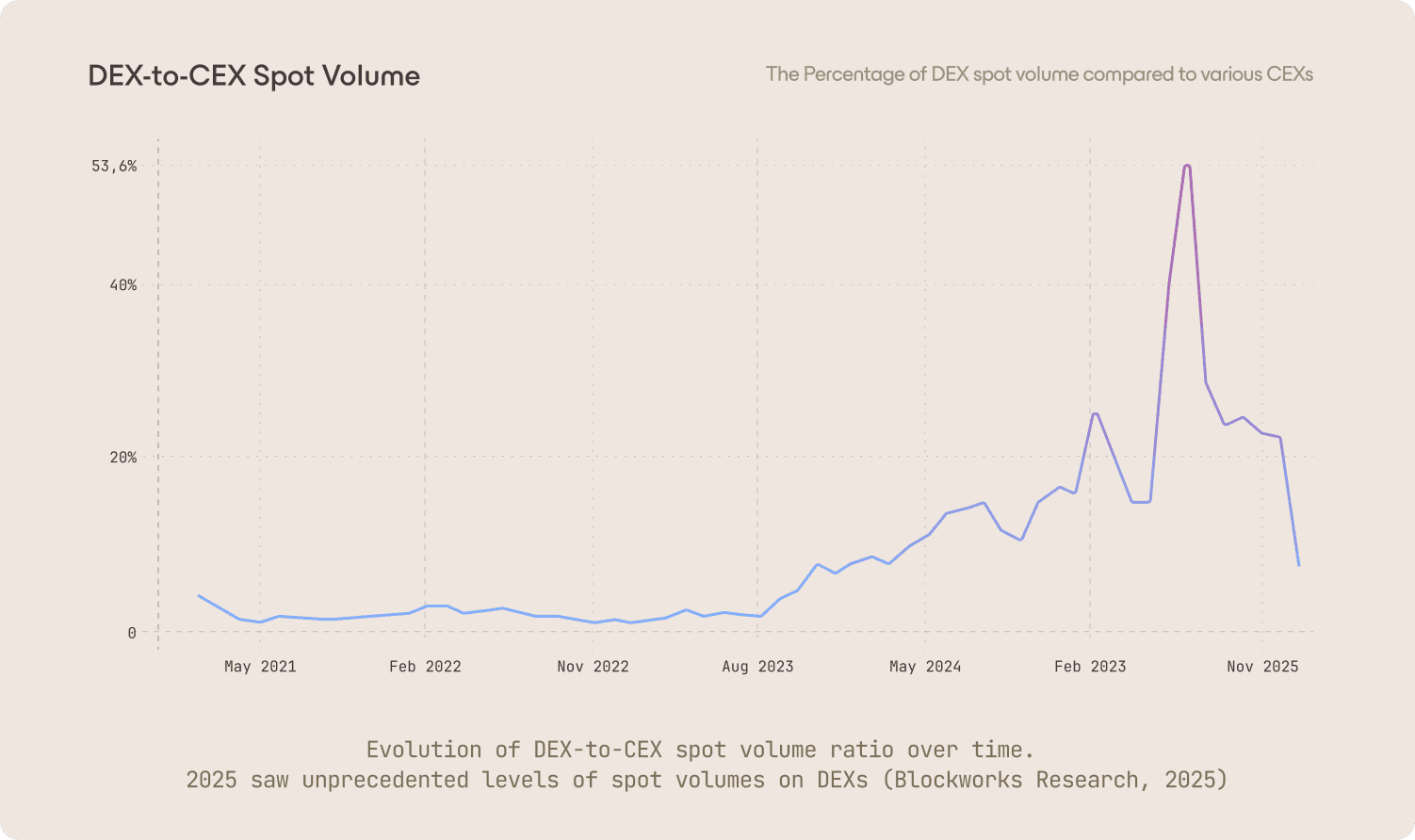

Your market depends on infrastructure you do not control. CEX listings can be revoked, market maker terms can change, and rented liquidity can unwind. If your onchain liquidity is a passive afterthought, there is no fallback. DEX-to-CEX spot volume ratios have increased approximately sixfold over the past five years according to research by Blockworks. The venue that most teams underinvest in is the one gaining the most share.

You get locked out of visibility. CoinGecko and CoinMarketCap are among the primary discovery platforms for retail investors. Both use liquidity and volume to calculate a Trust Score and Liquidity Score respectively, which determine how prominently a token appears across their platforms. Thin pools produce low scores and limited visibility regardless of project quality.

How Should Founders Compare DEX Liquidity Approaches?

What Are the Key Lessons for Founders?

Size backward from sell pressure, not forward from what remains after CEX allocations. Benchmark against price impact thresholds ($500K TVL = 4% on $10K, $5M TVL = 0.4%). If CEX commitments reduce available capital below the minimum depth your sell pressure requires, the DEX pool cannot absorb it and price impact increases.

Own your liquidity. Do not rent it unless you have to. POL eliminates the mercenary LP feedback loop and creates a persistent market that cannot be revoked. If the project lacks quote assets, bootstrapping strategies (starting at 80:20, targeting 50:50) allow deployment without upfront stablecoin reserves.

Concentrate after price discovery, not before. Full-range for the first hours when volatility is extreme. Concentrated management for everything after: Arrakis-managed positions typically deliver 3-4x greater depth per dollar and 4x lower slippage, with delegated onchain execution keeping assets protocol-owned.

Use dynamic fees where available. Static fee tiers leak value to arbitrageurs during volatile periods and repel organic traders during calm periods. Dynamic fees capture a higher percentage of trading fees. Launch at higher tiers and migrate down as trading stabilizes.

Configure protections deliberately. LVR and reverse LP sandwich attacks are not edge cases. They are structural risks that erode treasury capital continuously. Dynamic fees, private mempools, price range parameters, and CEX-aware pricing mitigate them, but none are defaults.

Before You Deploy: A Checklist

Pool structure

[ ] DEX selected based on where order flow originates (Uniswap for Ethereum frontend flow, Aerodrome for Base/Coinbase, PancakeSwap for BNB Chain/Binance Alpha)

[ ] Chain matches where users and product already exist

[ ] Quote asset chosen (ETH for governance tokens, stablecoins for RWAs and yield-bearing assets)

[ ] Fee tier appropriate for asset volatility, dynamic fees configured if available

Capital and inventory

[ ] Starting inventory ratio determined (100/0, 80/20, or 50/50) and bootstrap strategy configured before first trade

[ ] Capital amount justified by target depth and expected sell pressure, not arbitrary treasury allocation

[ ] Concentration strategy defined: full-range for price discovery phase, concentrated for post-stabilization

Operations

[ ] Rebalancing plan in place: who manages positions, what triggers adjustments, how often

[ ] Atomic execution confirmed for all position changes, private mempools for initialization

[ ] MEV protections active (dynamic fees, private mempools, price range parameters, CEX-aware pricing)

Go/no-go

[ ] Pool initialized correctly with tight price impact parameters

[ ] Team has operational capacity for ongoing management, or has delegated to an onchain infrastructure provider

[ ] Monitoring configured for price impact, volume-and-fee capture, and impermanent loss

The full sell pressure sizing framework, price impact simulations, and a month-by-month TGE prep timeline are in our Practical Guide to TGE. To structure onchain liquidity for your launch, schedule a call with the Arrakis team.

Thanks to CoinGecko and DefiLlama for the market data referenced in this article.

Disclaimer

This article is provided for informational and educational purposes only. Nothing in it constitutes financial, legal, tax, investment, or professional advice. Market conditions, deal structures, and fee terms referenced here reflect information available at the time of publication and are subject to change. Readers should independently verify all figures and terms with relevant counterparties before making any decisions. Arrakis makes reasonable efforts to ensure accuracy but does not warrant that all information is complete or current.